CyanoGuard raises €2.8 million to monitor cyanide safety in gold mining, food and medicine EU-Startups

Source: Maurice Jackson for Streetwise Reports 04/13/2020

The opportunities surrounding a potential district-scale prospect are outlined by Hannan Metals CEO Michael Hudson in conversation with Maurice Jackson of Proven and Probable.

Maurice Jackson: Today we will introduce an early-stage exploration company focused on identifying district-scale high-grade copper and silver systems in Peru. Joining us for our conversation is Michael Hudson, the CEO of Hannan Metals Ltd. (HAN:TSX.V; HANNF:OTCPK).

We’re glad to speak with you today to discuss the value proposition before us. Before we delve into company specifics, Mr. Hudson, please acquaint us with Hannan Metals, and share the opportunity the company presents to the market.

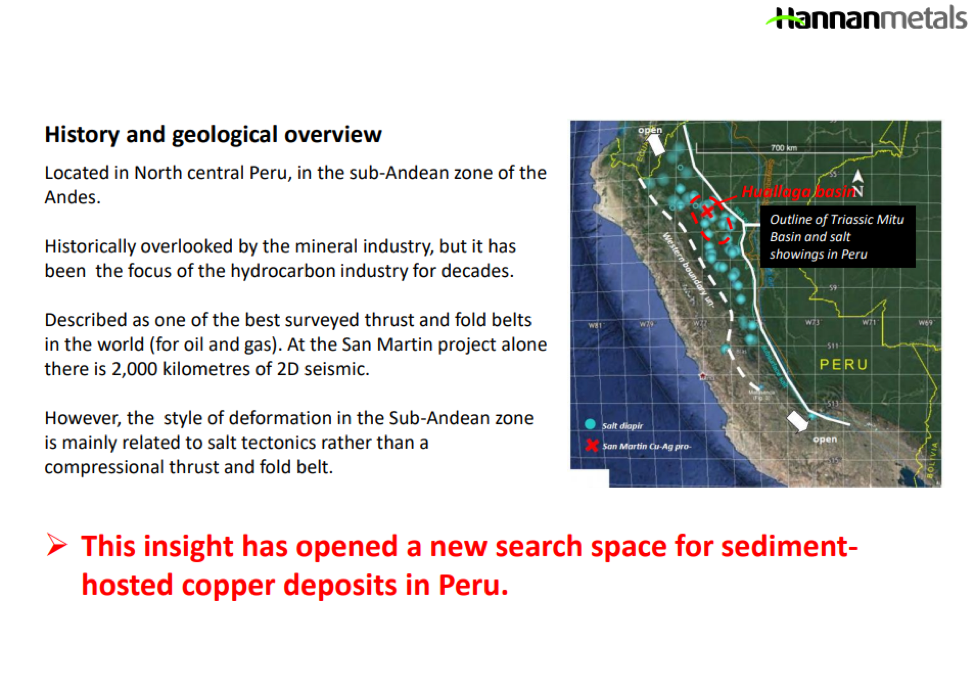

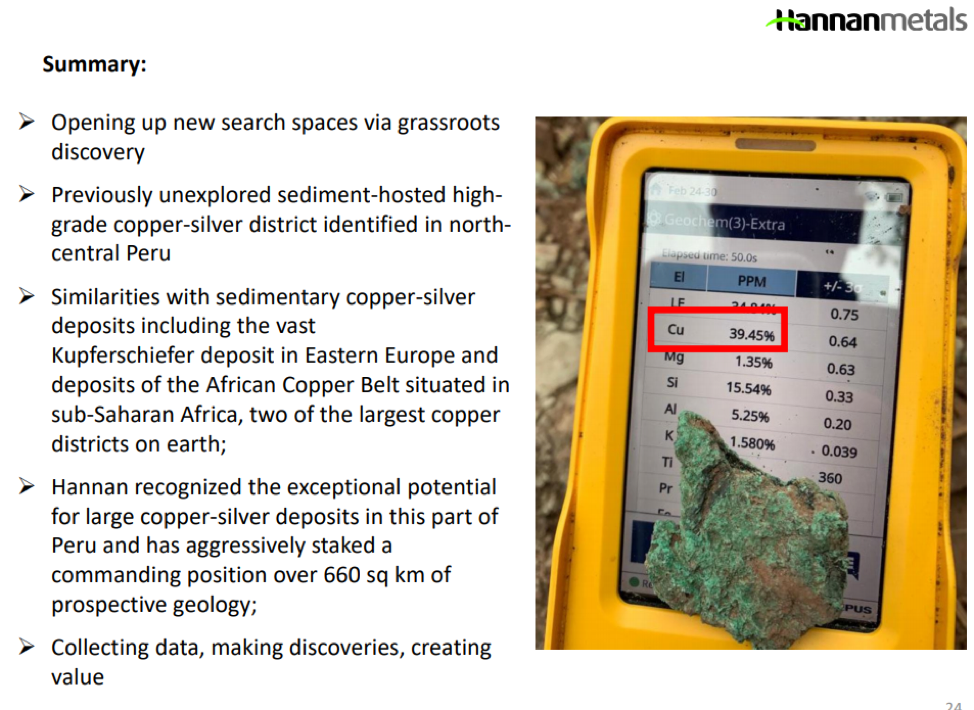

Michael Hudson: Hannan Metals Ltd. is a TSX.V-listed company exploring for copper and silver in Peru. The company is headed by people who have extensive experience within the mining industry, and specifically in Peru. We are exploring in a completely new district in the San Martin area of northeastern Peru. The project encompasses a newly identified, 120-kilometer (120 km) long, basin-scale, high-grade, sedimentary-hosted copper-silver system. This is a new deposit style for Peru, however it is the second-most prolific producer of copper, as a style, in the world, after porphyries. Geologically, the system shares similarities with sedimentary copper-silver deposits in the African copper belt. With a first-mover advantage, we recognized the exceptional potential for large copper-silver deposits during late 2018, and since then have aggressively staked 521 square kilometers of prospective geology.

Maurice Jackson: Let’s go to Peru and visit the San Martin. Where and how did Hannan Metals obtain the data that led to the acquisition of San Martin?

Michael Hudson: We have a 25-year history of exploring and acquiring exploration data in Peru. Based on some information from our datasets, we commenced reconnaissance exploration and found a significant amount of high-grade copper over a large area, and started staking. We put in our first claims in September 2018, and granting of these mining concessions started at the end of 2019. We are putting in a significant amount of effort to ensure that we meet and engage all relevant stakeholders, from local communities to regional and provincial authorities. Generally, the local people have been very welcoming. We are talking to people, listening to concerns, educating as we move forward, and building trust.

Maurice Jackson: Is the San Martin project already fully permitted?

Michael Hudson: We have about 40% of our mining concessions granted to date, with more continually being granted on a monthly basis. We are not at a drilling stage yet, with work over the first half of 2020 aimed at regional reconnaissance to [do] detailed mapping of mineralized horizons over specific prospect areas. Our aim is to balance project and social governance. We will try and keep the permitting process as simple as possible by keeping target areas small and engaging with the community to educate them and be transparent throughout the entire process. We are taking our time to define the right target areas and engage with the relevant communities.

Maurice Jackson: Can you elaborate on the infrastructure and the logistics surrounding San Martin?

Michael Hudson: The San Martin project is located about west and south of Tarapoto. There are multiple daily flights into this city from Lima. Project access is excellent via a proximal paved highway and, broadly, no part of the project is more than two hours’ drive from Tarapoto. This infrastructure is, of course, relatively new for Peru, and makes this project so much easier than if we were tackling it, say, 20 years ago.

Maurice Jackson: Well, let’s talk about a clever way that Hannan Metals has de-risked their project. Hannan has shifted the paradigm on exploration by implementing a concept known as new search spaces. And the intellectual capital derived from this concept has positioned Hannan Metals in a first-mover competitive advantage among your peers. Sir, please introduce the concept of new search spaces, and how does it fit into the narrative of defining the San Martin as a greenfields or a brownfields exploration plain?

Michael Hudson: Well, firstly, I didn’t coin the phrase. It comes from a very smart geologist called Jon Hronsky. And really, this is a concept that’s been taken a little further than just talking about grassroots exploration or greenfields. It’s basically identifying an area of prospectivity for whatever you may be looking for. And it may be in an old or a very mature terrain where there’s lots of data, but you come up with a new thesis. And then you search for that new thesis, whether it’s going underground for high-grade systems underneath old oxide gold, for example, or you go into new areas completely and say, “Well, the San Martin area has the same geological characteristics for many, many reasons as some of those super deposits that form in Africa or in Poland and northern Germany.” And then you collect the data that opens up that search space, I suppose.

It really is the true way to make discovery. It’s very hard to go back to old ideas in old camps and do the same again. And really those easy pickings have been made in our business. So you really have to think a little broadly from the initial start of your exploration. It’s looking into new areas with new theses or ideas or concepts, and then collecting the data to support or refute those. That’s the exploration or scientific process, but it really means that you’re thinking about it much earlier on, from a perspective of trying to find something large and new.

