Barry Dawes of Martin Place Securities shares his thoughts on the current state of the market, focusing on gold.

Gold has peaked for now, and gold Bugs can lick their wounds for a while. The real world is getting on with life.

T Bond yields are heading lower. The U.S. dollar is recovering, and currency rallies are over.

Small-cap resources are looking good.

Tuesday’s note pretty well covered the hysteria in the markets, sensing the peak in gold for now and the bottoming in most things U.S. Bond yields are lower, and the wild surges into the Swiss Franc and Euro peaked precisely at the 50-year uptrend lines, so the goodbye kisses there should see them make new lows.

The intensely bearish sentiment in U.S. stocks has been met with strong short covering that should see new highs coming along soon. Gold has been rising in a parabola for over two years, and that US$530 final vertical move was a sure sign of some sort of peaking. Peaking for now.

My medium-term target of US$3300 has been met and exceeded. The market now has a massive overhead overhang to digest. Consolidation for a few months at least.

Gold stocks globally have not been reflecting these higher prices, so the downside here should not be great, but new highs might take a while. Small gold and resources stocks, however, will now be aided by a rising U.S. equity market and an assurance that US$2000 and possibly US$2500 will prevail.

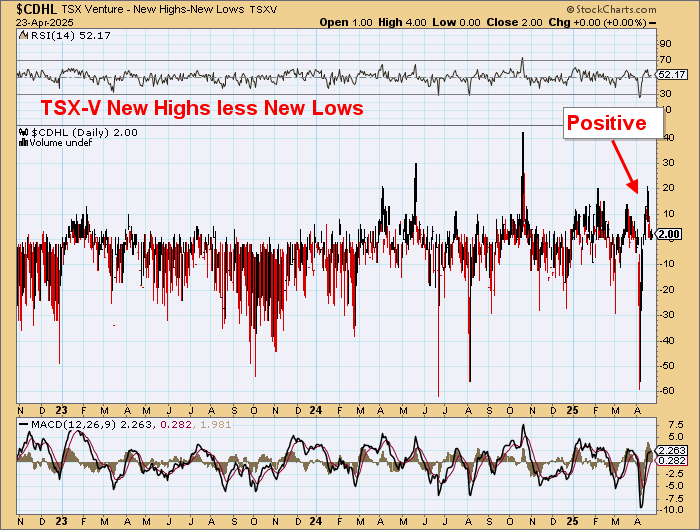

Despite the big sell of in US$ gold today the TSX-V CDNX was UP and new highs less new lows stayed positive.

The real world is turning up — up on the day.

Money flow into the sector:

Gold Stocks

Gold stocks are still in a bull market, but are probably three to five months sideways to down.

XAU is likely to pull back to 160 – ~10%.

This is looking constructive here.

Small Caps

Now, I will focus on small caps.

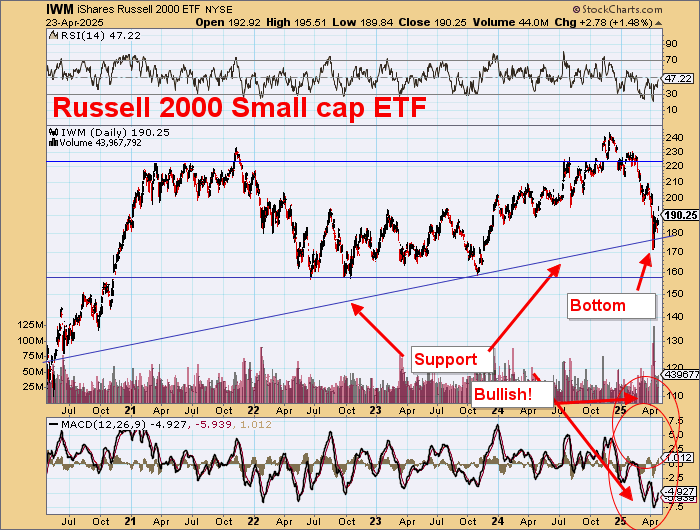

The Russell 2000 Small Cap ETF had a good bound from lows.

