Carlin-Type Gold Deposits: Everything You Need to Know – Visual Capitalist

Carlin-Type Gold Deposits: Everything You Need to Know Visual Capitalist

Carlin-Type Gold Deposits: Everything You Need to Know Visual Capitalist

Gold price has peaked for the year – DailyFX.com Kitco NEWS Russia’s central bank says it will stop buying gold at a fixed price Reuters Buy Gold […]

Gold and silver testing resistance | Kitco News Kitco NEWS

Gold, silver up but well down from daily highs; U.S. CPI awaited Kitco NEWS

Goldman Sachs continue to look for upside in gold Kitco NEWS

Kiski Area winter guard team captures gold medal at world championships TribLIVE

As Russia appears to be on the verge of defaulting on its debt, the U.S. debt market is also signaling trouble ahead. Treasury bonds, long […]

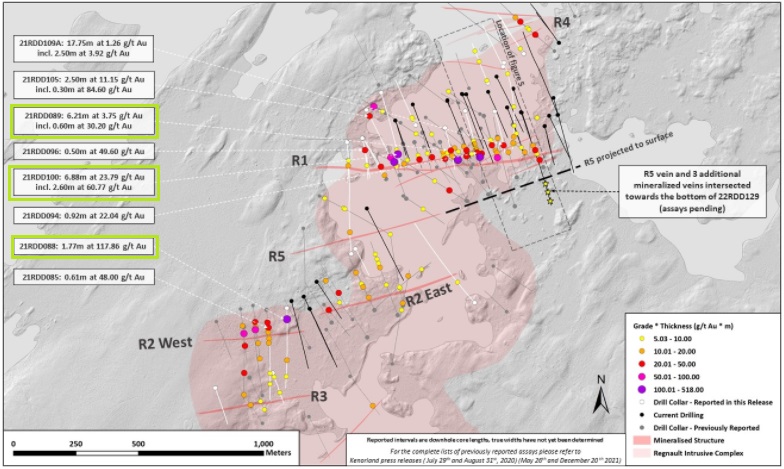

Source: The Critical Investor 04/10/2022 The Critical Investor sits down with Kenorland Minerals CEO Zach Flood to discuss the company’s latest exploration results from its […]

Source: The Critical Investor 04/08/2022 The Critical Investor looks at a junior miner that has been raising cash and acquiring additional claims for its Ontario […]

Gold: Recent Delivery Month Delivery volume for April gold is looking strong, beating out February. There are still 1,984 contracts open, so the month could […]

Copyright © 2026 | WordPress Theme by MH Themes