Gold Trader Hiring Spree Drives Up Pay as Bullion Market Booms Yahoo Finance

Author: Gold News Club

Treasure trove of gold coins, ancient jewelry unearthed in Christian city near Sea of Galilee Fox News

Goldman Sachs revisits gold price target for 2026 TheStreet

Guanajuato Silver Mines: Leading Sustainable Mining In 2026 Farmonaut

The investor gold rush is an outbreak of huge overthinking Financial Times

- Gold Price Rebounds After Sharp Selloff. Why It’s Back in Demand. Barron’s

- Gold’s price is plunging. Here’s why (and what investors should do next). CBS News

- A Gold Crash Everyone Saw Coming Lures Bargain Hunters Worldwide Bloomberg.com

Californians keep finding leftover loot from the Gold Rush — 1 man even bought a home with his spoils. How to cash in Yahoo Finance

Secret mining studies and private deals: is a new gold rush quietly starting in El Salvador? The Guardian

Gold’s relentless rally saw the precious metal surge nearly 10% just a week after breaking the $4,000/oz mark. At the same time, prominent voices in finance and media are breaking from decades of convention to question the stability of US assets.

In this week’s The Gold Spot, Scottsdale Bullion & Coin Founder Eric Sepanek and Precious Metals Advisor John Karow discuss what gold’s sustained strength signals about the US dollar and Treasuries, what the recent pullback suggests about the metal’s next moves, and why even long-time skeptics are beginning to recognize gold’s growing central role in global markets.

Gold’s Post $4,000/oz Moves

About a week ago, gold prices blew through $4,000/oz, putting to rest questions about the precious metal’s momentum. Within a week, spot prices nearly tacked on another 10% gain, stretching to $4,380.89/oz before a minor sell-off. Gold prices remain above the $4,000/oz threshold, signaling a new floor to support its price discovery.

The yellow metal’s boom is exciting for precious metals investors and a further indication of the asset’s inherent value, but this robust price action casts a shadow on US assets more broadly. Generally speaking, gold and USD-linked instruments — such as the dollar and government bonds — move inversely.

This market-wide phenomenon is playing out right now as record-high gold prices reflect structural weakness in US assets.

What Gold’s Strength Means for US Assets

Gold’s rapid ascent may seem overheated, but it’s less a warning sign for the metal itself and more a reflection of investors shifting out of paper gold instruments and into physical gold. The yellow precious metal has already climbed by more than 50% in 2025 — far above the 10% to 15% gains typically seen in a stable economic environment.

Meanwhile, the US Bond Index plunged 10% early in the year and has yet to recover. With the Federal Reserve resuming rate cuts, the resulting lower yields on long-term bonds continue to weigh on demand.

“The minute we start dropping interest rates, that’s going to devalue bonds. Other countries holding Treasuries will start selling those to buy physical assets like gold and silver.”

