Mining people: Asanko, Compass Gold, Ivanhoe, Premier Gold Mines, Unigold MINING.com

As the coronavirus spreads fear, sickness, and death, a specter haunts investors – the specter of deflation.

Despite central bankers’ attempts to push inflation rates higher, equity and commodity markets are collapsing. Inflation expectations as reflected in tanking U.S. Treasury yields, meanwhile, appear headed toward zero – and perhaps even below.

“I think that we have a real danger of deflation in the economy right now,” former Trump economic advisor Stephen Moore told Fox Business’ Maria Bartiromo last weekend.

Clearly, symptoms of deflation and leading indicators of economic contraction are now manifesting in dramatic ways:

But before investors jump on the deflation bandwagon, they should carefully consider the monetary and political forces that could be deployed to reverse a whiff of deflation.

Stephen Moore – who was once floated by President Donald Trump as a nominee to the Federal Reserve Board – is now urging the Fed to reinflate the economy. “I think the Fed should be proactive. I want more dollar liquidity in the economy,” he told Bartiromo.

More rate cuts are coming – markets are currently pricing in a further 75 basis-point reduction in the Fed funds rate – and possibly some unconventional liquidity injections as well.

Meanwhile, President Trump is pitching a payroll tax cut and other fiscal stimulus measures intended to supply consumers with more cash to spend into the economy.

Once the threat of deflation becomes a top concern of central bankers and politicians, it is likely to have already run its course… or have little room left to run. Deflation scares tend to be sudden and severe but ultimately short-lived.

As an investment thesis, deflation lacks a long-term driver.

The reality is that deflation will never persist for very long while our inflationary fiat monetary system remains in place.

Obviously, there are no signs the Fed is going to close up shop anytime soon. Both Democrats and Republicans depend on it to fuel their spending and borrowing priorities. And both parties favor easy-money policies.

The old adage, “Don’t fight the Fed” is worth heeding.

The last deflation scare in 2008 led to Zero Interest Rate Policy, Quantitative Easing, and unprecedented Fed balance sheet expansion. A generational buying opportunity emerged in U.S. stocks. While most on Wall Street expected a bear market rally, few predicted a massive bull market that would last for over a decade.

Initially, all asset classes rose out of their 2008-2009 bottoms. Commodities and precious metals, which had delivered standout gains in the years leading up to the 2008 financial crises, resumed leadership into 2011.

As gold and silver topped out in 2011, the U.S. stock market became the prime beneficiary of monetary expansionism in succeeding years.

Today investors seem convinced that once the Wuhan virus crisis abates, the S&P 500 will bounce back and become the place to be for years more to come.

More likely, the current turmoil in markets – and the central bank response – will effect markets in ways that stock market bulls aren’t expecting.

One surprising development currently taking place is that instead of serving as a traditional safe haven, the U.S. dollar is actually dropping precipitously verses foreign currencies. Consequently, foreign developed and emerging markets are often falling less drastically in dollar terms during big down days than U.S. stocks are.

Meanwhile, the strongest currency in 2020 has been gold – up better than 10% for the year. One of gold’s most under-appreciated functions is that of a deflation hedge. When risk assets are being liquidated, an ensuing flight to quality includes gold and Treasuries.

U.S. government bonds have performed spectacularly in 2020. In fact, bonds have been in a super-cycle bull market for nearly 40 years!

In recent years, many bond skeptics have prematurely called a top. But with rates across the entire yield curve plunging below 1% this week, we are now getting close to the point where it will become mathematically impossible to milk bonds for the kind of returns they have delivered in the past.

There is asymmetric downside risk to bondholders given the possibility that inflation fears reemerge. The real losses on 30-year bonds bought with a yield 0.9% would be staggering if inflation merely averages the Fed’s target rate of 2% over that period.

With the bond bubble having little room left to expand and potentially nearing a prick that will burst it… and with a stock market bubble potentially having just burst, where will investors find the next great bull market?

Perhaps in asset classes that have been depressed for many years. No asset class has been more beaten up for longer than commodities. Narrowing down to the precious metals space, it’s hard to find any market more undervalued than silver.

The white metal is now historically cheap versus gold – selling recently at its largest discount to gold (1/98th the gold price) since 1991. This in part reflects how lopsided the deflation trade has become. Unlike gold, silver is more of a pure play on inflation.

When the powers that be finally succeed in staving off the deflation threat with inflationary injections of fiat currency into markets and pocketbooks, new investment trends will take hold. The coming inflation will lift hard assets in general – and could launch silver explosively higher in particular.

