Gold Mine-Sponsored Digital Asset, Moria Token, Launches on the IDEX International Exchange Business Wire

Month: March 2021

- Gold Price Forecast – Gold Markets Looking Upwards FX Empire

- Gold prices end at a 2-week high ahead of Fed decision MarketWatch

- Gold eases on firmer dollar; Fed verdict eyed CNBC

- PRECIOUS-Gold firms as dollar, yields retreat; palladium hits 1-year high Reuters

- PRECIOUS-Gold muted as markets wait for U.S. Fed meeting Nasdaq

- View Full Coverage on Google News

Gold loses modest early gains on bearish outside markets Kitco NEWS

Gold futures up a second session, at highest in 2 weeks MarketWatch

Ray Dalio on ‘shocking’ tax changes: Could see new ‘prohibitions’ against gold, bitcoin Kitco NEWS

Gold and Silver IRA Guide Published Gainesville News

Categories

Is Inflation or Deflation Coming?

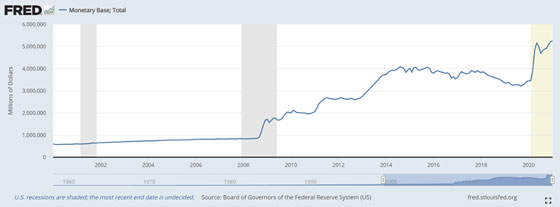

By the M0 measure of the money supply, there was a 52% increase between February 2020 and January of this year. This is a graph of M0 going back to 2000.

There. Proof of the coming hyperinflation. It took centuries to get to $3.4 trillion monetary base, and less than a year to increase it by over half. QED. This is all you need to know!

At least, so say those who are certain that prices are set to skyrocket. And who, of course, also say you should buy gold as it will skyrocket too.

On the other side, the hacks and apologists for the central bank and deficit spending argue there’s nothing wrong with the current monetary and fiscal policies. Paul Krugman, in this debate, asserts (in between many weasel words) that the Biden $1.9 trillion spending package won’t cause much inflation.

A Bank of America survey seems to confirm this, finding that 64% of people planned to pay off debt, save, or invest their $1,400 checks. The rich are not going to receive anything, so this response is showing the middle class is not planning on living large with this largesse.

One ugly fact is that the price of oil has shot up to $65. And the twin to inflation is rising interest rates. The 10-year Treasury yield has spiked up to 1.6%. Do these data points not argue for accelerating inflation?

At the same time, most car commercials advertise 0% interest for 5- or 6-year loans. This is not only a data point for lower interest rates—what would the Treasury have to be, for consumer credit to be zero interest?—but also for soft prices. The price of the car may not be discounted that much, but zero interest is a subsidy worth an additional thousands of dollars per car.

A Glaring Fallacy

Krugman argues that giving unemployed people free money is not stimulative. By the implication of his economic theory, this means non-inflationary. His reason is that it is simply replacing the income that people would have gotten, if they had been employed. And therefore, it is not giving them additional purchasing power.

The fallacy in this is so glaring, that we expect a precocious eight-grader could see through it. When those people were working, they were producing goods and services. Now they are paid the same, but producing nothing. That is, welfare checks prop up demand but lockdown cuts down supply. If supply falls but demand remains the same, we would expect higher prices.

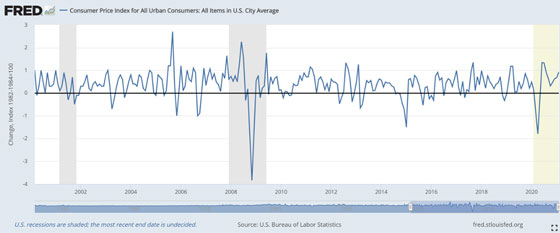

We see it in certain goods. The Consumer Price Index has perked up these last few months. But look at this chart, going back to March 2020, showing year-on-year change in the CPI.

This data is through last month. The inflation number has not gotten out of range, despite the breathtaking increase in the monetary base. Any argument for extreme inflation will have to say, in essence, “yes, but it’s coming”.

Is it? Before we get to that, we encourage the reader to think about all the previous times that the commentariat got excited during this long period of falling interest rates, telling us that a big inflation is coming.

Another thing we often hear, especially in the alternative investments community, is that the official CPI measurement is a lie. It’s not a lie. It’s something else.

Some debate what goods ought to be in the basket measured by CPI. And what product ought to replace one that becomes obsolete, such as buggy whips. These quibbles are the inevitable result of the fundamental confusion built-in to the nature of the index. The CPI violates a law of arithmetic that we all learned in fourth grade.

You cannot add apples to oranges.