Maurice Jackson: Mr. Hudson, to truly appreciate the value proposition of the San Martin, please provide us with a mental picture and tell us about this stratigraphy and the genetic model.

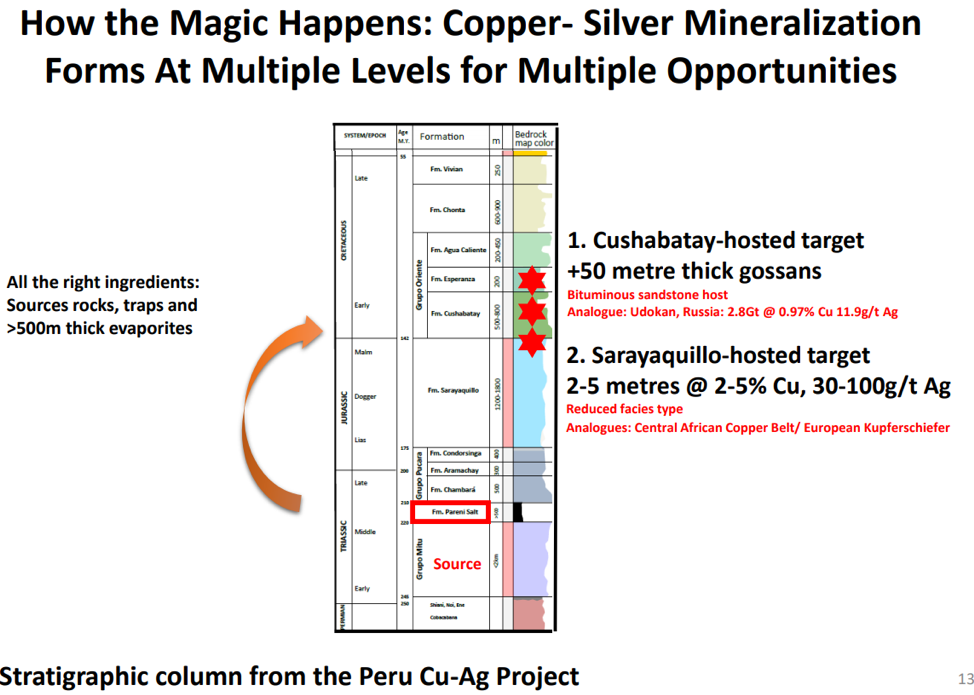

Michael Hudson: That is how the magic happens, I suppose, and we have been very fortunate here in, that this literally had very, very little exploration. There have been a couple of explorers in the past in this area, but we’re talking one year here and one year there. But really, the area and the understanding hasn’t been put together until. . .the last six to 12 months.

We’ve benefited from the data that has now been made freely available to the hardrock mining industry from the petroleum business, and the petroleum explorers were working in these areas a long time ago—way, way, way before we ever thought there could be any prospectivity here for metals. And that’s important because the petroleum explorers have bought hundreds, if not millions, of dollars’ worth of exploration data collected in a different way for a different commodity, of course—looking for oil. We can use that data and apply it to the things that matter for copper, and the things that matter for copper here in the sediment-hosted copper systems

I should say, there’s quite a large amount of silver with this system. So it’s really a copper-silver system. The things that matter here for these systems, like any deposit, are source, transport and trap. And they’re fairly well defined. It’s a relatively simple model in its gross scale. We always look for a source, and the source rocks, and the seismic data that the oilees have produced over these areas, give us a great understanding of the rocks, or the stratigraphy, or the layers of rocks and how they’ve formed through that period of time.

So, we can identify source rocks. We can identify transport, which is really important also. The seismic shows us those big structures, those big faults that have operated from very early stages in this geological basin right through to when the Andes were forming, and they went from. . .extension to compression when the Andes were forming. All these different stages we can identify through the rock record, and determine not only what is important, but when, and then we can target those structures that have been moving at that appropriate time.

And then the trap is probably the most important part. And in this case, it’s a chemical reaction that drops the metal out. We call it a redox boundary, a reduced oxidized boundary. The fluids are oxidized, and when they see the first reduced rocks in the sequence—they could be anything from black shales or graphite to what we have here, organic material—then the copper drops out.

The key point now is that these systems form over a vast scale. We have an area here that is under tenure for 120 kilometers of length. My apologies for using the metric system, but it’s something like 60 or 70 miles. It’s a very, very large system that is working that source, transport and trap. We’re finding copper in those trap horizons over this extensive zone. It’s not just one trap horizon we see. We see multiple traps, multiple redox boundaries forming in that stratigraphic pile of rocks. So, that data-rich environment that we have has really helped us fast track not only to understand, but to target, this system over such a large area.

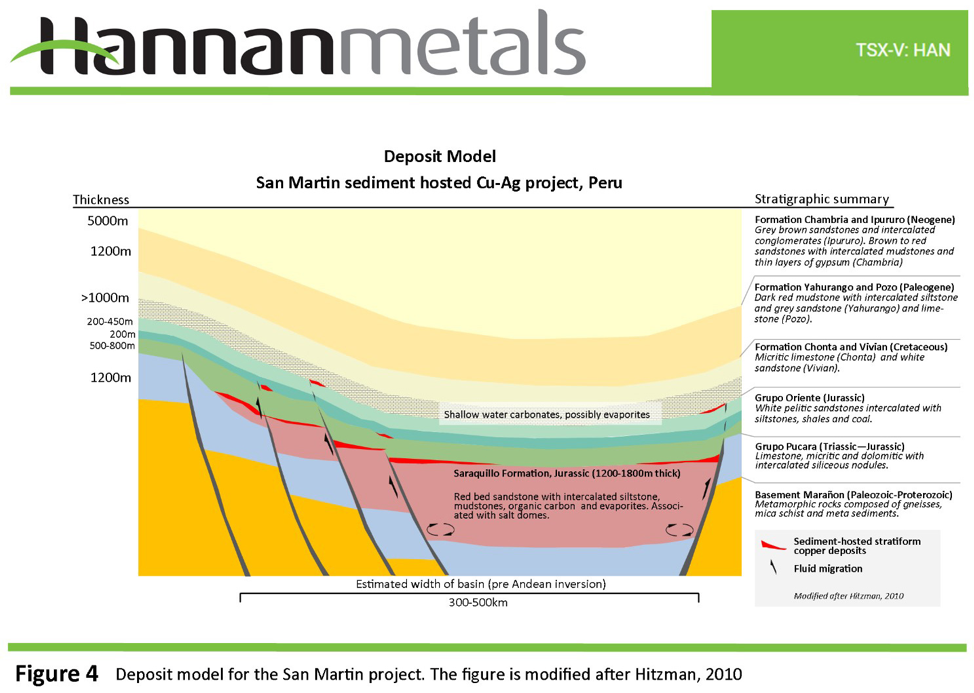

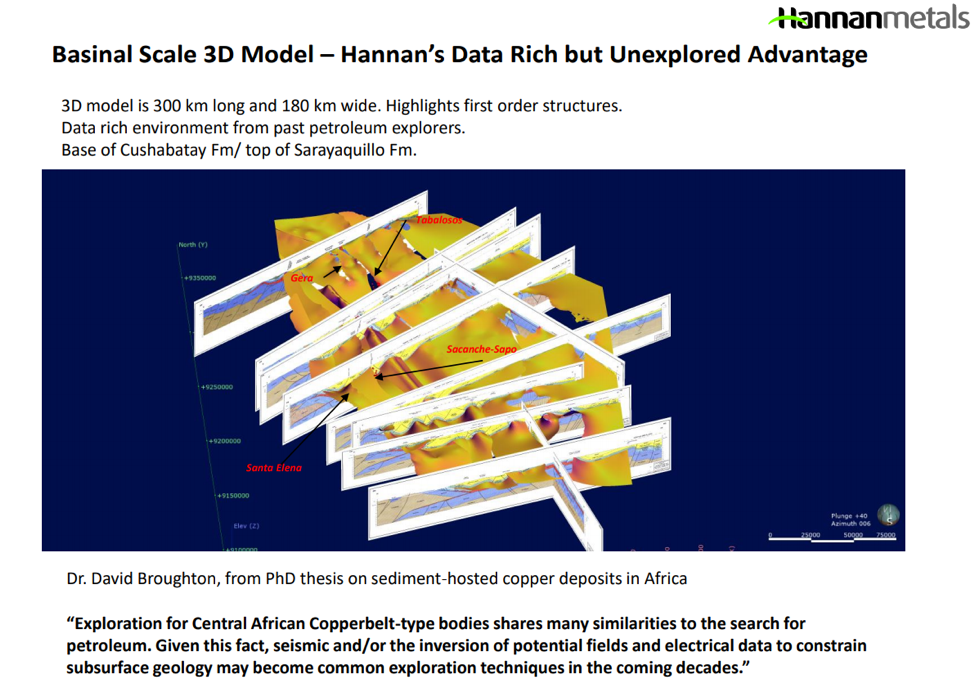

Maurice Jackson: We have before us a 3D model. What are we looking at here?