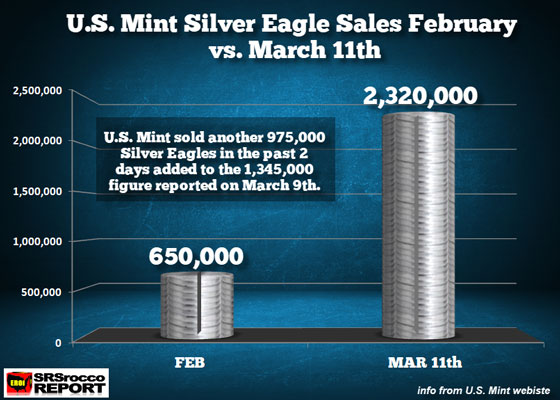

With the spread of the Global Contagion, the demand for physical precious metals has increased significantly. According to the U.S. Mint’s newest update, another million Silver Eagles were sold over the past two days. This brings to total Silver Eagle sales in March at 2.3 million, more than three times the previous month.

On my last update, the U.S. Mint sold a total of 1,345,000 Silver Eagles as of March 9th. Over the next two days, another 975,000 Silver Eagles were sold for a total of 2,320,000.

We haven’t seen this type of buying for quite some time. The U.S. Mint doesn’t sell Silver Eagles directly to the public, but rather to Authorized Purchasers who sell to the public. So, these sales figures represent purchases by the Authorized Dealers. Regardless, if the Authorized Dealers are buying a great deal more Silver Eagles in March, they are doing so because they are experiencing much higher demand from the public.

However, there may be a problem shortly for the Authorized Dealers if the U.S. Mint runs out of stocks of Silver Eagles. Why? Because, the U.S. Mint has cut back on monthly production runs of Silver Eagles due to the decreased demand for the past few years. I doubt the U.S. Mint will be able to supply another 1-2 million Silver Eagles in a short period of time. Thus, we may see the U.S. Mint suspend sales of Silver Eagles shortly until they can increase stocks.

If you do not own any physical precious metals, it may be a good idea to start DIVERSIFYING some assets into Gold and Silver. With the continued spread of the Global Contagion and coming disruptions in the Just-In-Time Inventory Supply Chain, it’s highly likely that demand for precious metals will only increase going forward. With rising demand and constrained supply, we may start to see much higher prices for gold and silver.

Source: Streetwise Reports 03/11/2020

Franco-Nevada’s Q4/19 and full-year 2019 numbers and 2020 guidance are reviewed in a CIBC report.

In a March 9 research note, CIBC analyst Cosmos Chiu reported that Franco-Nevada Corp. (FNV:TSX; FNV:NYSE) significantly beat earnings estimates in Q4/19 due to record sales of gold equivalent ounces and revenues.

Thus, CIBC increased its target price on the gold royalty streaming company to CA$162 per share from CA$157. In comparison, the stock, rated Outperformer by the bank, is trading now at around CA$140.45 per share.

Chiu highlighted that Franco-Nevada’s strong Q4/19 included record sales of 153,396 gold equivalent (Au eq) ounces. This led to full-year 2019 sales of 516,438 ounces. The total was well above the high end of guidance of 465,000–500,000 ounces (465–550 Koz) and CIBC’s forecast of 498 Koz. The high producer was the Cobre Panama mine in Panama, from which Franco Nevada received 43,554 ounces Au eq, also above guidance of 20–40 Koz.

With the strong sales, Franco Nevada posted total 2019 revenue of $844 million, surpassing consensus’ estimate of $814 million, Chiu pointed out. Full-year oil and gas revenue of $115.9 million contributed about 14% to the total revenue. This was driven by oil and gas revenue in Q4/19 of $30 million, which exceeded projections.

Q4/19 adjusted earnings per share (EPS), cash flow per share (CFPS) and EBITDA all exceeded consensus and CIBC’s estimate. Adjusted EPS was $0.59 versus $0.49, CFPS was $0.98 and EBITDA was $202 million.

At the end of 2019, Franco-Nevada had $132 million in cash and $1 billion-plus in available liquidity.

Chiu also noted that Franco-Nevada’s 2020 production guidance of 550–580 ounces of Au eq is solid and reflects a more than a 10% year-over-year (YOY) increase. A primary contributor will be Cobre Panama, in its first full year of operation. CIBC forecasts 555 Koz and consensus estimates 560 Koz. Guidance is expected to be offset by a YOY oil and gas underperformance of about 25%, assuming a West Texas Intermediate oil price of $45 per barrel. 2020 oil and gas revenue is forecast at $80–90 million.