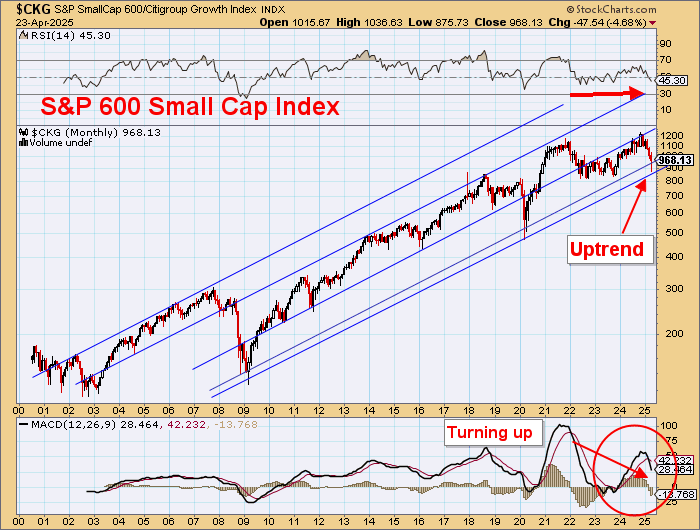

The S&P 600 Small Cap Index’s uptrends is intact.

The S&P Small Cap Advance/Decline Line is wobbly but still constructive.

It is Buy time!

The hysteria, yes hysteria, about the 10-year pushing through 5% just showed shallow thinking.

Be a Gold BULL, not a Gold BUG!

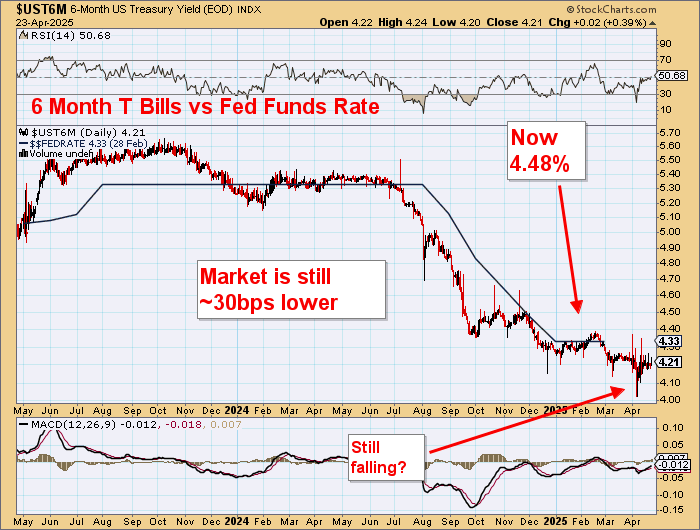

The 1-year Treasury Yield is heading lower.

Island reversal here — sharp falls are coming.

Trump is correct in calling out Fed chief Powell.

Almost 30bps higher than the market, and three to four months behind the curve.

And there is still time for a balanced Federal Budget in FY2025.

And a new gold standard is coming.

It is all good.

Heed the markets, not the commentators.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

This bodes well for Perpetua Resources Corp. (PPTA:TSX.V; PPTA;NASDAQ) having already received the final Record of Decision and potentially getting financed through the Export-Import Bank of the United States. Read on to learn why analysts like this junior miner.

Perpetua Resources Corp.’s (PPTA:TSX; PPTA:NASDAQ) Stibnite gold-antimony project in Idaho is among the first group of U.S. critical minerals projects chosen by the country’s National Energy Dominance Council (NEDC) for fast tracked permitting through the FAST-41 program, a news release noted.

“Though Perpetua received a Final Record of Decision in January 2025, its inclusion on the list demonstrates the [Trump] Administration’s support for the project currently moving through the EXIM (Export-Import Bank of the United States) financing process,” wrote Roth Capital Partners Analyst Mike Niehuser in an April 23 research report. “This is the critical path to a construction decision and integral to our investment thesis.”

Upon being selected for priority attention, Stibnite was put on the Federal Permitting Dashboard, a tool designed to increase transparency, accountability and predictability in the permitting review process and enhance interagency coordination and expedited decision-making, according to a Federal Permitting Improvement Steering Council release.

“Transparency is important for the public to efficiently observe that the law is followed, without commercial or activist influence, resulting in a more efficient process,” noted Niehuser.

“Being recognized as a Transparency Project by the White House underscores the immense strategic value of the Stibnite gold project,” Perpetua President and Chief Executive Officer Jon Cherry said in the release.