The CPI does not only add them, it averages them. An average of two numbers is (A + B) / 2. So, of course there will never be agreement on which goods are included, or the proper weighting. And therefore, on what the right number for inflation is.

But one thing should be clear. You could not obscure a massive drop in the value of a dollar, just by switching one consumer good for another in the CPI basket of goods.

Prices & Interest Rates

We have often written about the fact that prices move with interest rates. The relationship is not merely correlation. It’s causal (Keith will be presenting his radical theory of interest and prices at the Mises Institute Austrian Economics Research Conference this week, in Auburn, AL).

When interest rates fall, it lowers the cost of borrowing. At any given moment, there are many businesses that are considering borrowing to expand. Or borrowing to buy equipment to replace labor. But at the current rate of interest, it doesn’t work. What happens when the interest rate drops?

Their business case then becomes sound. So they borrow to increase production. This puts downward pressure on prices. Think of what happens if the supply of hamburgers increases, while demand remains the same. The price of a hamburger drops.

Falling interest has been the trend since 1981. But prior to that, we had rising rates. During that period of rising rates, producers who planned to borrow money to replace worn out capital equipment found that it didn’t work at the new, higher rate. However, what did work well indeed was to borrow to buy raw materials. And to borrow to finance work-in-progress, a buffer of partially completed goods in between each step of the manufacturing process.

In a period of rising rates and prices, the longer it takes between when a company buys the ingredients until it sells the finished goods, the more profit it makes. Thus they have incentive to borrow more to carry more materials in their warehouses.

This definitely does not describe the present environment.

Today, the monetary forces are pushing prices down. However, there are three nonmonetary forces that push prices up: regulatory, fiscal, and social.

Prices & Useless Ingredients

We have written many articles about mandated useless ingredients. This is when the government forces gasoline companies to add ethanol or MBTE. These additives push up the cost of petrol (we have read numbers around 25 cents per gallon). Gas is a low-margin commodity, and an increase in the cost per unit causes an increase in the price to the consumer.

Useless ingredients are being mandated all across the economy: supply-chain tracking, bathrooms compliant with the Americans with Disabilities Act, calorie labels on every item on restaurant menus, minimum wage and other labor laws such as the forced hiring of extra workers, umpteen airbags in automobiles, etc.

Some of these things may be good, and might have been chosen by free actors in a free market (though not in the rigid, unthinking, and expensive ways forced by regulators). However, the point remains. These are costs that do nothing for consumers. Most people don’t even know about them. They just say, “wow, the price of gas went up.”

Prices & Fiscal Policy

Fiscal policy works similarly. It adds cost, and hence pushes up prices, but few people are aware of it. Speaking of gasoline, we observed a gas tax hike in California a while back. We thought that, once people forgot about the tax hike, they would just think of the rising price of gas as part of inflation.

No discussion of forces that push up prices would be complete without discussing a deliberate reduction in supply based on social concerns. We refer to the government response to Covid. Looking just at the meat industry, forced plant closures reduced supply of meat last year. Since demand for food is quite inelastic, the price had to rise dramatically in order to force the marginal consumer to eat less meat.

We realize that the mainstream includes all causes of rising prices in their definition of inflation. However, regardless of the words used, we differentiate these nonmonetary forces pushing up prices as opposed to the monetary forces pushing them down. This distinction is important, especially if we want to predict what comes next.

This is because a monetary force not only cause prices to move, but the resultant price move transmits feedback to that monetary force. It’s a positive feedback loop. It tends to keep running in the same direction for a long time.

By contrast, nonmonetary forces are one-time events, that cause one-time price adjustments. A 25-cent gas tax causes a 25-cent (or 23- or 26-cent) price hike. But there is no further motion after that, unless the legislature meets again.

“Yes,” some will say, “but interest rates have been rising.”

Categories

Celebrate the Return of the Golden Bull

Source: Michael Ballanger for Streetwise Reports 03/15/2021

Sector expert Michael Ballanger considers how recent market moves have influenced investment in the precious metals markets.