Eric Sepanek

SBC Founder

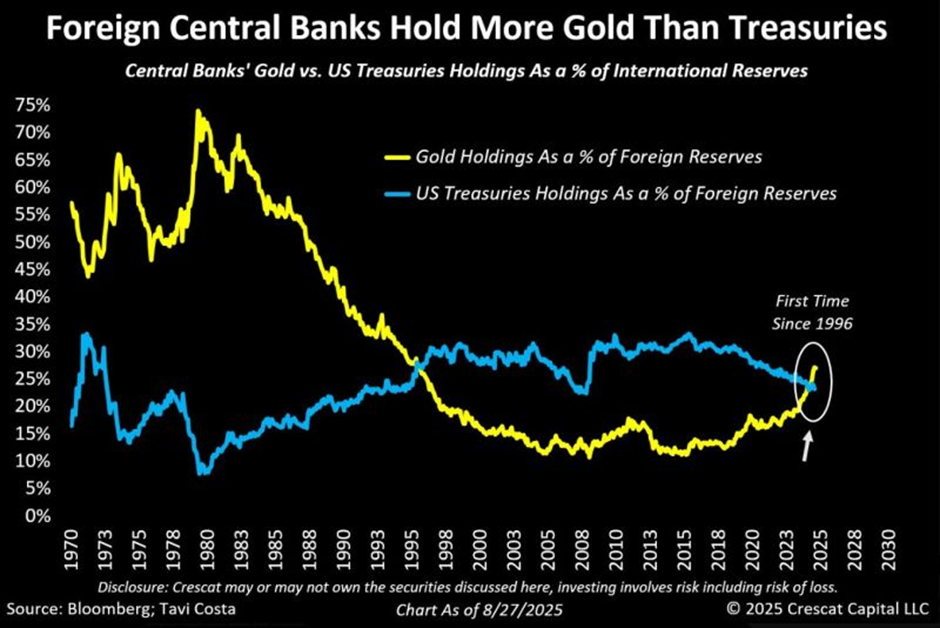

The US dollar also faces a sharp drop in global demand, particularly from official foreign investors. Nations deliberately pursue de-dollarization to reduce exposure to the US economy as national debt mounts, which just hit $38 trillion, and concerns over dollar-based risks grow. For the first time in years, central banks are buying more gold than dollars.

Source: Crescat Capital LLC via Investing.com

Major Media & Financial Names Change Tune

For decades, major media outlets and leading financial institutions have advocated the 60/40 investment strategy, which allocates 60% of funds to stocks and 40% to government bonds. Recently, some of the most recognized — and least expected — leading names have revised that conventional approach, opting for a more gold-heavy alternative.

Currently, many significant names are pushing for a 60/20/20 portfolio strategy, in which investors allocate 60% to stocks, 20% to bonds, and 20% to gold. CNBC, Bank of America, Morgan Stanley, Peter Schiff, and a growing chorus of financial leaders and media moguls are changing their tune on bonds and gold.

This is a tacit acknowledgement that US Treasuries no longer provide the financial stability to justify their inclusion as a bedrock of investment portfolios.

Gold Now Considered Safe-Haven

Gold’s exclusion from the traditional 60/40 strategy reflected widespread skepticism among conventional investment firms. The past few years have shattered this dominant belief system as bond markets dip, the US’s credit rating falters, national debt spikes, and the greenback sputters.

Simultaneously, gold is reclaiming its position as a cornerstone of the global economy. Since the end of the gold standard, countries have nominally attached their fiat currencies to the physical metal through massive gold reserves. Now, the yellow metal is taking a more official central position. Recently, the global banking system recognized gold as a Tier 1 asset, on par with bonds and the dollar.

“Treasury bonds are no longer low risk, and that’s a reflection of the massive debt load the world is carrying.”

John Karow

Precious Metals Advisor

Financial Heavyweights Signal Confidence in $5,000 Gold

Even after briefly pulling back from its almost $4,400/oz peak, many analysts and institutions believe gold’s rally is far from over. Major financial players are still calling for record-breaking highs ahead. Bank of America and Société Générale, and now JP Morgan project gold reaching $5,000/oz by 2026, while HSBC predicts the ongoing “bull wave” could carry prices to that level within that timeframe.

Jim Thorne, Chief Market Strategist at Wellington-Altus, expects gold to reach $5,000/oz, arguing that the metal is in the midst of a historic breakout fueled by weakening confidence in US fiscal management. Rob McEwen, CEO of McEwen Mining, echoes that view, linking rising public and private debt to what he believes is a solid setup for gold to climb to $5,000/oz.

James Luke, Metals Fund Manager at Schroders, calls that same price “frankly conservative,” noting that macroeconomic imbalances and persistent inflation could push gold even higher. The deVere Group forecasts $5,000/oz in the near to medium-term, citing inflation, geopolitical risks, and sustained investor demand.

Wall Street heavyweight Jamie Dimon of J.P. Morgan went even further, saying gold “could easily go to $5,000 or $10,000 in environments like this,” referring to today’s mix of fiscal strain and inflationary pressure. Similarly, BlackRock’s Evy Hambro recently commented that gold could “go a lot higher” as investors increasingly turn to it amid global uncertainty.

It’s evident that a rising number of prominent names believe $5,000/oz gold and higher is on the table.

