- Gold slides over 1% after Fed projects rate hikes into 2023 CNBC

- Gold price plunges $40 as Powell says inflation will be like the ‘lumber experience’ Kitco NEWS

- Gold prices post first gain in 4 sessions, move lower after Fed update MarketWatch

- PRECIOUS-Gold treads water ahead of Fed policy statement Reuters

- Gold Price Prediction – Prices Drop as Yields Surge FX Empire

- View Full Coverage on Google News

Month: June 2021

‘Best time to buy gold is before crisis’: watch inflation risk and $3K gold price target, says industry expert Kitco NEWS

Gold prices to average $1820 in 2021 – Metals Focus Kitco NEWS

Gold settles higher, then moves lower after Fed policy statement MarketWatch

What will today’s FED decision mean for gold and Silver Kitco NEWS

Source: Peter Epstein for Streetwise Reports 06/15/2021

Peter Epstein of Epstein Research believes Golden Independence Mining Corp. could be an M&A target for a major with a neighboring prospect.

Note: Golden Independence Mining Corp. (IGLD:CSE; GIDMF:OTCQB) is earning into a 75% interest in the Independence gold project. It’s assumed for the purposes of this article that the company achieves an initial 51% interest later this year. Golden Independence will then have three years to earn up to an additional 24%, by spending a total of US$10 million ($10M) more on exploration/development.

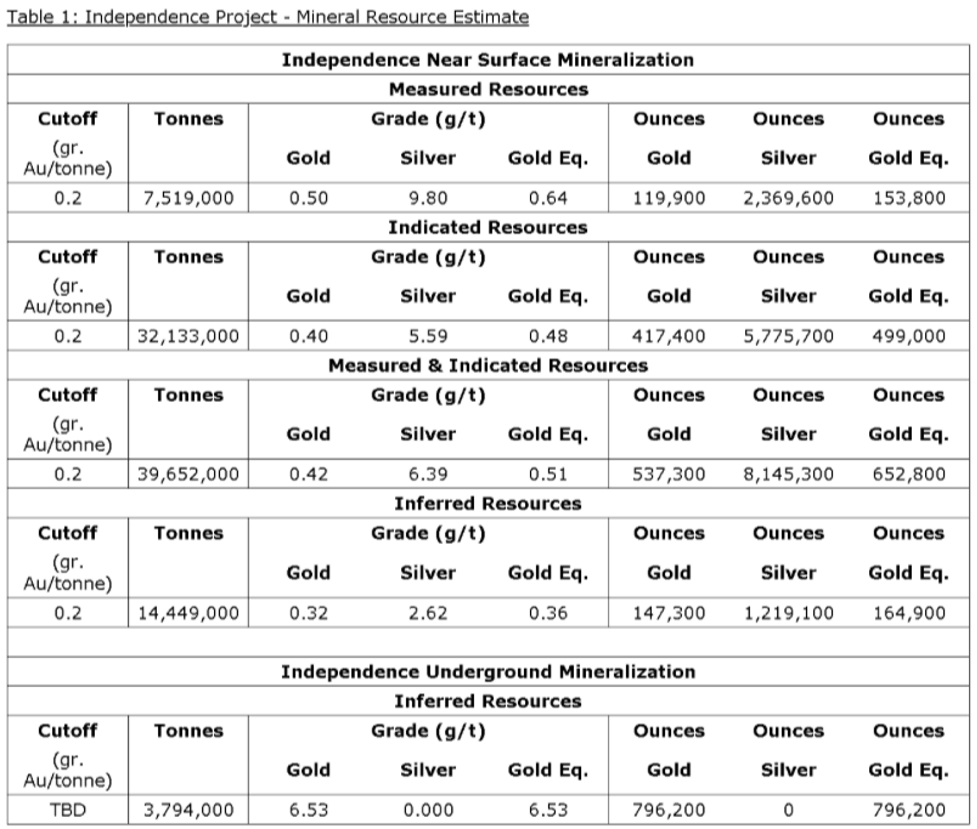

Golden Independence Mining Corp. is well underway in its efforts to earn (up to) a 75% Interest of a brownfields project in Nevada. Last month, management delivered a NI-43-101-compliant mineral resource estimate of 684,600 Measured, Indicated and Inferred ounces gold (plus 9.4 million ounces silver [9.4 Moz]) on a 100% project-level basis. Including silver, that same figure, in gold equivalent ounces, is 817,700.

Another resource estimate and a preliminary economic assessment (PEA) are expected by year end. As a reminder, the project’s 796,200 (Inferred) deep underground ounces, (grading 6.53 g/t gold) will not be incorporated into the mine plan of the upcoming PEA.