Michael Hudson: This is quite an unusual circumstance, in that [this area has] really only been explored for less than a year, [and] we’re able to build up a comprehensive 3D model. And this is a model in a program called Leap Frog. It’s something like 300 kilometers long by 180 kilometers wide. We can see the planes, or the sections, like cross-cutting a loaf of bread along the long axis. Their interpretation is from the seismic sections that the oil companies have provided.

We’ve been able to tie all those together literally in this program, and we can start to understand all those features that I’ve just talked about: the source, transport and trap. Features that really allow us to understand how this copper basin formed, and how the copper formed, and that gives us the style. Once again, as I said, this style wasn’t really understood until all this data was pulled together.

Then it allows us to home in on specific areas, not only stake those areas, which we’ve done very aggressively. We’ve had a first-mover advantage here because we were first, and it’s led to a staking rush all around us, I should say. But we had that benefit of all that data and the ability to stake what we wanted first. And then, within those mining concession areas that we’ve staked, many of them have now been granted. We’re able to narrow down the areas which we want to explore.

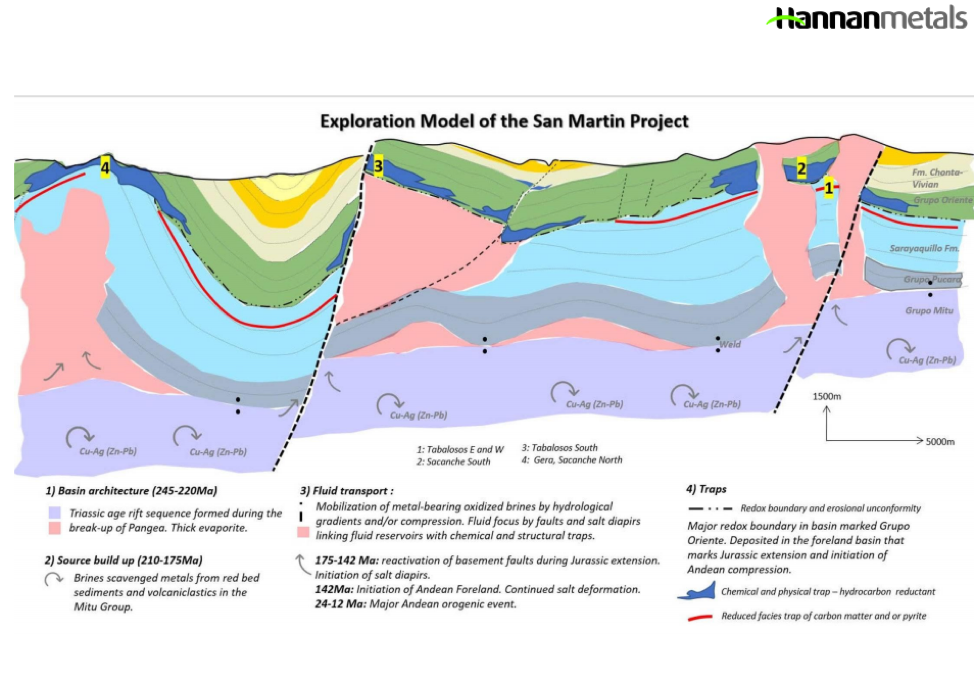

Maurice Jackson: Can you walk us through the exploration model?

Michael Hudson: This is a very good, summarized, cross-section model created by Lars Dahlenborg, the president of Hannan Metals. What he’s summarizing there is the source, which are those purple rocks and the fluids taking the copper. The other key point here that I didn’t mention before is that scavenging the fluids and bringing up into those source rocks is driven by salt, of all things.

So, there’s vast salt deposits that formed in these areas, and salt forms an amazing scavenger of metals. These highly brine-rich fluids act with superpowers, basically, to take the copper out of those purple rocks at the bottom. Then those fluids move up through those faults. So there’s the transport. We can see the dotted lines.

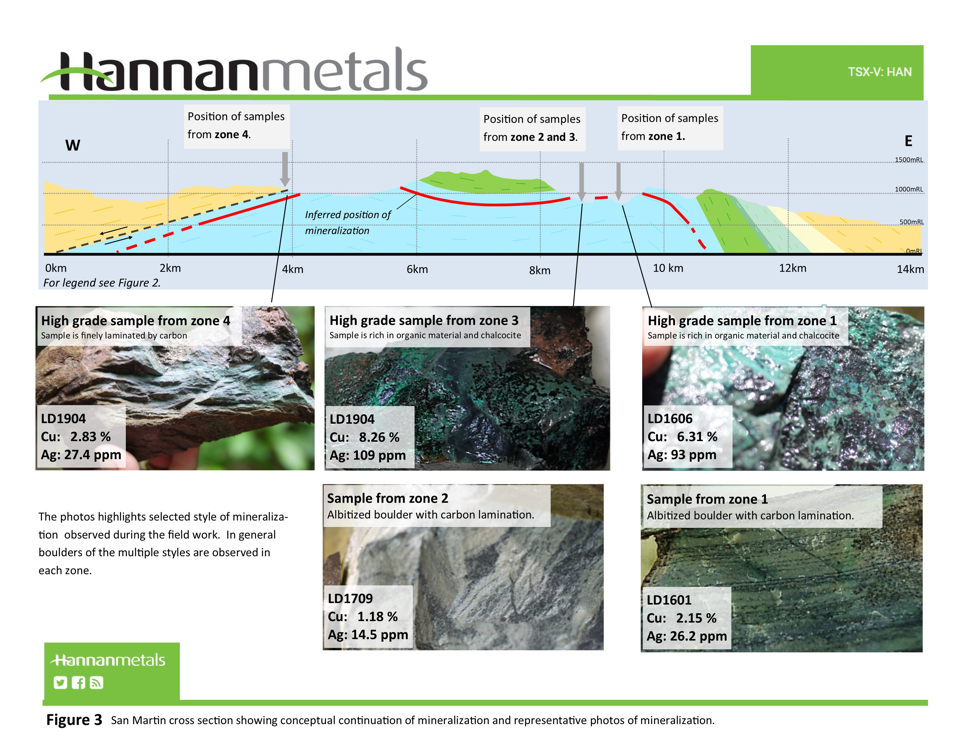

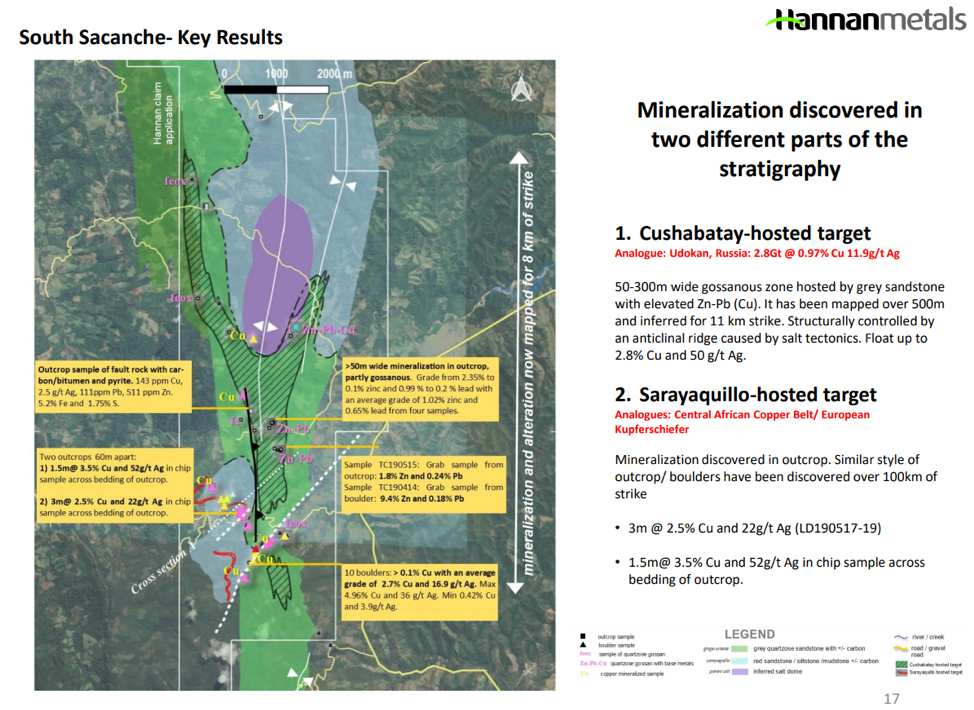

And then into those areas at the top there, we’ve got little red line. That’s one area we call the Sarayaquillo Formation, and that’s one area where this redox boundary, or the trap, forms—and then even up and higher, where there’s the green rocks with the blue. They’re areas where we’re finding gossans of lead and zinc, which are peripheral to the copper—and also copper in those areas now. [The gossans] are 50 to 80 meters wide at surface over multiple kilometers. This is a big and vast system. We’re talking about five- or six-kilometer views through the earth’s crust there. The scale of that is very big, but that’s the magic.