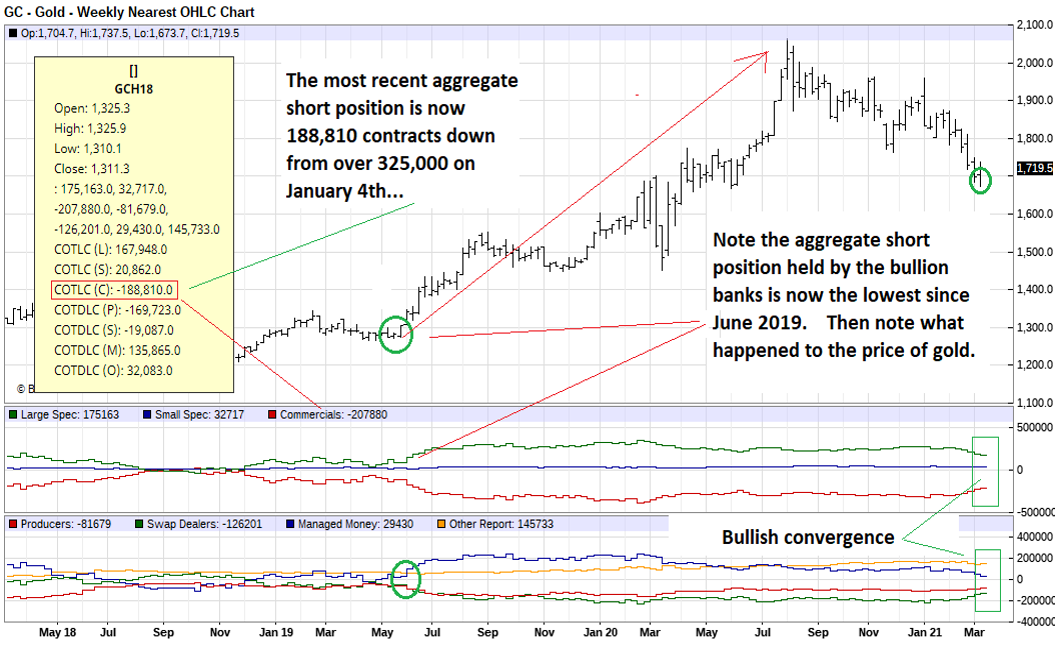

I had not intended to hit the keyboard today, having worked all week to prepare the Special Situations Report on my top-performing Norseman Silver Ltd. (NOC:TSX.V) (whose 65% year-to-date advance and 869% advance since the March 2020 lows has been a pleasant surprise), but Friday’s COT (Commitments of Traders) report grabbed me by the throat and slammed me into the chair.

The bullion bank behemoths that manage gold prices in the Crimex futures pits are particularly adept at bullying, and unlike the schoolyard, where bulging biceps and menacing unibrows command fear and obedience, it is the bulging wallets that send the meek scurrying for cover. I have watched the COT over the years, and whereas I used to make all trading decisions from the COT numbers, that has tempered somewhat since the world went into “manic mode” with the arrival of that nasty flu bug a little over a year ago.

Had I let the actions of the bullion banks be the sole determinant of my trading decisions last March, the 375,000-contract net short position would have sent me screaming under the bed. Fortunately for me (and those that follow me), other inputs weighed in heavily and it was the weekend of March 14–15 of last year that I ignored the Commercials and went “all-in.” As they say, the rest is history. The biggest rally in the miners in many years ensued and one of the best performance years since 2011 unfolded, and continues here in 2021.

However, it was November 2015 that the movement of the Commercial Cretins was critical to identifying the end of the 2011–2015 Great Bear Market in gold, silver and the precious metals equities. For a very brief period in very early December of that year, commercial traders actually went long the Crimex futures markets (and they never go long), after covering shorts week after week from late summer right up until the end of November.

Back then, it was not only the number of aggregate shorts but also the ferocity of the directional move that was the “tell”; the bullion bank behemoths were relentless buyers displaying a highly abnormal behavioral bias that was the “starter’s pistol” for the new bull market in gold.