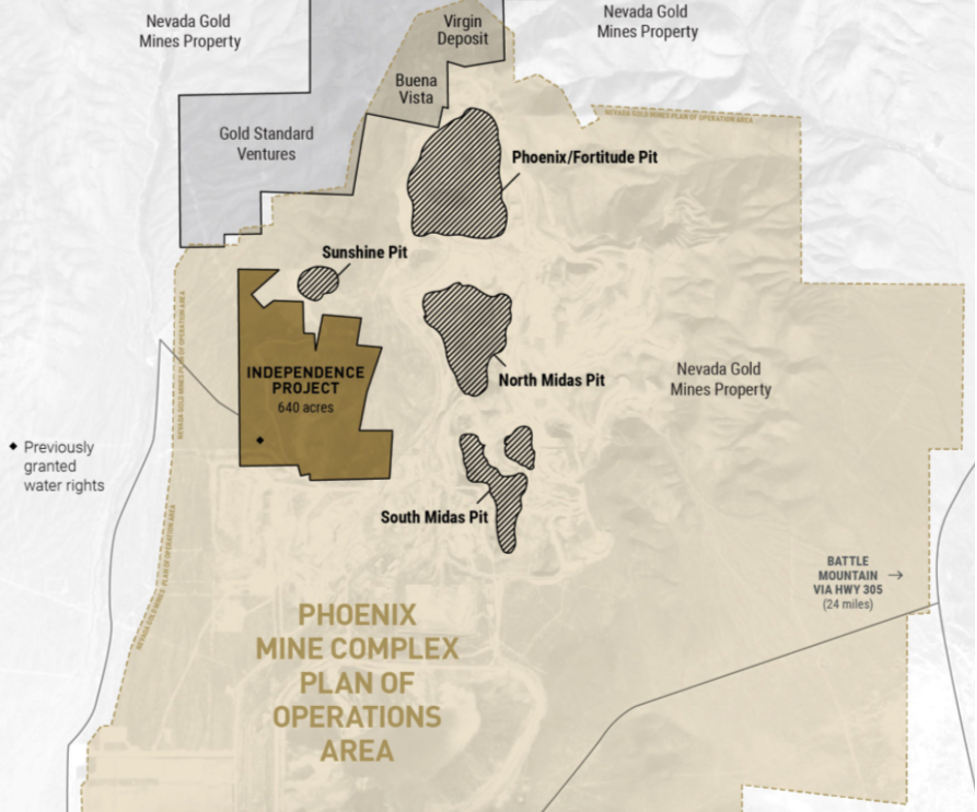

The property benefits from >$34M in past exploration, including over 210 holes drilled. It’s adjacent to Nevada Gold Mines’ (NGM) Phoenix-Fortitude mining operations, (~180,000 ounces/year at an attractive AISC of ~$1,000/ounces) just 0.5 kilometers (km) to the southwest, on the Battle Mountain-Cortez trend.

In fact, it’s more than adjacent, the property sits inside NGM’s Environmental Impact Statement and Permitted Plan of Operations. NGM is a 61.5%/38.5% joint venture (JV) owned by Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) and Newmont Corp. (NEM:NYSE). NGM is a major: It will produce ~3.5 Moz of gold this year; it has 12 open-pit mines and 10 heap leach facilities.

This location is ideal, near majors NGM and Kinross Gold Corp. (K:TSX; KGC:NYSE) and mid-tiers Coeur Mining Inc. (CDE:NYSE) and Hecla Mining Co. (HL:NYSE), in a brownfields setting, in the heart of Nevada’s incredible gold and silver abundance. Did I mention that Nevada ranked #1 of nearly 80 global jurisdictions in this year’s Fraser Institute Mining Survey?

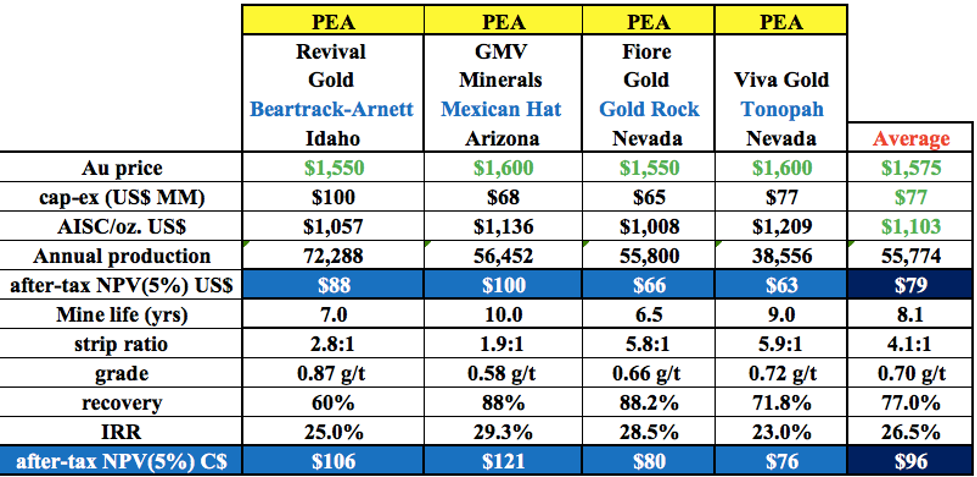

Management is pursuing a simple, low-risk, heap leach project that (subject to a PEA) could produce ~50-70k ounces of gold/year for 7–9 years. Based on four peer heap leach projects in the western U.S., all at PEA stage, it seems reasonable that Golden Independence’s property could develop into a project with an after-tax NPV(5%) of CA$90-$100M.