Maurice Jackson: You alluded to some comparisons earlier, but a picture’s worth a thousand words. And when I think of the San Martin, the first thing that comes to my mind is scale, and I’m talking about district scale. To put some things into perspective, can you provide us with some comparisons?

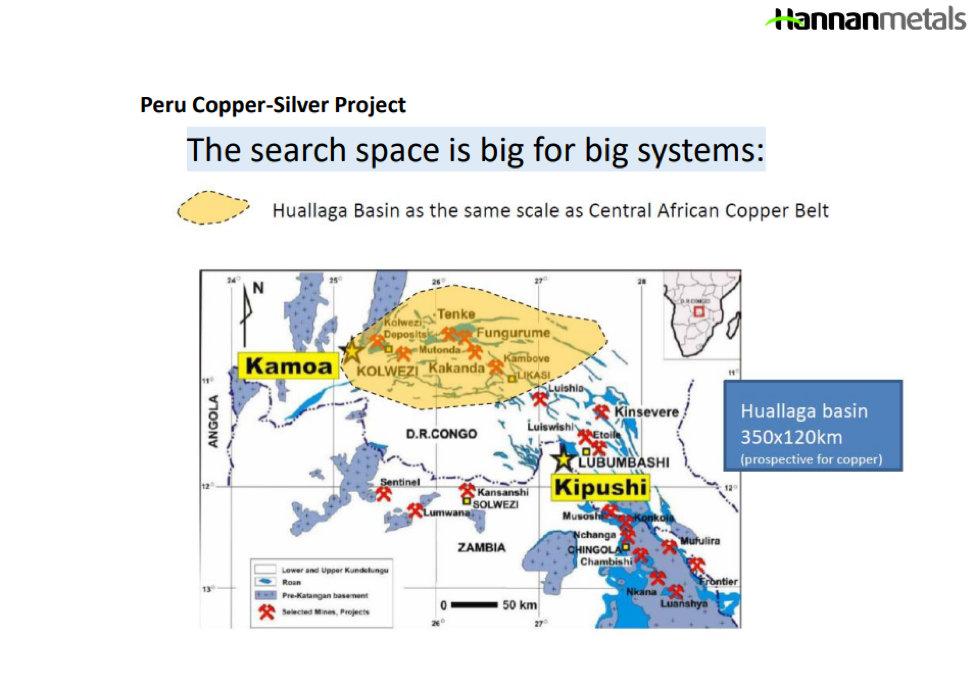

Michael Hudson: Yeah, the important things that you’ve just mentioned there are scale and grade, and if you can find that, that’s the nirvana of our business, of course. We have both of those in abundance. The picture that you see here is the Central African copper belt. It’s not where we’re exploring, of course, but what it shows is the scale of that system. The sediment-hosted copper deposits on earth are the second-most prolific form of copper, where we derive our copper from—the first being porphyry these days. The porphyrys are coming to an end, in my prediction. Those higher-grade porphyrys have been mined. There’s many more of them that have a lower grade, but as the world is changing, those big open pits with lower and lower grades become less desirable. These higher-grade systems that have a smaller footprint will be more desirable. And that’s what happens here in the copper belt, in many respects.

These systems are big and high-grade. You can see the scale of the basin that we’re exploring, called the Huallaga Basin, and that’s overlaying in that yellow color. And you can see we’re about a third the size of the copper belt just in the basin that we’re exploring in. That is really only a small part of this full-end basin system that extends on the eastern side of the Andes.

This is a new copper belt that not only exists where we’re exploring, but it extends from Colombia through Ecuador, where we have some peer companies exploring for the same systems. They’re about 300 kilometers north of us, and then down through Peru into Argentina and Chile. So, this is a big new copper belt. We have some of the more advanced and more easily accessible areas and that’s why we targeted where we wanted to, but this has some big implications for Peru too, right? This is a new copper belt for Peru potentially developing here. They already produce, on a country basis, the second-most amount of copper in the world. This could shift them to number one, if this thesis continues to hold.

Maurice Jackson: We’re going to cover your technical team later, but they’ve been quite successful in the results on the implementation of the new search spaces. And that’s not just on scale, but equally impressive on identifying high-grade. What are some key results that have current shareholders excited?

Michael Hudson: We have some very high grades, and they’ve actually surprised us too, to be completely frank, Maurice. This system is developing some very high grades, from the initial boulders—and hundreds of them that we found over this very vast area in creeks—and then we’ve started to find some of these outcrops. We’re seeing three to five-meter-thick zones in the Sarayaquillo Formation running 2–5% copper, something like that. That obviously is our next challenge, is to find continuity of these high grades, and that’s what we’re working to do, of course. But as I’ve said, it’s relatively early stages. This is our first intense year of exploration, which has had a little hiatus, of course, now, with everything that’s going on in the world with COVID-19. But we still had quite a good start before we were shut down a few weeks ago.

There’ll be many more of these high grades found. Also, we’re finding not only that Sarayaquillo, that 2–5% copper over those widths over large areas. We’re seeing these outcrops 20 kilometers apart, and we’re finding very thick lead-zinc gossans that we think are peripheral to the copper-bearing parts of the system. These gossans are 50 to 80 meters wide and running percent levels, up to 10% zinc.

The main target here is copper. But you never know what you just may find here. And we may find both—not only a copper system, but a lead-zinc system, as it’s turning out here. So, yeah, we’ve been very successful so far because of that data-rich environment that I talked about before, which has allowed us to target these areas. Just maybe there’s a hell of a lot more here to be found, of course, and so the early results will reflect where this project’s going.

Maurice Jackson: What are Hannan Metals’ principal objectives for the next 12 months?

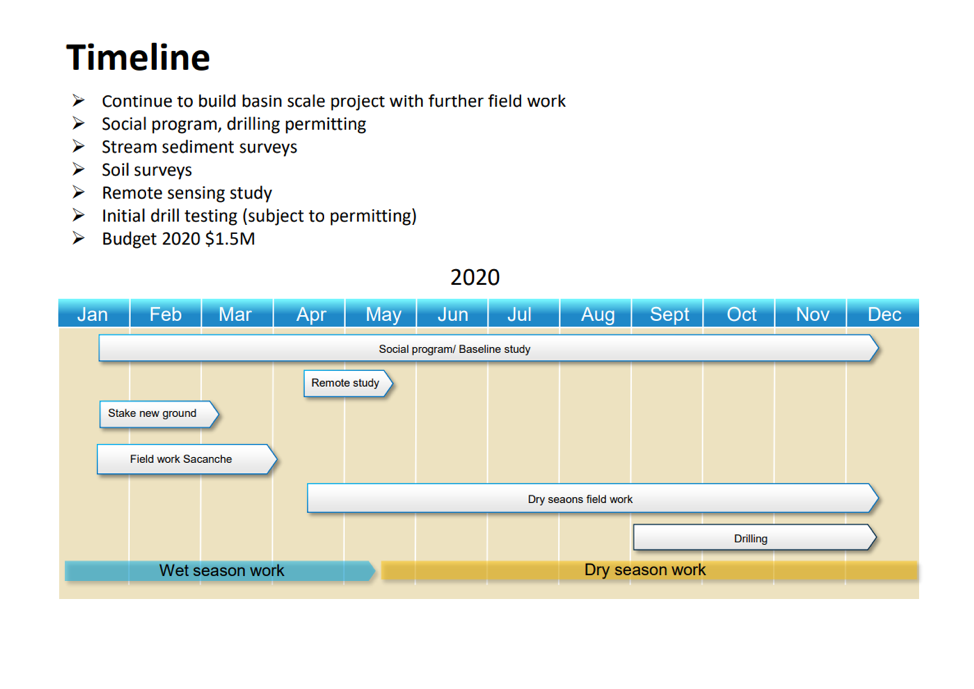

Michael Hudson: We hope that within the next year we will have drilled and demonstrated both continuity and scale of the mineralized system. This will be subject to permitting. We have recently raised CA$2.2 million (CA$2.2M) and now have a CA$1.7M budget for 2020 to complete a significant amount of field work over the next year.

The other key point is our main objective to work with the locals to tell them what we want to do, to gain their acceptance, and then come back and show them what we’ve done. And show that we’ve been operating with responsibility. Because these areas haven’t been explored before, there’s a general lack of understanding about what exploration is, so there’s a lot of education here to be done to explain that we’re prospectors, and obviously looking for areas that could potentially be mines one day.

But it’s a very high-risk business, of course, and we just don’t know where those better areas are going to be. So, it’s very much a first principle, working with the local people, as well. So, that’s a key objective as well, because if you get off on the wrong foot anywhere in the world from the very early stages, it’s very hard to recover. Starting well is a key objective for us in that respect.