Buy the Dip in Gold and Silver

Gold’s recent 5% pullback doesn’t seem so extreme when viewed in the broader context. The yellow metal has been on a historic rally, posting gains of more than 50% in less than a year. Zoom out to two years, and the gains are over 100%. No healthy asset can achieve those returns without a breather from time to time.

With leading media and financial figures encouraging investors to invest more in gold and silver, central banks topping up their reserves, and gold and silver price forecasts continuing to rise, the outlook for the precious metals market is bullish. These short-term dips should be viewed as a prime opportunity for investors to dollar cost average into a lower cost basis.

People who buy physical gold are long-term players. This is the classic buy-the-dip pattern. When the iron’s hot — strike.–

Peter Schiff warns of a category-5 financial hurricane that could supercharge the gold and silver rally, so investors shouldn’t wait around until conditions are too bad. UBS analysts recently advised investors to use short-term dips to augment their gold and silver exposure. As the old saying goes: It’s better to buy gold and wait than to wait to buy gold.

👉 Ready to make smarter moves in the precious metals market? Unlock the 22 critical errors to avoid when buying precious metals with our free Precious Metals Investor Guide.

Handpicked Related Articles & Videos

$5,000 Gold?! Why It Might Be Coming Faster Than You Think

Gold Rewrites the Rules: From 60/40 to 60/20/20 Investing

Dollar Cost Averaging: What Is It & How It Maximizes Gold Bullion Returns

Question or Comments?

If you have any questions about today’s topics or want to see us discuss something specific in a future The Gold Spot episode, please add them here.

Comment

Categories

Is the US Becoming a Cashless Society?

As cash’s share of everyday transactions declines, digital payments become the norm, and officials fast-track cryptocurrency adoption, many investors are wondering: Is the US becoming a cashless society?

Although people have pondered a world without cash for decades, no point in history has seen more concrete developments to bring about that reality.

Governments are openly discussing reducing the use of hard money, optimizing cashless payments, and even digitizing legal tender. At the same time, consumers and businesses have turned toward non-cash payments for efficiency and convenience.

The pandemic-era accelerated these trends as lockdowns forced commerce online and governments reenvisioned domestic and international trade payments.

While the road to a cashless society is still being paved, it’s picking up pace. Investors who want to prepare their wealth for this rapidly approaching future properly should get an accurate picture of cash’s role in the future.

The Evolving Consumer Payment Landscape

Every year, the Federal Reserve releases a Diary of Consumer Payment Choice survey, which offers insights into how payment behavior shifts over time. Here’s what the latest findings say about the evolving payment landscape.

Cash Continues Decline as Digital Methods Expand

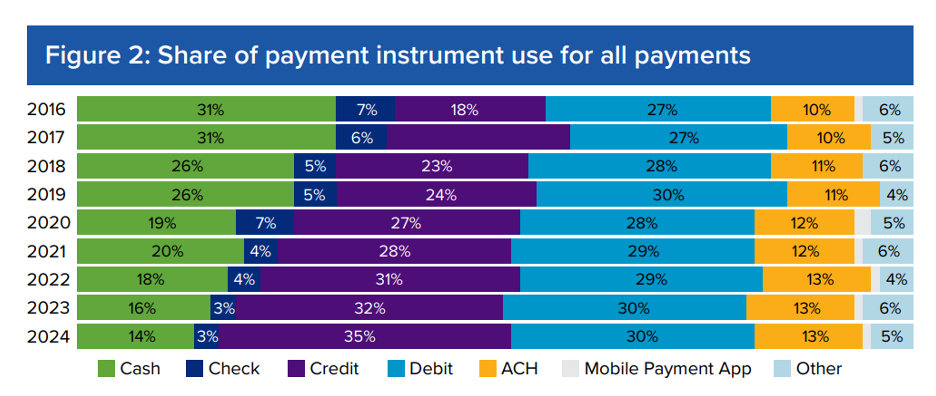

In 2024, cash accounted for only 14% of total payments, nearly halving since 2019. On the flipside, noncash transactions soared from 74% to 86% during the same period. Put another way, non-cash payments grew at an average annual rate of 3%, while the share of cash transactions shrank by more than 11% per year.