However, the heap leach approach could be replaced with an entirely different, much more sexy project, if gold prices remain elevated. In addition to soon owning 51% of the shallow open-pittable resource, Golden Independence has a much deeper mineral resource of 796,200 (Inferred) ounces of gold. These ounces carry a grade of 6.53 g/t.

So here’s the thing about those high-grade, much deeper ounces—they’re valuable as a starting point to what could become a larger deposit. However, they’re worth tremendously more to a mid-tier or major with the cash to drill dozens of very deep holes.

If only there were a large giant gold producer nearby that might be interested in 6.53 g/t gold material… Wait! Of course there is, that would be NGM. There’s a slight problem though.

It’s safe to assume NGM would not want to get involved with the project unless/until it was 100%-owned by IGLD. With that in mind, management will be trying to strike a deal to obtain 100% ownership sooner rather than later. As it stands, IGLD has three years to earn into a 75% Interest.

I said earlier that the heap leach plan could be scrapped. If NGM were to take a keen interest in IGLD’s project (after gaining 100% control of it), they would likely want to develop the more profitable high-grade deposit right away.

NGM could perhaps reach production from underground in three or four years. How so soon? NGM is one of the largest gold producers in the world, and IGLD’s property is within NGM’s existing plan of operations.

To be clear, the immediate focus is on the oxide mineralization amenable to heap leaching. The resource delineated 817,700 gold-equivalent ounces, but that’s before recoveries. There will be slippage, as the range of recoveries for gold and silver is 40%–85%. A lot will depend on the mix of transitional, sulfide and oxide zones.

Management will learn more about that through the PEA process. I estimate that 500,000 heap leach recoverable, gold equivalent ounces is a reasonable estimate for the project as it stands. That would be a very nice outcome: 7–9 years at 56–71,000 ounces/year.

Finding more higher-grade (still shallow, open-pittable) oxide material has the potential to add tens of thousands of ounces, but it won’t be a game-changer unless the high-grade intervals found to date are more widespread than currently understood.

The best intercept was shocking: 9.1 g/t gold over 24.4 meters! While exciting, management does not yet know how extensive this high-grade zone is.

If Golden Independence only had the heap leach project, I think the upside would be attractive, but not exciting. However, one has to access the potential value of the 796,200 ounces of 6.53 g/t gold in the hands of a mid-tier or major.

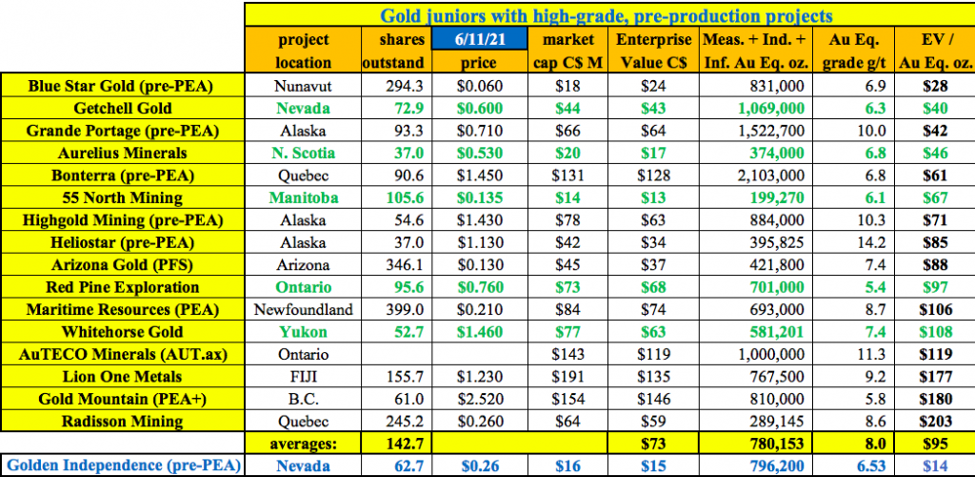

One way to do that is to compare the size and grade to peer North American gold juniors. In the chart below, one can see a number of examples.

The five highlighted names (in green, all pre-PEA) have an average enterprise value (EV; market cap + debt – cash) to ounce of gold in the ground (EV/oz) ratio of ~$72/oz. The average resource size and grade is 585,000 ounces at an average 6.4 g/t, figures that are very close to IGLD’s high-grade, underground resource.