Maurice Jackson: We’ve discussed the good. Let’s address the bad. What can go wrong, and what is your action plan to mitigate that wrong?

Michael Hudson: Well, lots of things can go wrong in exploration. You don’t find what you think is there, and then that second-guessing nature, without a doubt. As I hinted at before, we are de-riskers by nature, and the only similarity of businesses is the R&D [research and development] business in the pharmaceutical business where we spend lots of capital. There’s very few projects that progress and advance forward toward mining. That’s sort of like the wonder drugs that are eventually permitted and become very successful drugs, after lots of R&D in the pharmaceutical business. That’s what we’re doing. So there’s, of course, inherently a lot of risk.

How is that mitigated? That’s mitigated by having the right managers of the scarce capital that we’re able to access in the capital markets, and exploring appropriately. Not spending another dollar if we’re proving something isn’t there rather than is there. It all comes down to the opportunity itself, and whether the system develops. And so far so good. We can certainly see that there’s truly a great prize here to be gained. But we’ll spend the capital appropriately to mitigate those risks.

The other area, I suppose, and I touched on that, also is permitting. We want to make sure we get that right. So, it’s no good if we find the world’s biggest deposit of copper and we’re never able to access it—and, of course, with getting the local stakeholders our side. We have to make sure that those two go hand-in-hand. And really, it’s working with credibility and respect, and good communication. And, like any relationship in life, if you have those values, then ideally things can progress for you, but that’s our culture of the company, and how we aim to succeed.

Maurice Jackson: Those are some good ethics to subscribe to. Switching gears, we’ve covered the project. Let’s discuss the people responsible for increasing shareholder value with their business acumen, and discuss the commercial and technical expertise your team provides to Hannan Metals’ shareholders. Mr. Hudson, please introduce us to your board of directors and management team.

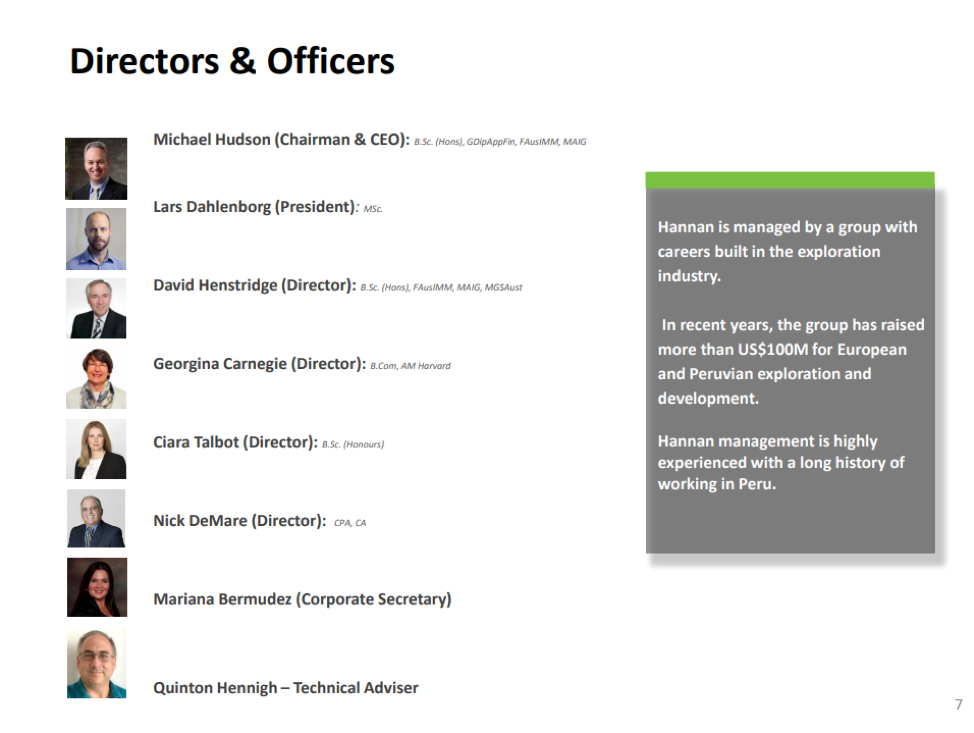

Michael Hudson: Well, I’ve mentioned a few of the team here before. I see myself as a leader and spokesperson, but I have some much more capable, and fantastic people around me. I should just say that I’m a geologist, of course, and I worked in and breathed geology for my career over the last 30 years. And. . .what I really love doing is finding things, and that’s what motivates me.

I’ve worked with a good group of people, the majority of which I’ve worked with for the last 20 years in the junior business. We’re a very tight team. We’re technically driven. We’ve been in the capital markets, and made many discoveries before. In the last cycle we took three discoveries to half-a-billion-dollars in market capitalization, through from first principles, and really you can say this is our next one in waiting, in terms of the next discovery.

Lars Dahlenborg is the president. He and I have worked together for 12 or 13 years, and Lars is a brilliant geologist, and done most of the pulling together here. . . .It’s very important to have geologists who’ve made discoveries and know how to manage their capital. Some gray hair is important, and David Henstridge is a geologist I’ve worked with for 20 years, and he sits on the board also. Ciara Talbot is a geologist also. Ciara is the director of exploration for Lundin Mining Corp. (LUN:TSX), so she runs Lundin Mining’s large exploration budgets. So, she’s got some amazing experience worldwide and brings that larger company philosophy, of which most of us have worked for in our careers but not for some time, from my point of view.

Then, of course, you can’t just have geologists. You’ve got to have other people around you, and Georgina Carnegie is more from the geopolitical side of things. She’s Harvard trained, World Bank, OECD, came out of the Australian government, and she really has helped me in many places in the world unravel the different onion rings of power as you work your way up through a country. She’s been fantastic at articulating those messages.

And then you need the engine room, of course, behind you in running these public companies. Nick DeMare, a long-term business partner, manages all the governance, and that side of the business. And once again, Mariana Bermudez, who sits in Vancouver, is our long-suffering corporate secretary, and makes sure that the business runs on a day-to-day basis.

And so, that’s really the team from the board and the offices. I should say the hardest workers, in many respects are those geologists, and we’ve got long experience in Peru. We’ve gone back to people, for the most part, that we know and know well. They’re the people and the drivers and the helpers in the field who are doing the hard yards finding all this copper.

Maurice Jackson: Mr. Hudson, I notice we overlooked a very important name. Could you please share who that is?

Michael Hudson: Well, a very important person indeed, and that’s Dr. Quinton Hennigh, who came to the company relatively recently, but has known the company and the story pretty much from the first press release we put out on this copper discovery. Quinton is an extremely well-known geologist. He’s probably one of the most famous geologists in North America for his ability to think big, to pick discoveries, and then to support teams in developing them.

From a personal point of view, I’ve really enjoyed working with Quinton. You don’t generally learn a lot in this business, and in the junior business, unless you surround yourself with some super people, and Quinton is just one of those people who’s taught me a lot from his vast experience base. Quinton is an advisor to the company. We were both down in Peru relatively recently together, and kicking the rocks. And his voice and experience is a tremendous advantage, and we love having him on the team.

Maurice Jackson: Having Dr. Quinton Hennigh is a competitive advantage in and of itself.

Michael Hudson: Exactly.

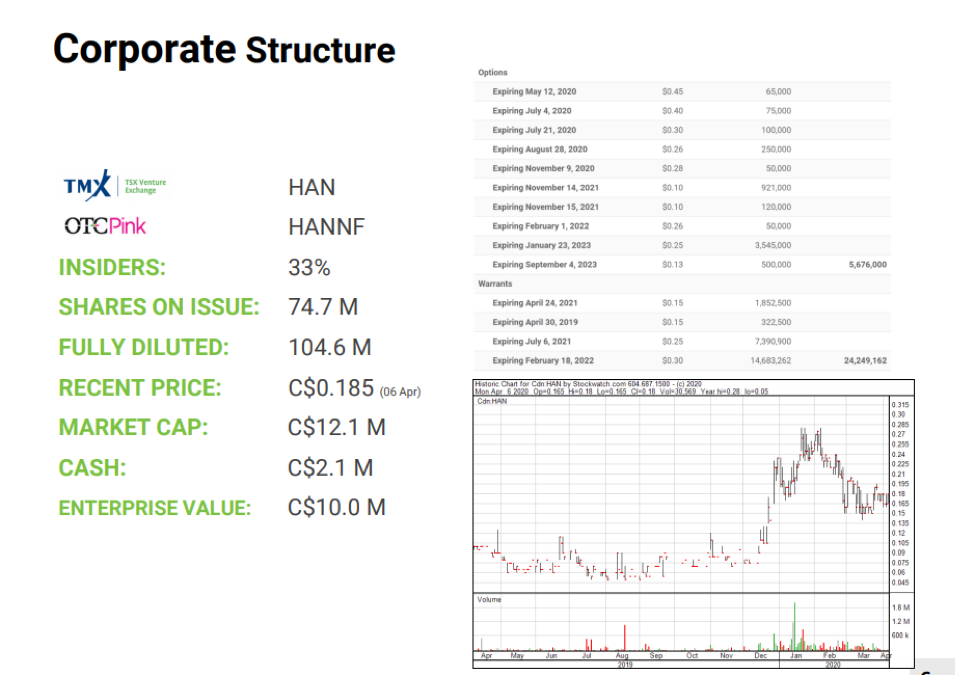

Maurice Jackson: All right, let’s get into some numbers. Please share the capital structure of Hannan Metals.