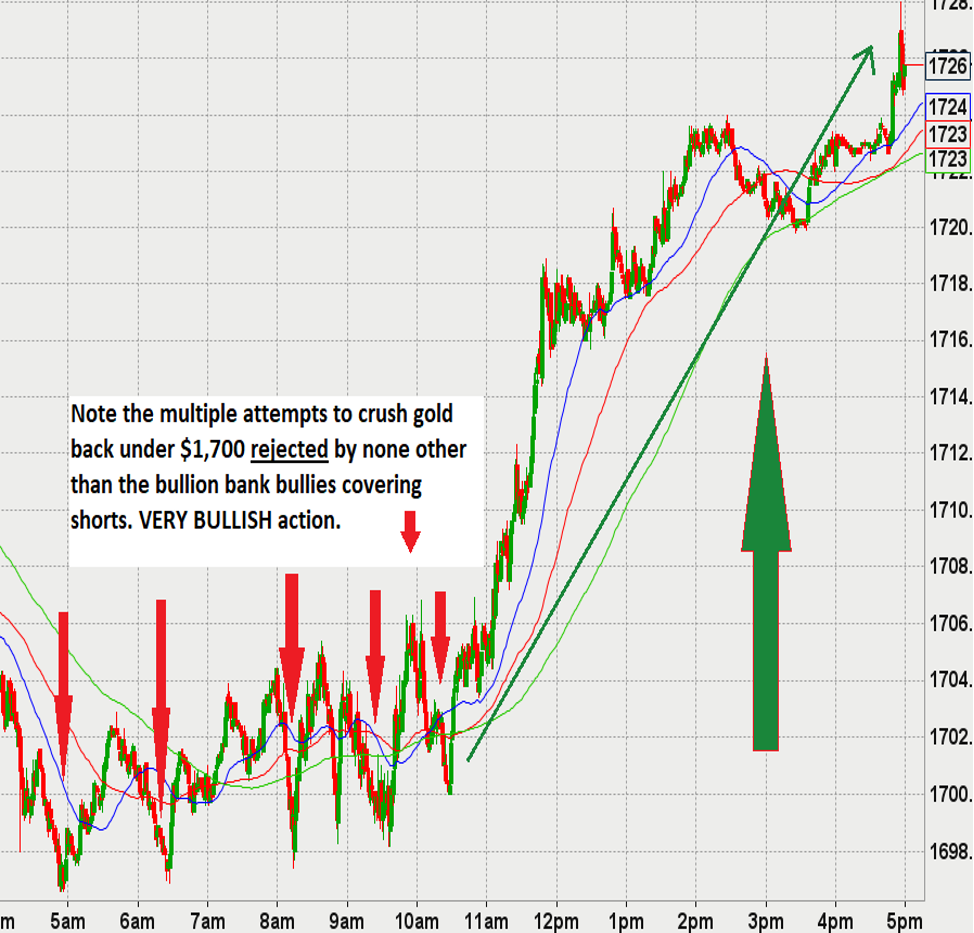

Because I issued a “BUY” on gold last Monday morning at US$1,680 (only after generously self-medicating during breakfast), I decided that I wanted to add to the positions, but before doing so, I wanted to do some work on the COT. So, I made a note to pick up the 3:30 p.m. bulletin to get a sense of just how urgent the bullion banks had become in their newfound bullish bent. The chart you are looking at is not an “End of the Bear Market” type, but more of an “End of the Correction” type, with aggregate shorts held by the bullion bank bullies collapsing at a rapid rate into last Tuesday.

Now, we will not get the action from Friday’s $25 air pocket until next week, but watching April Gold move late day from US$1,696.60 to US$1,728.00 reeked of desperation from those that are short wanting to be “less short,” with little time to do so. It had all the malodorous trappings of the Commercial Cretins.

I maintain that the lows for the correction are now behind us and that you can reload your favorite gold miners with reckless abandon. I continue to favor the developers and want to point out that GGMA favorite Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) has now finally caught the “correction bug,” and now sits 30% from its 52-week high. Mind you, it is still ahead 340% from the March 2020 lows and trades at US$21.75 per ounce of in-ground gold, with the benchmark for “ounces in Nevada” at US$100. Since they are growing the resource through drilling, I see the current price as a gift and will be adding shortly.

While the rebound in energy prices has a number of the gold bugs all giddy about the inflation outlook, I would prefer that the number one cost input for the gold miners be moderating rather than spiking. It is important to remember that the 2001–2011 Commodities Supercycle, involving the Great Chinese infrastructure boom, included $100/barrel oil, and that was a margin pinch for many of the gold miners and the number one reason they underperformed after 2007.

My trusty Rottweiler (Fido) has also provided an important “BUY” signal this week, as he has returned from his sanctuary under the tool shed, having avoided flying wine bottles and quote monitors that usually represent hazardous impediments during gold corrections. Bullseye targets with dart-ravaged images of bullion bankers and central bankers and investment bankers are now concealed from view and, with the window to the courtyard now repaired, the inhabitants of this abode are safe from the maniacal ravings of this author, always welcomed but rarely trusted by all.

And I can’t really blame them.

Originally published March 13, 2021.

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at miningjunkie216@outlook.com for subscription information.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold, Norseman Silver. My company has a financial relationship with the following companies referred to in this article: Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Getchell Gold. Please click here for more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold and Norseman Silver, companies mentioned in this article.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

( Companies Mentioned: GTCH:CSE; GGLDF:OTCQB,

NOC:TSX.V,

)

Categories

Poland Wants More Gold

Poland’s gold-buying spree isn’t over. In 2018, the National Bank of Poland began aggressively adding gold to its reserves. Through the first half of 2019, the Polish central bank added more than 100 tons of gold, nearly doubling its reserves. So, why did Poland decide to significantly increase its gold hoard? In a nutshell, to […]

The post Blog first appeared on SchiffGold.

What is the ballooning trade deficit telling us about the US economy? Peter Schiff recently appeared on NTD News to talk about it. He said the US has never been worse on trade and it is a sign that we don’t have a recovering economy. In fact, we have a phony economy in danger of […]

The post Blog first appeared on SchiffGold.