Since IGLD’s resource is 100% Inferred, (peers are a mix of Measured + Indicated + Inferred), I ascribe a $50/oz valuation estimate to IGLD’s 796,200 ounces. That’s a 30% haircut to the $72/oz average mentioned above. At $50/oz, IGLD shares have an implied value of CA$0.65. (Note: this is not a price target, merely a thought experiment). The current share price is CA$0.26.

I believe that if the gold price remains elevated, a rising tide will lift all boats. Consider that a year ago, PEA and feasibility reports were using $1,400-$1,450/oz long-term gold assumptions. In recent weeks I’ve seen three with $1,600/oz and two with $1,650/oz gold price assumptions. A year from now, I suspect the price might be $1,750/oz.

A heap leach operation of say 60,000 ounces/year, for 7–8 years, would be very profitable at today’s spot price! Sixty thousand ounces x US$800/oz operating margin = CA$58M/year in operating cash flow. Add merger and acquisition (M&A) to the picture and valuations of near-term operating mines could soar.

Regarding the deep high-grade scenario (funded by NGM or another mid-tier or major), the sky’s the limit on how that could potentially unfold. I imagine Golden Independence being free carried through a Bank Feasibility Study, while maintaining significant ownership in the project, (say 30%).

Owning 30% of a high-grade underground mine operated by a major would be quite valuable. NGM, in particular, has the experience, deep pockets and mining infrastructure in place to significantly grow and exploit the current 796,200-ounce resource.

While it’s impossible to say if NGM will ever build a mine (or develop a satellite deposit) from Golden Independence’s high-grade resource, if it’s meant to be, I imagine the operation could be 150,000+ ounces/year. NGM’s adjoining Phoenix mine is operating at ~180,000 ounces/year, and is now processing lower grade material than it has in the past.

Therefore, 30% ownership of 150,000 = 45,000 ounces/year attributable to IGLD, with perhaps a US$1,000/oz profit margin—that would be CA$54M in free cash flow per year, for possibly 10+ years, starting in 2024 or 2025, with far less equity dilution, and far less operating risk.

In conclusion, Golden Independence is highly tied to a strong gold price. It benefits very nicely from increases, but below $1,650/oz, robust profitability would start to wane. The company is undervalued in an open pit, heap leach mining scenario, and very undervalued if management can partner with a major to develop its high-grade underground gold ounces.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosures/disclaimers: The content of this article / interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Golden Independence Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Golden Independence Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed / registered financial advisors before making investment decisions.

At the time this article/interview was posted, Peter Epstein owned stock options in Golden Independence Mining, and the company was an advertiser on [ER].

While [ER] believes it is diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, [ER] cannot guarantee that its efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of any article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein’s disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

( Companies Mentioned: IGLD:CSE; GIDMF:OTCQB,

)

Source: The Critical Investor for Streetwise Reports 06/15/2021

The Critical Investor provides details of the explorer’s non-brokered CA$1.2M financing, which will be used to advance projects including the company’s silver prospect at Mount Haldane in the Yukon.

As precious metal prices, alongside almost all other metals, are performing well, Alianza Minerals Ltd. (ANZ:TSX.V) management received lots of interest, and was able to reel in subscriptions for their non-brokered CA$1.2 million ($1.2M) private placement, announced at May 31, 2021. The placement consisted of CA$0.12 flow-through shares, with no warrants attached, which is a sign of strength and rare.

Red Cloud Securities acts as a finder and will be, together with other finders, eligible for a finder’s fee of 7% in cash and 7% in finder’s fee warrants. These warrants are exercisable into shares at CA$0.12 for a period of two years. The proceeds of this round will be used for exploration on the flagship Haldane silver project in Keno Hill, located in the Yukon.

All pictures are company material, unless stated otherwise. All currencies are in U.S. dollars, unless stated otherwise.

After this financing closes, which is planned in the next few days, the treasury of Alianza Minerals will contain CA$2.2M. The company also enjoyed warrant exercises to the tune of CA$625,000 since Sept. 30, 2020, coming from the July 2019 and February 2020 private placements. According to CEO Jason Weber, more exercises can be expected in the coming months. (There are 11.35 million warrants at $0.10 expiring July 2022 and an additional 19.1 million expiring in Feb 2023—we expect those to be exercised soon, as share price moves up and/or they get close to expiry—especially the July 2022 set.) According to Weber, Alianza is now fully funded until Q2/2022.

As there actually were no plans in Q1 to do more financings for the remainder of this year, I wondered what changed Weber’s mind, although the golden rule is when you can get the money, just take it. According to him, there was financing available, and with the challenge in finding drills for projects in the Yukon this year, he felt it was important to expand the current program while they had the rig on site, as it will be very difficult to locate another later this season to bring back to Haldane.

I also wondered if Weber wouldn’t ramp up exploration if they hit something big at Haldane, with more rigs, raising more funds, especially when silver prices keep increasing. He answered that Alianza would definitely want to ramp up with a big program at West Fault should the drilling be successful, but that would be subject to drill rig/crew availability.