Michael Hudson: Well, we’ve got 74 million shares on issue; fully diluted around about 104 million shares. The market cap varies around $10–12 million at the moment. In terms of cash, we’ve got about CA$2 million cash in the bank. That will see us well and truly for this year’s budget, which was targeted to be $1.7M, of which we’ve spent some of that already. We were going to end with about half-a-million dollars cash after this field season.

That, of course, has been changed somewhat with this lockdown that we’ve seen now globally, where we try to avoid spreading this nasty virus, and Peru is no different. So, we just have to see where things go, until it’s appropriate and responsible to start our efforts again. But we’ll surely have enough cash in the company to get through to that first drill program that we spoke about.

Maurice Jackson: How much debt do you have?

Michael Hudson: Zero. If you take debt into one of these companies it’s a death spiral, and you really don’t want to operate with any debt as a junior explorer, in my humble opinion.

Maurice Jackson: Who are the major shareholders?

Michael Hudson: Well, we just completed a capital raise with $2M with the Sprott Group out of Carlsbad in California, and so they have a large percentage on their books. And then the other large percentage is actually insiders. It’s something like 40% of the holdings tied up between those two groups.

Maurice Jackson: I hope readers are taking note here. We’ve got Dr. Quinton Hennigh and Rick Rule: Those are two names that have given the endorsement to Hannan Metals, so I would certainly take note of that. And there are some other high-profile names that vetted Hannan Metals and are shareholders.

Michael Hudson: We have been fortunate to have some high-profile names as shareholders, such Bob Moriarty, Mickey Fulp, Brent Cook, Joe Mazumdar and Maurice Jackson.

Maurice Jackson: Are there any redundant assets on the books that we should know about?

Michael Hudson: Wow, that’s an interesting question. We still absolutely hold our Irish projects. But I wouldn’t call them redundant in any way, shape, or form.

Actually, we did some fantastic work there, and probably have some of the most compelling targets that have developed through lots of exploration, and lots of seismic acquisition actually. And that’s what gave us the real insight to going into this data in Peru, with all that petroleum data. That has inherent value rather than redundant value.

But the key point there is if we can keep those on the books with minimal expenditures, we’ve got such an exciting project here in Peru. There will be interest in those assets in Ireland, and we’ll determine just how to monetize those for shareholders as we go forward.

Maurice Jackson: Are there any change of control fees, and if yes, what is the compensation?

Michael Hudson: No, there’s none.

Maurice Jackson: That’s quite impressive actually. Is management charging a consultant fee for any services?

Michael Hudson: Yes. Myself and Lars have a salary. But I think that you’re probably hinting at, do we have a separate company that charges above and beyond, which is not the case. I take a very modest salary; something like CA$8,000 a month to run this company, which is probably one of the lower cost CEO salaries you’ll find in the business. But I truly believe in putting money in the ground. And I’ve got a lot of equity. I’ve written lots of checks for this company, and I’m in it for discovery.

Maurice Jackson: When was the last time you purchased shares and at what price?

Michael Hudson: I purchased shares right up and down from $0.25 down to $0.15 down to $0.05. So, I’ve purchased all the way up and down the chain there. In fact, myself and my business partners, along with Rick, were the only ones writing checks last year when nobody was interested.

Maurice Jackson: In a closing, multilayered question. What is the next unanswered question for Hannan Metals? When can we expect a response, and what determines success?

Michael Hudson: Well, we’ll continue to put out press releases over the next three or four months. We’ve got rocks in the lab. We’ve got rocks in our field camp that need to be sent to the lab once we can get back there. Then we’ll go back into the field when it’s a responsible time to do so. There’ll be continuous news flow despite the lockdowns that we see in Peru.

What will success be? Success will be further discoveries and confirmation of these areas over the larger area. It’s very early days, as I’ve said, and so we need to collect a hell of a lot more data to de-risk, and find a lot more of those outcropping areas, ideally, that we move toward drill targets, permitting those drill targets, and then demonstrating that continuity of grade. And I think if we can do that over the next year, where we’ve de-risked this project, and really proven at the next level, the opportunity here.

Maurice Jackson: Michael, what keeps you up at night that we don’t know about?

Michael Hudson: What keeps me up at night: That’s a really good question. What drives me is discovery! I live here in Australia. I have the benefit of waking up and seeing the day’s field results, so I’ll always take a look there before I have my morning coffee. What keeps me up is capitalizing these projects, or these companies, appropriately, and finding the right shareholders who share the vision. I suppose it’s not keeping me up at night, but it’s always an ongoing challenge, of course. And making discoveries in a timely manner that fits the needs of that capital. Often that’s very hard to do, of course, because everything always takes longer. I’ve been managing these companies because I love it.

I suppose the only other thing that I should say is just the safety of people. We’ve got field teams operating in these challenging environments, and even a slip of the ankle on a slippery stone is some of these areas. In jungle areas it’s tough to medivac someone out, so they’d have to walk out. Safety is paramount and it is something that I think about, as I have firsthand experience, having spent lots of time in those areas myself.

Maurice Jackson: Mr. Hudson, last question: What did I forget to ask?

Michael Hudson: You had very thorough questions, Maurice. So, I think we’ve covered a lot about the project, the people and the opportunity here, so I thank you for that. I suppose I want to say two things.

I think there’s huge opportunity here for the mining industry to be reshaped. It’s not a popular industry per se, in wherever you go in the world, yet everybody relies on something for mining. I hope there’s a greater discussion between society and the mining industry itself, to demonstrate that this is such an essential industry. In fact, it is an essential industry. It’s one of the few industries still going here in Australia at the moment, because if we didn’t produce the metals, we don’t have our mobile phones. We don’t have our washing machines, houses, in any sort of infrastructure.

As we decarbonize the world and go toward electrification, copper plays an extremely important aspect of that. We’re going to mine more copper in the next 20 years than we have for the whole history of the earth. New discoveries are really needed to meet supply, and this discovery plays into that narrative perfectly. And as I mentioned there before, this has a huge opportunity for Peru to create a completely new mining district in what is already one of the world’s most prolific countries from a metal endowment point of view.

So, I think there are just a few high level thoughts that I have. I thank you for your time.

Maurice Jackson: Well, thank you, sir. Mr. Hudson, for someone listening that wants to get more information on Hannan Metals, please share the website address.

Michael Hudson: It is www.hannanmetals.com.

Maurice Jackson: For direct inquiries, contact Hannan Metals at (604) 699-0202, or you may e-mail info@hannanmetals.com. Hannan Metals trades on the TSX.V: HAN | OTC: HANNF.

Before you make your next bullion purchase, make sure you call me. I’m a licensed representative for Miles Franklin Precious Metals Investments. We provide a number of options to expand your precious metals portfolio from physical delivery, offshore depositories, precious metal IRAs and private blockchain-distributed ledger technology. Call me directly at (855) 505-1900, or you may e-mail maurice@milesfranklin.com.

Finally, please subscribe to www.provenandprobable.com for mining insights and bullion sales.

Michael Hudson of Hannan Metals, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosure:

1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Hannan Metals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Hannan Metals is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Images provided by the author.

( Companies Mentioned: HAN:TSX.V; HANNF:OTCPK,

)

Source: Michael Ballanger for Streetwise Reports 04/13/2020

Sector expert Michael Ballanger offers his take on how investment tactics have changed over time, as well as on recent market moves.

Back in the Dark Ages, before cellular phones and the Internet, I was studying to complete the Ontario Securities course one afternoon when I came across the part discussing “asset allocation” and “portfolio construction.” This section covered the recommended mix of bonds and stocks, and everything revolved around the word “risk.” When the customer was in early adulthood, they advised being overweight stocks and underweight bonds, and as the customer matured toward middle age and retirement, the weightings slowly reversed, resulting in an entirely fixed income portfolio generating returns of around 10%.

In other words, a $1,000,000 pool of retirement capital threw off $100,000 of annual income upon which to comfortably retire. With that kind of return, there was little need for the risk associated with stocks, and proof of that was the firm for which I toiled, McLeod Young Weir Ltd., known primarily as a “bond house” with the vast majority of their operations and research geared to fixed income.