If current trends persist, cash could represent just 7% of consumer payments by 2030, with the remaining 93% dominated by cards, digital wallets, and bank-linked transfers, underscoring the country’s steady march toward a cashless economy.

Cash Transactions Hold Steady, But Total Payments Increase

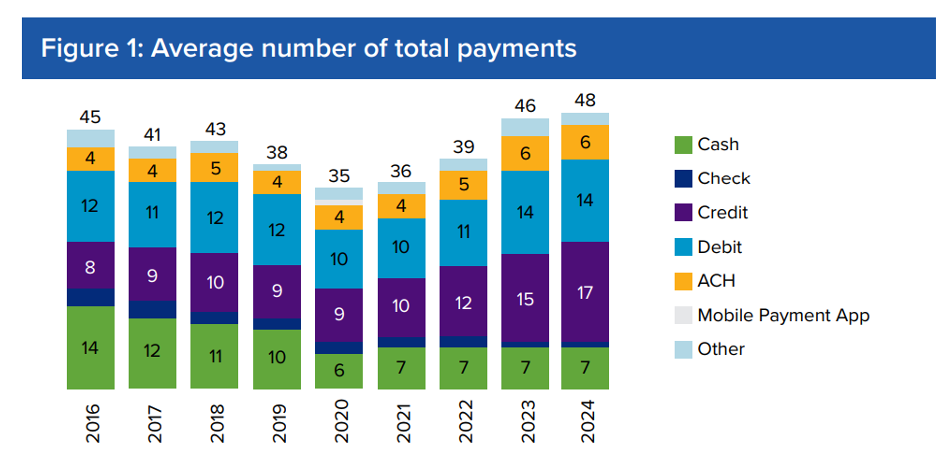

Cash’s share of overall transactions fell to an all-time low of 14% in 2024, but this shift isn’t simply due to Americans using less physical money. Fed data shows that the average number of monthly cash payments has held steady at 7 since 2021.

What’s changing is the rapid growth of digital, card, and bank-based payments, which are expanding the total number of monthly transactions from 35 in 2020 to 48 in 2024.

As a result, even though cash usage hasn’t dropped in absolute terms, its relative share continues to shrink. This shows that cash is being crowded out, not by declining use, but by the accelerating preference for and diversification of alternative payment methods.

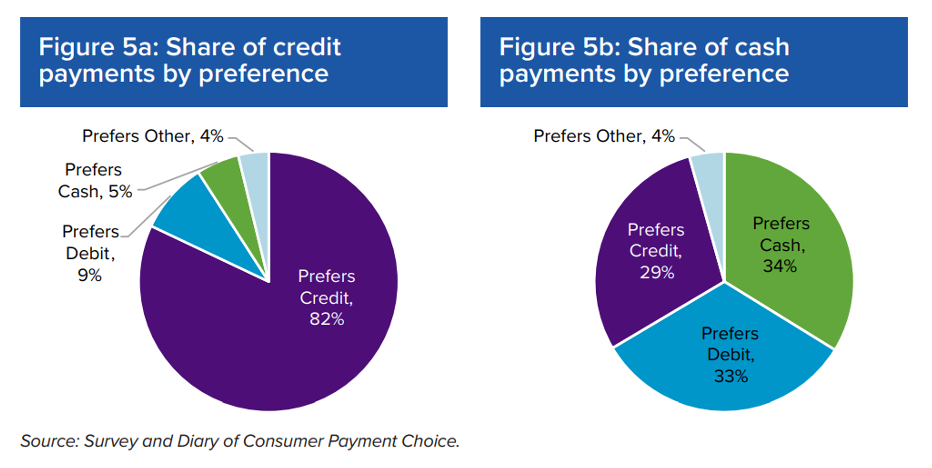

Two-Thirds of Cash Payments Are Not by Choice

If the adage that “cash is king” still holds, it’s an unpopular monarch. The Fed’s findings show that even when cash is used, it’s often out of necessity, not preference. This could occur when digital payments aren’t accepted or simply not functioning.