Recently, the company announced the commencing of phase 2 drilling at Haldane on May 17, 2021. This has been slightly delayed as it was planned to start in April. According to Weber, this small delay was caused by a late winter in the Yukon. The first results are expected late July.

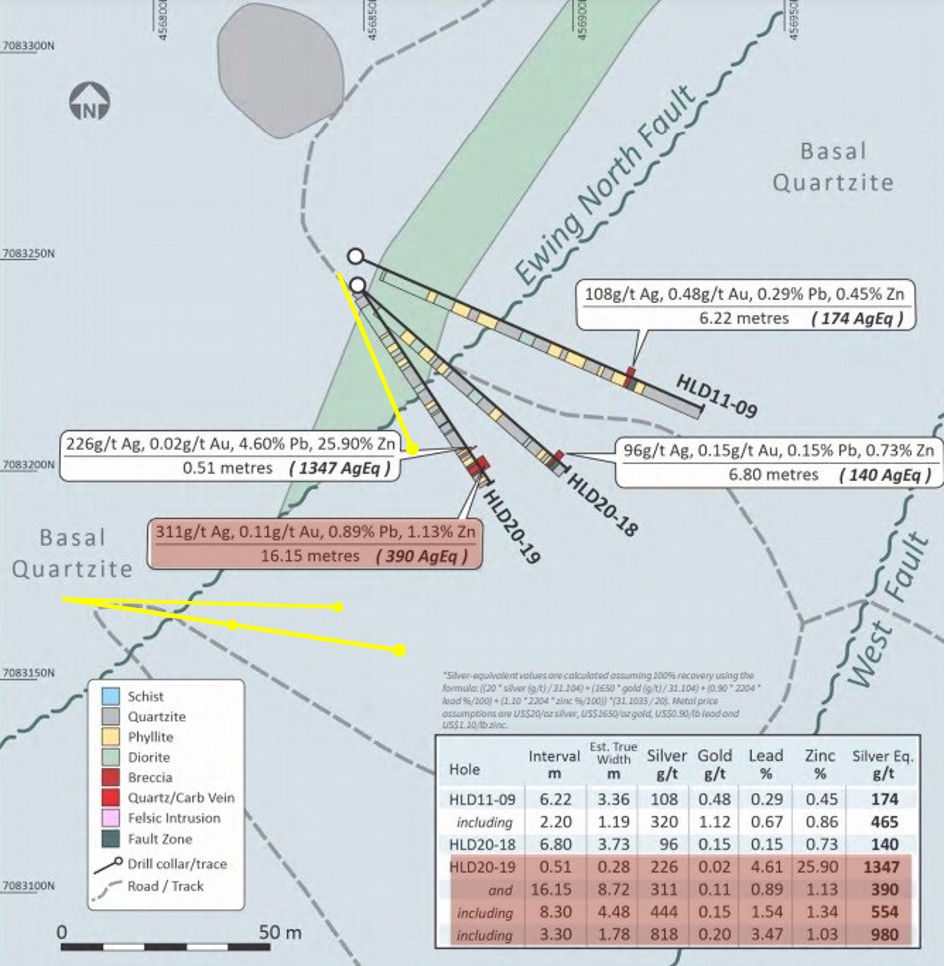

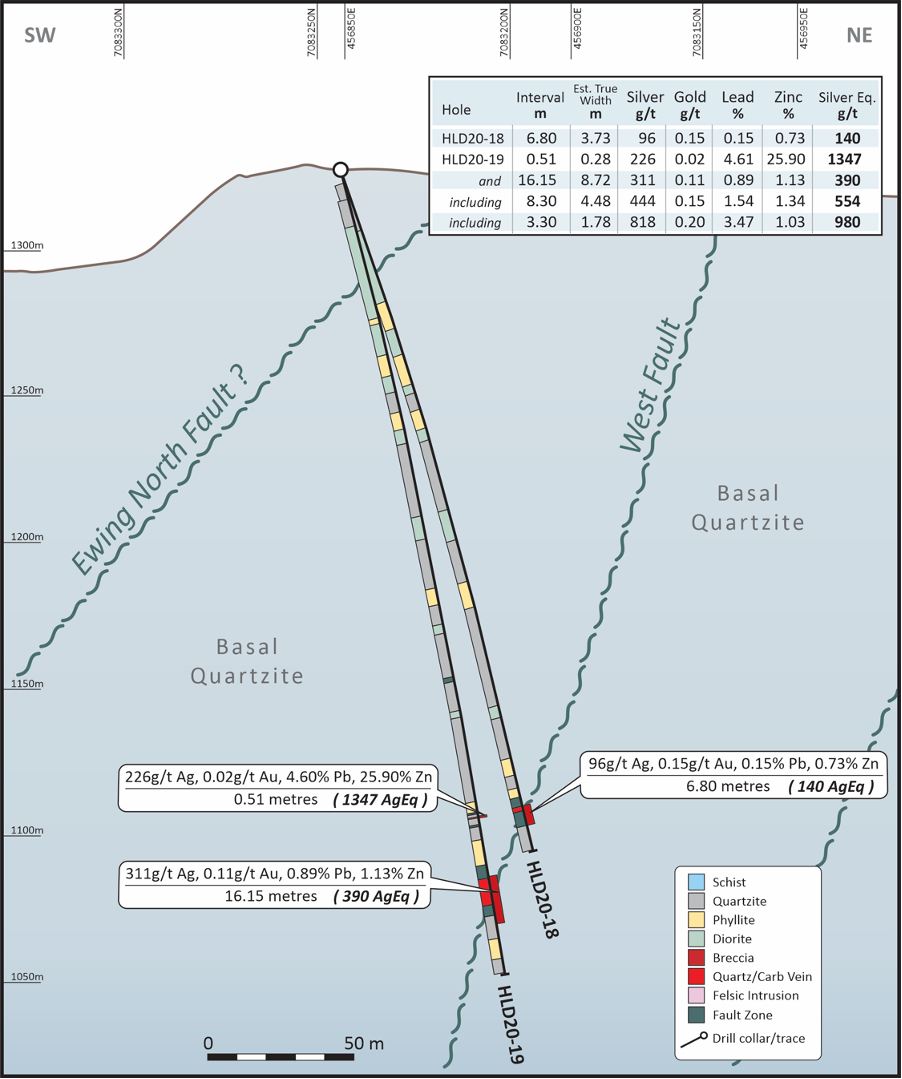

This program will focus on the West Fault target, where highlight drill hole HLD20-19, reported on Jan. 28, 2021, intersected 16.15 meters (16.15m; estimated true width 8.72m) averaging 311 g/t silver, 0.89% lead and 1.13% zinc. This includes a high-grade interval of 818 g/t silver, 3.47% lead and 1.03% zinc (980 g/t silver equivalent [AgEq]) over 3.3m (1.78m estimated true width).