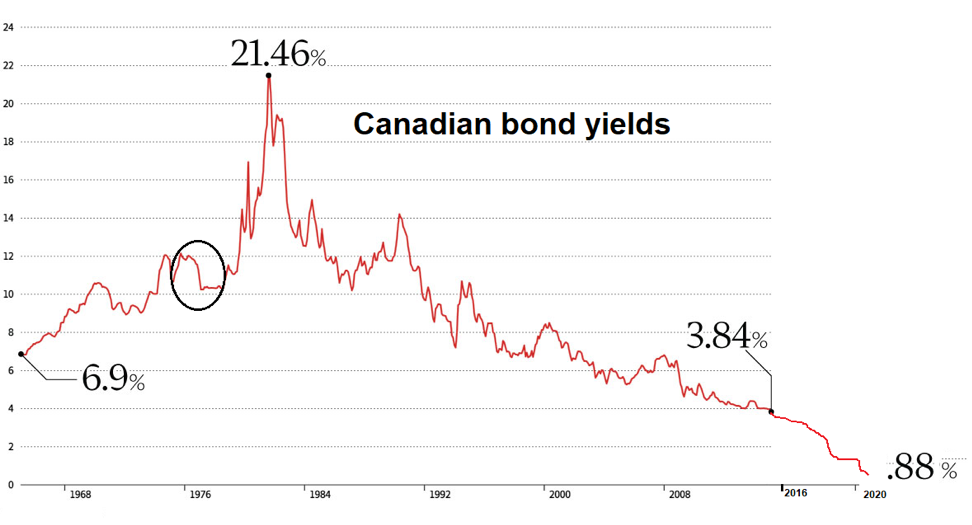

However, over the years, as central bankers gained more and more sway over policy and as bond yields began to sink, the importance of the risk-free return as a benchmark for performance was replaced by more aggressive styles of portfolio construction. Though “financial engineering,” new products driven by derivatives and leverage were designed to augment these diminishing yields, and instead of investing their $1,000,000 of retirement capital with the “lender of last resort,” the Bank of Canada, retirees today are forced to follow the advice of the financial wizards of Wall and Bay Streets. They invest in alternative products or outright stocks and, in doing so, move from “risk-free” to “risk-fraught” and very uncertain returns. As you can see from the chart shown above, $1,000,000 invested today generates a 0.88% return, or a paltry $8,800 of annual income, which is pathetic.

More importantly, after the shellacking taken by stocks in the last quarter, coupled with the 2008 financial crisis, the new mantra for retirees is no longer return on capital, but rather the certainty of a return of capital as the paramount consideration.

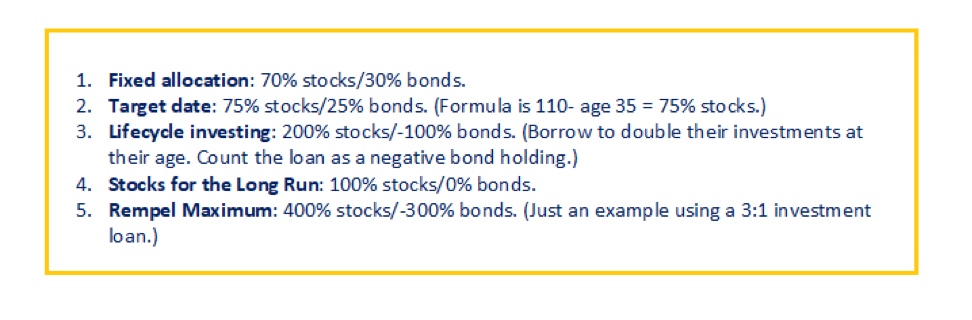

I did an ad hoc Google search of “asset allocations,” and arrived at the following example of a few different types of allocations. You can see that all of these include stocks, with the most outrageous being the Rempel Maximum, which has a person leveraged to the gills to own stocks. Imagine the poor retiree that must generate income by moving to stocks, who is today down 17.1% year to date (TSX Composite), which amounts to a loss of $171,000 on his million-dollar nest egg. Now that’s “real money.”

Where I am going with this train of thought is simple. Nowhere in any of these “models” is there an option for precious metals. It is either Door #1 to Hades, or Door #2 to Purgatory. I can go “overweight” risky assets and “underweight” riskier assets, or vice-versa, but at the end of the day, I have a retirement fund made up of risky paper.

Thanks to the wizardry of central banking and financial engineering, prices for things that used to be the domain of the natural flows of capital, driven purely by the forces of demand and supply, have become pre-set, orchestrated prices that are either suppressed (as in gold and interest rates) or inflated (as in stocks and real estate and anything else vaguely resembling banker collateral). This unnatural interference in the flows of capital is diabolically dangerous, and it the reason why we are seeing these grotesque moves by the ever-merging life forms called the U.S. Treasury and the Federal Reserve. What I saw last week was beyond surreal, and it is not going to end well.

There was a revealing interview on CNBC last week in which the guest, a money manager named Chamath Palihapitiya, tells the anchor (Scott Wapner) that there should be no bailout of the airline industry. The anchor asks, with a pained expression verging on abject horror, “But you would let all these people lose their jobs?” The gentleman then proceeds to lay to waste any and all shreds of credibility in the CNBC clown by explaining to him what happens when a company goes bankrupt, and how the employees actually benefit in some cases, and how the only losers are the speculators and the unsecured debt holders that gambled in the first place! It was priceless, and it was exactly what I wrote about in 2009 when all the billions of bailout dollars rescued the speculators and riverboat gamblers in the U.S. banking business and threw homeowners under the bus.

The numerous tweets I sent off late last week were an effort to wake more than a few people up to what is turning out to be the Second Major Financial Heist of the New Millennium. The banco-politico alliance is once again remembering to “never let a good crisis go to waste,” and are lining up at the trough again to gorge themselves on taxpayer slop. It drives me to absolutely madness.

Moving on to the markets once again, it is imperative to understand one thing before I proceed. The stock market is, for the current U.S. president, not only “of interest;” it is an obsession. Because of this, and because of the current panic gripping the Fed and the Treasury, aided and abetted by the mainstream media, I have zero confidence in the effectiveness of either technical or fundamental analysis of the financial markets here in April 2020. The lines dividing the executive and legislative branches of governments around the world have become blurred, and the fallacy of Fed “independence” has been shown for what it is – fallacy.

The specter of a prolonged bear market brought on by the government lockdown is the logical projection based upon the initial economic feedback and history, but as these are not normal times. As this is an American election year, with a global pandemic surrounding them, these are, in fact, extremely abnormal times. The $6 trillion Fed balance sheet and the Congressional act granting $2.3 trillion in stimulus funding is testimony to the urgency of rescuing the stock market (and voters), so betting heavily on a resumption of the downturn in stocks is unwise at the best, and a fool’s folly at worst.

Similarly, expecting that gold and silver are going to be allowed to move to unfathomable heights unimpeded by the invisible hand of the banco-politico alliance is equally naïve. While conditions supporting such a move are ideal, covert operations designed to nullify such a move have been used in the past.

That said, the Dow Jones had the best week since 1938 last week, and CNBC must have flashed it fifty times Thursday afternoon before I turned off the set. Of course, that 1938 rally was a classic bear market rally, with the ultimate lows coming in 1942. The Fibonacci study I did back in late March suggested that the 2,655–2,797 range was the most logical distribution zone for the rebound to end, but it doesn’t rule out an extension move toward 2,940.

The rebound itself comes as no surprise to my subscribers; the CNN Fear-Greed Index hit an unheard-of reading of “1” around mid-March and has now risen from “Extreme Fear” to just “Fear” and a “43.” Give me a few more Trump tweets and Mnuchin messages; throw in a pinch of Powell pressers, and we will be north of 50 and back in the “Greed” mode, with all systems “go” and stocks a-chargin’.

I am very modestly short the SPY, from $272 and a 50% position in May put options, but it is an outright “punt” on a retest and taken from the “Crash 101” textbook. I “should” get a retest, but with the New York Fed putting in triple overtime, it might get “bypassed” as it did in 2019.

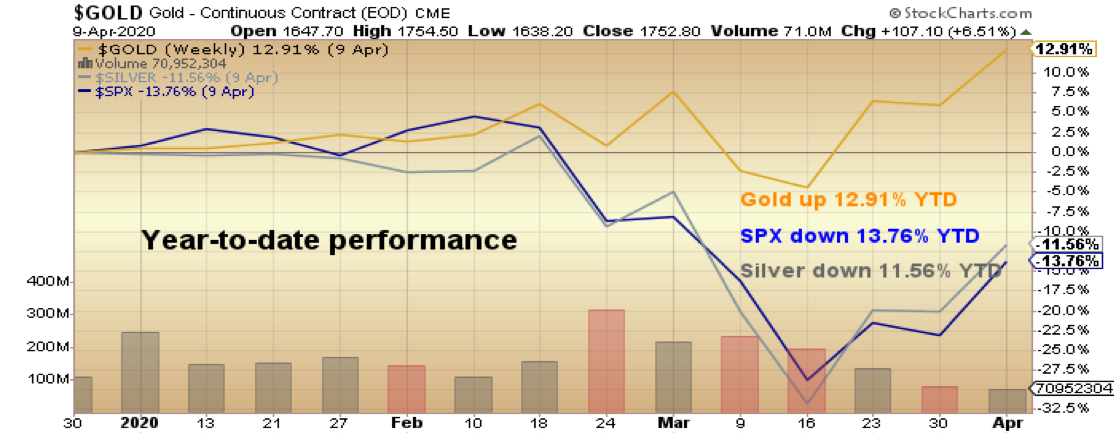

The big news on the week was the new eight-year high registered in gold, and despite the $10 pullback after the close of the pit session, the technical picture looks impressive, verging upon exciting. The HUI had an equally impressive move to 232, going out near the highs of the day and week. However, interestingly, the HUI:Gold ratio remains 20.9%, below the level it hit in late December when gold was priced $120 lower at $1,530/ounce and 59.8% lower than in August 2016, with gold at $1,371/ounce. If gold miners were valued relative to gold prices at the 2016 levels, the HUI would be 371, which is 55% higher then we are today.