These developments are a result of U.S. President Donald Trump’s March 20, 2025 Executive Order, “Immediate Measures to Increase American Mineral Production,” intended to spur an increase in domestic production of critical materials and thereby reduce reliance on other nations for supply. Among the materials Trump noted as critical was antimony, produced historically at Stibnite and the target of future production there.

Crucial Asset to the Country

Perpetua Resources’s Stibnite is “one of the largest and highest-grade open-pit gold mines in the U.S.,” wrote Hotline’s Jay Taylor on March 21. The project has an existing gold resource of 4,800,000 ounces and is projected to produce about 460,000 ounces of gold annually in its first four years of operation, as outlined in the feasibility study and financial update. Plus, the project offers exploration upside.

Along with gold, Stibnite boasts 148,000,000 pounds of antimony, the only known reserve of the metal in the nation, according to the U.S. Geological Survey (USGS) January 2024 Mineral Commodity Summaries.

Stibnite represents a significant opportunity to restore a domestic supply chain of this critical mineral, essential to U.S. national security, the energy industries and advanced technologies, given that China stopped antimony exports to the States last December. Stibnite could supply up to 35% of U.S. antimony demand during its initial six years of production, based on the USGS 2023 Antimony Data Release.

“Perpetua remains a key player in securing a domestic critical mineral supply of antimony through ongoing advancement of the Stibnite gold project,” wrote Heiko Ihle, H.C. Wainwright & Co. analyst in a March 21 research report.

Project costs are in the lowest quartile, with a low strip ratio and a projected all-in sustaining cost of US$435 per ounce (US$435/oz) during years one through four. The antimony will afford byproduct credit with gold as the primary product and economic driver of the project.

Stibnite will be powered by low-cost, clean hydropower, one of the lowest carbon emissions grids in the country. Idaho-based Perpetua will supply part of the antimony produced at Stibnite to Ambri, a U.S. company that is commercializing a low-cost liquid metal battery essential to the green energy transition.

At Stibnite, Perpetua also is restoring the brownfield site. Its plan of operations, approved by the U.S. Fish and Wildlife Department, includes various environmental solutions, such as restoring miles of blocked river habitat and re-establishing fish migration, removing legacy tailings and enhancing water quality.

“Our goal is to transform an area abandoned after 100 years of mining activity into a national strategic asset for critical mineral and gold production through responsible mining and a sustainable approach to restore the environment for the benefit of all stakeholders,” the company noted in its 2025 Investor Presentation.

Along with being chosen as a Transparency Project, Stibnite has received other government interest. This includes a total of about US$75 million (US$75M) from the U.S. Department of Defense and most recently, a letter of interest in 2024 from the U.S. Export-Import Bank for debt financing of up to US$1.8 billion (US$1.8B).

Two Hot Sectors

Gold: Despite gold’s US$100 correction on April 23, the gold bull market has “years to run” due to multiple fundamental reasons, wrote Brien Lundin of The Gold Newsletter on the same day. “So gold bugs and bulls should take the advice of that catchy tune: ‘Don’t worry, be happy!’ This correction in gold was inevitable and desirable. And now we’re back on firmer footing for more gains to come.”

According to Technical Analyst Clive Maund, gold “is in melt-up mode due to an unprecedented confluence of economic and geopolitical factors.” This gold bull market is still in its early stages as evidenced by the still depressed silver:gold ratio. As such, precious metals stocks should take off.

Jesse Colombo of The Bubble Bubble Report shared a similar sentiment on April 17. “If history is any guide, major gold breakouts like this don’t fade quickly,” he wrote. “They tend to kick off bull markets that last a decade or more.”

Growth is forecasted for the global gold market through at least 2030 at a 5.1% compound annual growth rate (CAGR), according to Research and Markets. By then, the market’s size is projected to reach 6,300 tons (6.3 Kt), up from 4.7 Kt in 2024.

However, the market has a current undersupply of about 900 tons, and this is expected to increase to 1,200 tons (1.2 Kt) by Q4/25, wrote John Zadeh on April 17. This growing supply deficit bodes well for higher gold prices.

Niehuser is one of several analysts who are bullish on Perpetua. His rating on the stock is Buy, and his target price reflects 50% return potential.