By 2024, Franco Nevada aims to produce 580–610 Koz Au eq versus CIBC’s projection of 570 Koz.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosure:

1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Franco-Nevada, a company mentioned in this article.

Disclosures from CIBC, Franco-Nevada Corp., Earnings Update, March 9, 2020

Analyst Certification:

Each CIBC World Markets Corp./Inc. research analyst named on the front page of this research report, or at the beginning of any subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein accurately reflect such research analyst’s personal views about the company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

Potential Conflicts of Interest:

Equity research analysts employed by CIBC World Markets Corp./Inc. are compensated from revenues generated by various CIBC World Markets Corp./Inc. businesses, including the CIBC World Markets Investment Banking Department. Research analysts do not receive compensation based upon revenues from specific investment banking transactions. CIBC World Markets Corp./Inc. generally prohibits any research analyst and any member of his or her household from executing trades in the securities of a company that such research analyst covers. Additionally, CIBC World Markets Corp./Inc. generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that such analyst covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report, CIBC World Markets Corp./Inc. may have a long position of less than 1% or a short position or deal as principal in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures set forth below, may at times give rise to potential conflicts of interest.

Important Disclosure Footnotes for Franco-Nevada Corporation (FNV.TO)

• 2a These companies are clients for which a CIBC World Markets company has performed investment banking services in the past 12 months: Franco-Nevada Corporation

• 2e CIBC World Markets Inc. has received compensation for investment banking services from these companies in the past 12 months: Franco-Nevada Corporation

• 2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services from these companies in the next 3 months: Franco-Nevada Corporation

• 7 CIBC World Markets Corp., CIBC World Markets Inc., and their affiliates, in the aggregate, beneficially own 1% or more of a class of equity securities issued by these companies: Franco-Nevada Corporation

For important disclosure footnotes for companies mentioned in this report that are covered by CIBC World Markets Inc., click

here: Disclaimers & Disclosures.

( Companies Mentioned: FNV:TSX; FNV:NYSE,

)

Source: John Newell for Streetwise Reports 03/11/2020

Technical analyst John Newell charts the Dow-Gold ratio and speculates on where it could be heading.

The Dow/Gold ratio broke a trend-line in past few weeks that could be signaling that gold could be trending higher against the Dow Jones Industrial Index in the next 18 months to two years.

An example might be a ratio of 10 or the Dow at 20,000 and gold at $2,000 (a new all-time high in U.S. dollars) equals 10.

Conversely, if the Dow went to 30,000 and gold went to $3,000, the ratio would equal 10. This is not a prediction but an observation.

What I found interesting was in the mid-1970s gold corrected from ~$200 to ~$100 and the Dow/Gold ratio went up ~260%, as it did again from the 2012 lows into mid-2019 but over a longer period.

John Newell is a portfolio manager at Fieldhouse Capital Management and president and CEO of Golden Sky Minerals Corp. He has 38 years of experience in the investment industry acting as an officer, director, portfolio manager and investment advisor with some of the largest investment firms in Canada. Newell is a specialist in precious metal equities and related commodities and is a registered portfolio manager in Canada (advising representative).

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosures:

1) John Newell: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures/disclaimer below.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Additional Disclosures and Disclaimer from John Newell, Fieldhouse Capital Management

Legal Notice / Disclaimer:

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

John Newell has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

John Newell makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of John Newell only and are subject to change without notice. John Newell assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, John Newell, assume no liability for any direct or indirect loss or damage or for lost profit, which you may incur because of the use and existence of the information provided within this Report.

It should not be assumed that the methods, techniques, or indicators presented in these pages will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. Examples presented on these pages are for educational purposes only. These set-ups are not solicitations of any order to buy or sell. The authors, the publisher, and all affiliates assume no responsibility for your trading results. There is a high degree of risk in trading.

Hypothetical and historical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical and historical performance results and the actual results subsequently achieved by any trading program. One of the limitations of hypothetical and historical performance results is that they are generally presented with the benefit of hindsight. In addition, hypothetical and historical trading may not present the financial risks and returns for future trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all which can adversely affect actual trading results.

Disclaimer: This Publication is protected by Canadian and International Copyright laws. All rights reserved. No license is granted to the user except for the user’s personal use. No part of this publication or its contents may be copied, downloaded, stored in a retrieval system, further transmitted, or otherwise reproduced, stored, disseminated, transferred, or used, in any form or by any means without prior written permission. This publication is proprietary.

Neither the information, nor any opinion expressed constitutes a solicitation for the purchase of an investment program.

Chart provided by the author.