Drilling at the Middlecoff target returned less spectacular results, with hole HLD20-21 having 0.4m at 342g/t Ag from 186m to show for, and HLD20-20 returning no mineralization at all, as it was terminated before the target depth due to excessive hole deviation. According to management, it shows that the structure is continuous to the south, and they will continue to explore to the south and depth for thick, high-grade silver intercepts as witnessed at West Fault drilling.

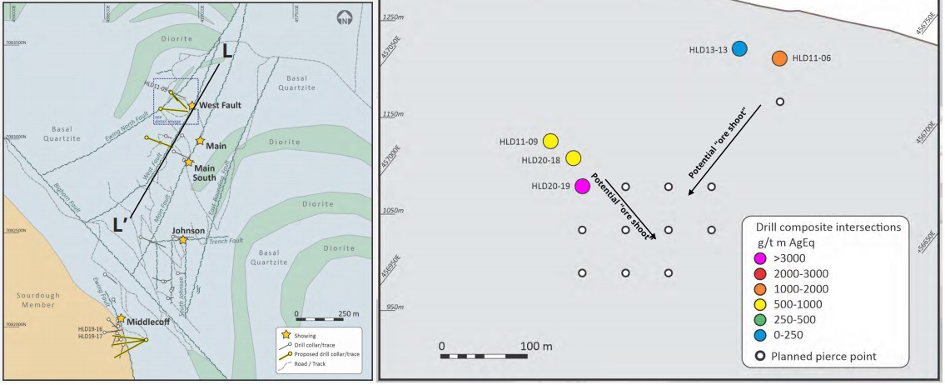

This phase 2 drilling will systematically follow up on this result, testing along strike and down dip to define possible high-grade mineralized shoots associated with HLD20-19. The target remains open in all directions. It is expected that up to four holes will be completed in the current campaign. An overview of phase 2 drilling can be seen here:

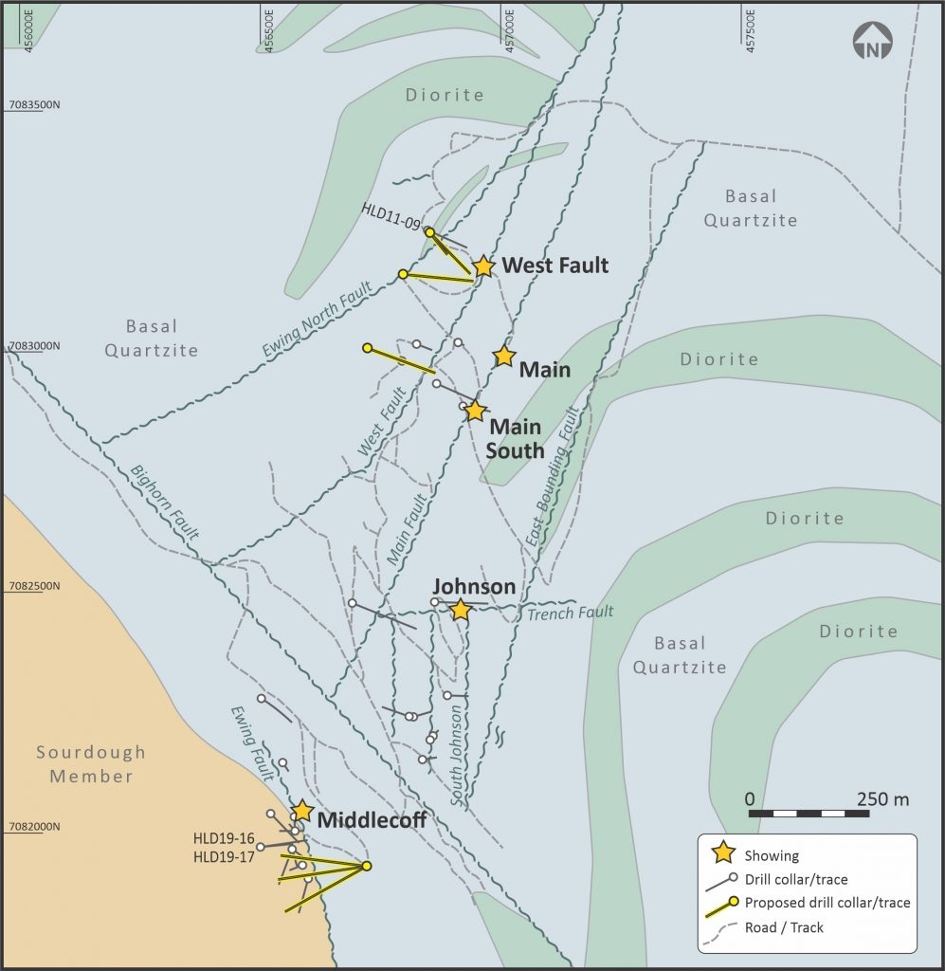

A more zoomed-in map can be seen below:

Looking a bit more in detail on the West Fault drilling:

As can be concluded from the scale in this map, these three holes are just a very small part of the West Fault structure, which currently is interpreted by management to be over 1,750m in strike length. The following section shows the intercepts relative to the two main faults. I asked CEO Weber if he could be so kind to draw the currently planned trajectories on this map in yellow, of the four drill holes that are drilled now, and asked him why these specific trajectories and locations were chosen. He was happy to outline the four collars, and replied that they are systematically stepping out on ~50m centers to identify the orientation of a high-grade “shoot” that may be represented by the intersection in HLD20-19. As they get more information (drill holes), they update the order of planned pierce points.

As a reminder, Weber’s positive attitude is reinforced by the great drill results that Alexco Resource Corp. (AXU:NYSE.MKT; AXR:TSX) is currently producing at its Bermingham Northeast Deep Zone, which is located in the center of the Keno Hill mining district, in between the old mines. Highlights of Alexco program were 8.76m at 3,583 g/t Ag, 5.3m at 2,070 g/t Ag, 8.15m at 1,414 g/t, 6.12m at 1,560 g/t and 7.46m at 1,381 g/t Ag. Alexco is drilling to expand the existing resource of 45 million ounces (45 Moz) 844 g/t Ag at depth, and owns several other high-grade deposits in Keno Hill, only confirming to Weber that Alianza’s Haldane location is close to prolific areas.