In the DiscoveryAlert article, Zadeh pointed out that most major financial institutions recently raised their gold price targets for 2025. The forecast now of many is US$4,500/oz by Q1/26 or even sooner.

Technical Analyst AG Thorson also believes gold is in for a substantial long-term rally, possibly even surpassing US$8,000/oz by 2030E, he wrote in an April 18 article on FX Empire. However, he also thinks a pullback below US$3,000/oz is highly likely.

“I believe gold is nearing a major peak and is likely headed for a 20% correction that could unfold over the next three to six months,” Thorson wrote. “That said, if silver surprises to the upside and breaks above US$35/oz in the coming days, the rallies in gold and mining stocks could extend beyond April.”

Jana Kane, editor-in-chief of the LiteFinance trading blog, reported on April 21 that analysts’ gold price forecasts for 2027 to 2030 generally are favorable. Their projections have the price landing somewhere between US$4,988.99 and US$5,194/oz by 2030.

Whereas longer-term forecasts, for 2040 to 2050, are less certain due to numerous factors, most analysts’ gold price estimates remain bullish, between US$8,243 and US$10,000/oz during that period, Kane added.

Lundin highlighted on April 21 that even though gold’s current ascent seems “unstoppable,” most mining stocks have not started recognizing the yellow metals’ bull market. The largest, most profitable gains have yet to be realized.

With the gold price soaring, now is the time to take or add to positions in mining stocks that either have not moved yet or have moved but still have a significant upleg ahead, Maund noted on April 11.

Antimony: Demand for antimony continues to increase because the metal is vital to many industries, a March 7 Carbon Credits article pointed out. Applications include munitions, small arms, missiles, batteries, solar panels, flame retardants, chemicals and alloys, and more.

The global market is projected to expand to US$3.5B in value by 2030 from $2.5B in 2024, reflecting a 6.2% CAGR, according to Research and Markets. The U.S. antimony market also is forecasted to grow significantly, reaching an estimated value of US$107M by 2032.

Despite rising demand, global supply of this critical mineral is in a deficit. According to Barry FitzGerald in an April 12 Stockhead article, antimony stockpiles have been diminished because of ongoing wars, and military stores must be replenished. The solar industry also is helping dwindle the world’s supply as it needs antimony for its top-end glass panels.

H.C. Wainwright’s Ihle rates PPTA Buy. His target price represents a 52% return to target from the company’s current share price.

“In short, antimony has become a metal that everyone wants and needs,” FitzGerald wrote. “It is why the price is at record levels and why the price will not be retreating any time soon.”

Specifically, since China curtailed antimony exports to the U.S. in 2024, antimony prices “have been on an absolute tear as [a] result,” he added. “What was being exchanged for US$12,000 per ton just 16 months ago now commands US$60,000 per ton.”

Bob Moriarty of 321gold wrote on April 22 that since Jan. 1, 2023, the antimony price soared 240% from a base of 100 to 340 today. Since Trump took office, the price rose almost 50%.

“Prices for critical metals are exploding, and others are starting to notice those few stocks in this particular area of interest,” Moriarty wrote.

With projects that contain both gold and antimony (like Perpetua Resources’ Stibnite), FitzGerald pointed out, investing in one for the antimony when prices are record high also is an investment in a gold stock at a time of all-time high prices.

The Catalysts: Permits and Financing

Three major catalysts are on the horizon for Perpetua, according to its Investor Presentation. One is receipt of final permits for Stibnite. In this vein, the junior miner expects a decision on final federal approval, in the form of a U.S. Army Corps of Engineers Clean Water Act 404 permit, in Q2/25. Should Perpetua receive this permit as expected, it will be nine years after Perpetua started the formal permitting process for Stibnite (2016) under the National Environmental Policy Act.

The other catalyst is funding to continue advancing Stibnite. Perpetua currently is preparing a formal application to EXIM for debt financing through its “Make More in America” and “China and Transformational Exports Program” initiatives and is expected to complete and submit it soon, noted Niehuser. The analyst expects EXIM financing terms to be better than those with conventional financing, he wrote.

“Inclusion on the Permitting Council’s initial list indicates federal support to grant the Clean Water Act 404 permit and for approval of EXIM financing,” Niehuser commented.