Two-thirds of all cash payments are made by people who actually prefer to pay with cards. By contrast, over 80% of credit and debit card transactions come from consumers who prefer those specific methods.

As a result, cash is increasingly taking a backseat, used more as a fallback than a first choice, undermining its staying power in a payment system increasingly driven by digital tools and consumer convenience.

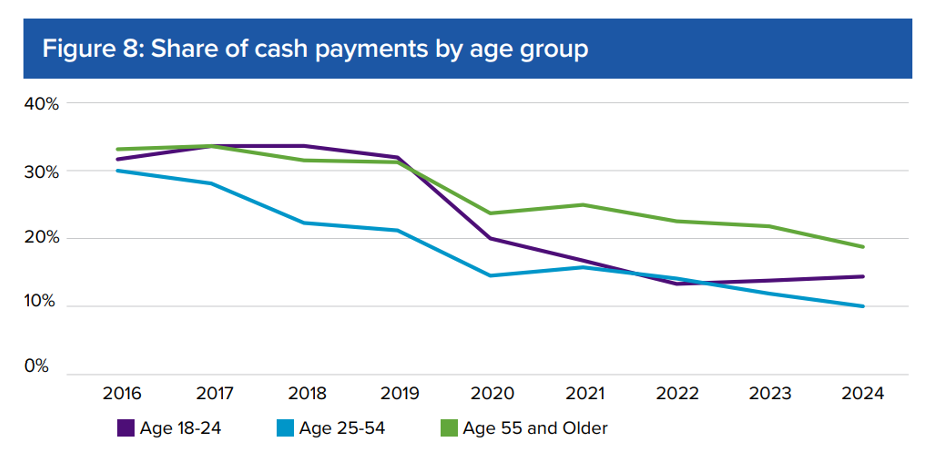

Generational Shift Drives Drop in Cash Transactions

When you break down cash usage by age group, the picture becomes even clearer. Cash is quickly falling out of favor, especially among younger generations. In 2024, just 10% of payments made by adults aged 18 to 24 were in cash, well below the national average of 14%. Adults aged 25 to 54 used cash 5% less than those 55 and older.

Younger consumers use cash less and are also moving away from it faster. In 2016, cash made up about 30% of payments across all groups, with little variation by age. Over the past eight years, a clear generational divide has emerged. Today’s younger, digitally fluent consumers are increasingly bypassing cash altogether. This shift is likely to accelerate as they enter their prime earning and spending years.

Reduction in Circulating Cash

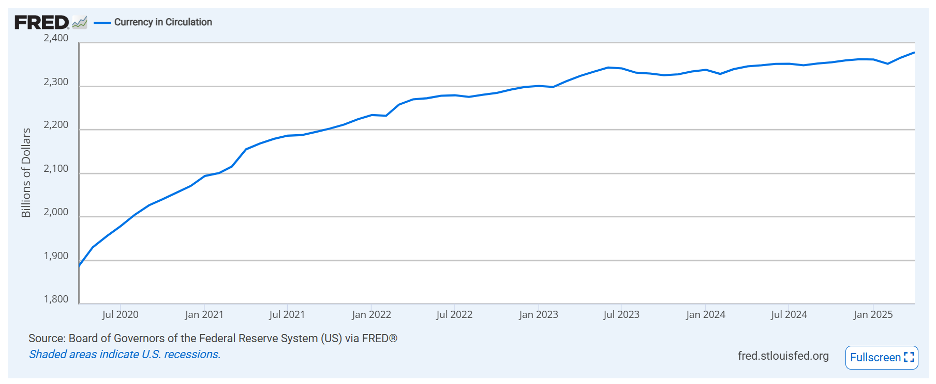

Another crucial metric for determining the country’s changing relationship with cash is tracking how much currency flows within the economy. As of June 2025, the US circulates approximately $2.38 trillion of hard currency. This is a stark jump from $1.76 trillion in 2019.

The primary driver behind the massive surge in circulating cash was the federal government’s attempt to stimulate growth by injecting hundreds of billions of liquid assets into the economy. The amount of physical currency in circulation has plateaued since early 2023, signaling a shift in monetary policy and a downsized demand for cash.