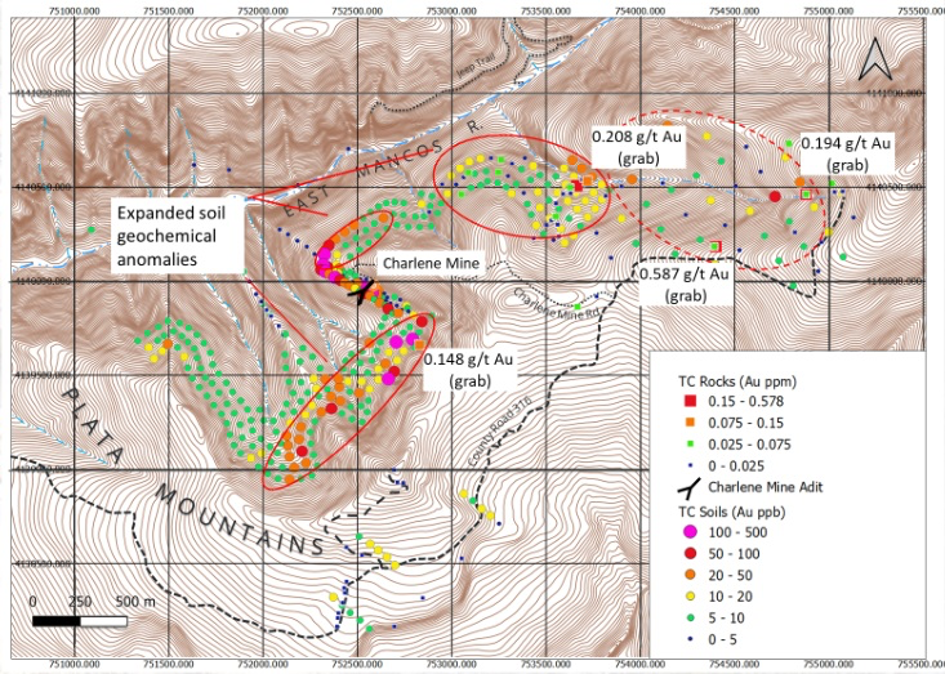

Other active projects of Alianza Minerals are Twin Canyon in Colorado, and Tim Silver in the Yukon. They expect to get a drill permit for Twin Canyon this summer, and are actively looking to find a joint venture (JV) partner who could assist in exploration. The goal is to start drilling in Q3 of this year.

The company completed a soil sampling survey, and an underground structural mapping and sampling program on the Charlene Mine (see center of map below), and successfully detected gold values (up to 6.28 g/t Au), and expanded the gold in soil anomaly footprint.

CEO Weber was enthusiastic about the results so far: “We are excited by the results of our sampling programs at Twin Canyon. We have now demonstrated a large anomalous gold footprint over 3,000 meters in length with multiple prospective altered host stratigraphic horizons. A key component of the program was gaining an understanding of structural controls for gold mineralization, which we have achieved, along with returning numerous multi-gram-per-tonne gold analyses. This knowledge will be utilized in designing and refining drill targets at Twin Canyon and will be integral to finding a partner to advance the project through drilling.”

Regarding the Tim project, Coeur Mining Inc. (CDE:NYSE), the operator of the JV, commenced a reconaissance exploration program last month, which consists of a SkyTEM airborne geophysical survey, and will be followed up by groundwork later this season. The survey is expected to collect magnetic and resistivity data over the concessions to help identify and delineate structural features on the property. It is also expected that this data will be valuable in mapping geology in areas of sparse outcrop. This data will be used to plan subsequent work, including mapping, soil geochemical sampling and trenching later this summer.

According to Weber, the results of the survey are already known to Coeur, but he is not allowed to share them, as is often the case when the JV partner is the operator. I asked him if he had a grasp on what and when he was able to share any exploration results with the general audience, and according to him it will most likely be late 2021 before they have anything they can release publicly.

On a final note, the company also reported on April 28 the acquisition of additional data on the Yanac Copper project in Peru. Yanac is a drill-ready copper porphyry project, and the data contained results from a five-hole reverse circulation (RC) drill program from 2005. One hole returned 232m at 023% Cu and 0.015% Mo.

The company was planning to target follow-up drilling, but the current elections in Peru seem to point toward a very close victory for candidate Pedro Castillo, who is vehemently anti-mining, so management is waiting for the definitive outcome. According to Weber, a victory for Castillo has no consequences for holding the project in the near term, but it would factor in the decision-making process if the climate for mining in Peru were to drastically change for the worse. He added that they are actively talking to potential partners to take the project on, so any uncertainty has not had a large impact yet.

Conclusion

The wait is on for the upcoming drill results on Haldane, which are expected late July, and an additional CA$1.2M in the coffers of the company doesn’t hurt, of course. The goal is resembling the central Keno Hill grades, as drilled by the likes of Alexco, routinely containing four-digit silver grade results over 5-10m. If Alianza could succeed in producing such assays, and the silver price holds up or rises even further, as is widely anticipated among experts, the tiny market cap of CA$15M should be something of the past real soon. As the company is involved in more than one project, the gamble isn’t as binary as with a one-project greenfield explorer.

Mount Haldane drilling

I hope you find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclaimer: The author is not a registered investment advisor, and currently has a long position in this stock. Alianza Minerals is a sponsoring company. All facts are to be checked by the reader. For more information go to www.alianzaminerals.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

( Companies Mentioned: ANZ:TSX.V,

)

The federal government has already run a $2.06 trillion budget deficit in fiscal 2021 with four months left to go. But somewhat surprisingly, over the last few months, the national debt hasn’t increased at nearly the pace you would expect considering the budget shortfalls. Given the level of spending, borrowing should be much higher. How has […]

The post Blog first appeared on SchiffGold.

Inflation is running hot right now. The May CPI data came in hotter than expected, a trend we’ve seen every month this year. But the Federal Reserve and the mainstream financial media continue to insist inflation “transitory.” Peter Schiff recently appeared with Tucker Carlson on Fox News to talk about skyrocketing prices. Peter started by […]

The post Blog first appeared on SchiffGold.

As we enter into the Great Reset, it is likely that the US dollar will collapse as… by Josh Sigurdson with Tim Picciott via World Alternative Media Josh Sigurdson talks […]