That is the reason that I added to positions taken three weeks ago after I posted the two “Generational Buying Opportunity” charts of the Senior Gold (GDX:US) and Junior Gold (GDXJ:US) Miner exchange-traded funds (ETFs). If you assign 2016 valuations to GDX and GDXJ, you get $45.12 GDX and $55.25 GDXJ. In fact, although I took a few trading account shekels off the table into the advance, I still hold August calls in GDX from that Monday morning when it gapped down to $16.18, and I still have 133 days until expiry, which is cool.

They say that entry points are the key to successful speculation, whether it is real estate or stocks, so whenever you get panic as thick as it was in mid-March, you have to ignore CNBC and BNN and your “wealth advisor,” and close your eyes, pinch your nose, and buy.

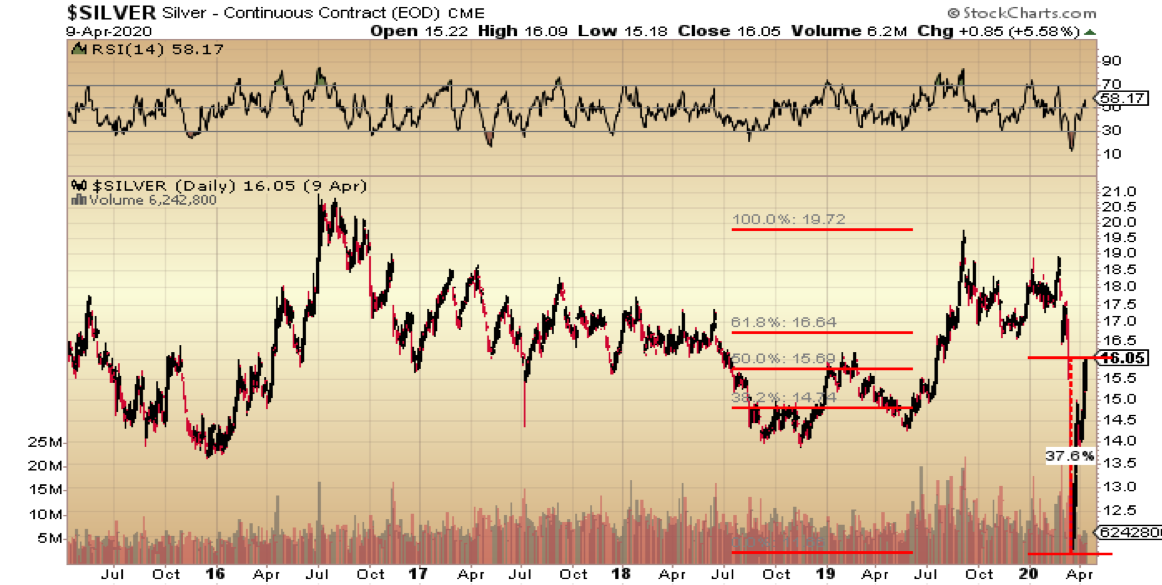

Silver remains an enigma, although it has advanced over 37% off the lows. It has also cleared the first two Fibonacci levels, with only USD $16.64 remaining as a hurdle.

Much as I love silver, I also hate silver, because it is the most easily tampered-with pricing mechanism in the history of commerce. While we all like to think of silver as the “poor man’s gold,” it is still suffers from 57% industrial demand versus only 8% for gold, so when the world goes into a viral lockdown, silver demand plunges off a cliff, and price with it.

I am still rethinking my position on silver and how to play it for the rest of the year, but the challenge lies in this: If I opt for added alpha by going for the huge leverage and added volatility of silver, I sacrifice the certainty of being on board gold, whose fundamental and technical set-ups are spectacular. I like the certainty of gold, but I also love the excitement of a rampaging short squeeze in silver. I have been through two of them, in 1980 and in 2011, and came out with my arms, legs and face intact, and only minor damage to my liver. The exhilaration of the silver ride is matched only by the violence of its terminus, and the attendant piles of malodorous body bags at the side of the trading pit. Surviving one of them is tantamount to three tours of duty in an Asian jungle armed with a broken hockey stick and a roll of tape.

I made a prediction on Twitter last week, which is this: “Give me a 2-day close above USD $1,750 in gold and I’ll show you a $2,000 price by Queen Victoria’s birthday.” For those heathens unfamiliar with the Great Queen Victoria, we Canucks celebrate her date of birth every May 24 weekend, usually with great vigor and always with great respect. As it is usually the first chance to get the first real sunburn of the year after a grueling winter, we affectionally nicknamed it the May “Two-Four” weekend. That’s because, back in the day, every Friday included a lineup at what was called, a few decades back, “The Brewer’s Retail,” and the hard-core “players” came out of the store with a case (or several) of twenty-four bottles of Molsons or Labatts beer, affectionately and appropriately called “The Two-Four.” You didn’t order a “case” or a “dozen” or a “six-pack;” the real players ordered a “Two-Four,” and because the first really fine spring weekend of the Canuck year is usually a long weekend spent at some poor lad’s parents’ cottage, you always arrived (invited or not) with a “Two-Four.” More often than not, one left with only a few “empties,” so as to not burden the host, but that is the reason most Canucks refer to this holiday as “The May Two-Four Weekend.”

So, as is customary of the upcoming festive part of May, I raise a glass both in advance and in salute of the breakout in gold prices and the birth date of the regal Lady from whom the phrase “We are not amused” found its origin.

The last thing to discuss, notwithstanding the Herculean efforts of Bill Murphy and Chris Powell, founders of GATA, is that, at long last, we are finally witnessing the fruits of labor drawn from the hearts and loins of true believers in “free market capitalism,” the identity of whom you will be hard-pressed to find in today’s banco-politico alliance.

The domination of the mainstream media (MSM) by the owners of digital, literary and monetary printing presses, can only be described with one adjective—vile. The true role of gold has always been to protect wealth and was never meant to be a cognizant threat to the U.S. dollar because the Founding Fathers, who drafted the American Constitution, designed it that way. They knew precisely the outcome of uncontrolled and opportunistic politico-banco alliances, which was why they built currency debasement safeguards within the document.

But, as is always the case, over time the documents gets subverted through Constitutional “amendments” that are argued in defense of “modern conditions.” These “modern conditions” are at the very heart of why societies move from “free” to “enslaved,” because the elite would have you all believe that moves they are allowed to make and laws they are allowed to break are justification for outcomes rarely intended and never expected.

The indiscriminate trashing of the domestic currency of any country is a crime in over 90% of the globe’s sovereign countries. but laws protecting currency debasement are waived when the perpetrators are politicians or bankers. The average citizen goes to jail while the banco-political alliance is applauded. Abominations like this have only one defense; you don’t play their game. You have to pay your bills with dollars or euros or yuan or yen, but you don’t have to invest in them—and nor should you.

Looking out on the horizon, you must realize that the vast majority of portfolio managers around the world have, for decades, been managing money without any exposure to precious metals. In that context, gold has been an orphan, under-owned and unloved in a relative sense. With the trillions upon trillions of investible assets having ignored the space for so many years, there remains an entire generation of managers only just waking up to its portfolio utility. Having gold up 12.91% year to date has allowed those very few advisors to protect their client assets, but they are so rare that they represent a tiny fraction of the fund flows that move markets.

As soon as the Q1 performance numbers begin to surface, I predict a tsunami of new money flooding into the precious metals space. We are already seeing it, with gigantic volume and percentage moves in the big boys like Newmont Goldcorp Corp. (NEM:NYSE) and Barrick Gold Corp. (ABX:TSX; GOLD:NYSE), but when all of these imitative and herd-mentality fund managers get the memo, trillions of dollars will be chasing a very small and completely underowned sector. When this Hadrian’s Wall of demand hits the Lilliputian paucity of supply, precious metals producers, developers and explorers are going to experience exponential price moves that will dwarf the moves seen in 1976–1980 and 2002–2011.

Make sure you have your positions, because you won’t recognize these prices by the time summer rolls around.

Originally published on April 10, 2020

Follow Michael Ballanger on Twitter @MiningJunkie.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Newmont Goldcorp, a company mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.