Public Using Cash as a Store of Value

While the near-doubling of cash in circulation over the past few years might imply rising demand for cash-based transactions, a closer look tells a different story. People aren’t spending more cash simply because there’s more of it available.

In fact, as of 2024, 82% of all US currency by value was held in $100 bills, a denomination rarely used for everyday purchases. These high-value notes are increasingly being used as a store of value, not a medium of exchange, suggesting cash is now more about preserving wealth than facilitating payments.

The Business Shift Away from Cash

On the merchant side of the equation, many businesses are adopting cashless payments for a more streamlined transaction process, with some even eliminating hard money as a form of payment altogether.

A Post-Pandemic Pivot

In the wake of pandemic-era closures, the share of cashless businesses doubled. At a similar time, Square–one of the world’s most popular point-of-sale systems–reported cash payments had shrunk to less than one-third of total transactions.

Rebound, Not a Reversal

Cash has since clawed back some of those losses as the economy returned to business-as-usual, yet the arc is still bending toward less reliance on hard money.

Data gathered from the Fed suggests only 60% of companies in the US accept cash, leaving 40% that presumably only take cashless forms. In a nationwide survey of small businesses, 19% of owners claimed to cease accepting cash as payment or intended to phase it out in the future.

There’s a debate around whether this rise in cashless transactions is driven by consumer preferences or merchant restrictions. Regardless, it’s evident that the payment landscape is experiencing a significant drop in cash transactions and a growing proportion of cashless options.

Learn everything you should know about investing in precious metals.

Request the Free Guide

How Politics Pushes Us Toward a Cashless Future

While consumer and business habits shape the visible data, political forces often steer the direction behind the scenes. The positions of influential lawmakers, the agendas of fiscal policymakers, and proposed legislation offer critical clues about the future of the US as a cashless society.

Here are some of the most impactful developments:

US CBDC

The idea of a Central Bank Digital Currency to replace or supplement the US dollar has been a hot topic of debate for many years. Dubbed informally as a “digital dollar,” this potential rollout remains in experimental and non-committal phases.

In 2022, President Biden signed Executive Order 14067, directing the government to look into the possibility of a CBDC. Officials have adamantly repeated that the Fed “would only proceed with… a CBDC with an authorizing law.” In other words, it would need congressional approval to move forward with the development.

FedNow Instant Payments

While its CBDC approach remains experimental, the Fed developed a fully digital payment system with the launch of FedNow. This government-backed payment platform aimed to enable instant transactions between financial institutions and their customers. Through this interbank system, banks and credit unions can transfer funds in near real time.

Although FedNow focuses on the digital transaction of real dollars, it could support a broader shift toward a cashless economy if implemented at scale. While individuals, businesses, and third-party payment providers won’t use FedNow directly, they’ll still benefit from the speed and efficiency it provides.

Crypto Integration

No administration has moved faster to integrate cryptocurrency into the US financial system than Trump 2.0. A skeptic during his first term, the president has since been the biggest champion of crypto, launching his own memecoins, tearing back regulations, and pushing for official adoption.

- The SEC removed a rule requiring banks to treat customer-held crypto as liabilities.

- The OCC and FDIC expanded the scope of legal crypto activities and removed pre-approval hurdles.

- The DOJ disbanded its primary crypto crimes unit.

- A congressional resolution blocked new IRS reporting rules for crypto brokers.

- The federal government is exploring a Strategic Bitcoin Reserve and Digital Asset Stockpile.

Is the US a cashless society?

No, the US is not a cashless society…yet. Developments in the private and public sectors seem to be tipping the economy in a cashless direction. Customers are demonstrating an increasing preference for cashless payment methods, and businesses are more than willing to oblige.

For years, the Fed has been looking into the development and adoption of a US CDBC that could potentially replace the physical dollar. At the same time, the Trump admin is fast-tracking the official integration of crypto into the country’s official reserves and banking system.

While fiat currency still plays a foundational role in the economy, it’s fair to say the US is well on its way to becoming a cashless society.

Questions or Comments?

“*” indicates required fields