Once the final permits are received and financing is secured, the next major event for Perpetua and Stibnite is a construction decision. If the company decides to proceed, construction at Stibnite potentially could start this year, noted the analyst.

Stock Remains a Buy

Niehuser is one of several analysts who are bullish on Perpetua. His rating on the stock is Buy, and his target price reflects 50% return potential.

Similarly, H.C. Wainwright’s Ihle rates PPTA Buy. His target price represents a 52% return to target from the company’s current share price. [OWNERSHIP_CHART-10820]

“We expect ongoing news flow related to financing activities for the site,” Ihle wrote. “We anticipate continued interest from institutional investors as the domestic antimony supply remains quite scarce while Stibnite continues to get more and more derisked.”

A third analyst with a Buy rating on Perpetua is Cantor Fitzgerald’s Mike Kozak. His target price reflects a potential uplift of 38%, as noted in his March 21 research report.

Ownership and Share Structure

According to Refinitiv, management and insiders own approximately 0.50% of Perpetua.

Institutions own about 63.52%. Top institutional shareholders include Paulson & Co. with 35.08%, Sun Valley Gold LLC with 4.2%, Sprott Asset Management LP with 4.16%, Kopernik Global Investors LLC with 3.05% and Sprott Asset Management USA Inc. with 3.41%. The rest is in retail.

Perpetua has 70.61 million (70.61M) outstanding shares and 69.97M free float traded shares. Its market cap is CA$937.13M. Its 52-week range is CA$6.80–CA$19.72 per share.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

Perpetua Resources Corp. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000.

Doresa Banning wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

After announcing its inaugural divided last month, MAG Silver Corp. (MAG:TSX; MAG:NYSE American) releases production results from its Juanicipio joint venture (JV) in Mexico for the first quarter of 2025. One analyst noted that silver recoveries there have “stabilized at a world-class level.”

After announcing its inaugural divided last month, MAG Silver Corp. (MAG:TSX; MAG:NYSE American) has released production results from its Juanicipio joint venture (JV) in Mexico for the first quarter of 2025.

The company said Juanicipio, 44% owned by MAG and 56% owned by Fresnillo Plc, “delivered exceptional operational performance, record-breaking silver recovery and robust output across all metals, cementing its status as a world-class silver operation.”

Building upon metallurgical enhancements implemented in 2024, Juanicipio achieved a record-breaking record silver recovery rate of 96% in the quarter, the company said.

“We are very pleased with Juanicipio’s blockbuster start to 2025,” said MAG President and Chief Executive Officer George Paspalas. “Consistently strong grades and record recovery have laid the foundation for a strong 2025. Looking ahead, we remain focused on optimizing production and advancing our key capital investments, including the tailings dam expansion and underground infrastructure development, to sustain and enhance our output. We are well positioned to meet 2025 production guidance and continue delivering strong returns for our shareholders.”

In a research note update on April 23, Scotiabank Analyst Ovais Habib noted that MAG’s silver production was above the firm’s expectations.

“We view the results as positive for MAG shares as overall silver production exceeded our expectations with full-year guidance maintained,” wrote Habib. “We continue to look forward to further ongoing optimizations as the company advances on major capital investments including the tailings dam expansion and underground infrastructure development. Following model updates, MAG shares are rated SO (Sector Outperform) with a US$18.50 PT.”

In a research note update on April 23, Scotiabank Analyst Ovais Habib noted that MAG’s silver production was above the firm’s expectations.

Canaccord Genuity’s Dalton Baretto also issued an updated note on April 23 after MAG’s release.

“While production guidance was above our forecasts, we note that this was again driven by higher grades than anticipated and implies that Q1 could be the high-water mark for production based on average grade guidance for the year,” Baretto noted. “That said, we note that Ag recoveries have stabilized at a world-class level of at or above 95%. The mill average run rate was also the highest level in five quarters. We are surprised by the elevated level of sustaining capex guidance, as these are ~2x the level indicated in the March 2024 technical report.”

Preliminary Production, Guidance for 2025

MAG said Juanicipio saw steady milling performance during Q1, with 337,000 tonnes of ore processed, which is consistent with 2024 levels.

The silver head grade averaged 430 grams per tonne (g/t) during the quarter, achieving the top end of 2025 grade guidance.

Preliminary Q1 production included 4.5 million ounces (Moz) silver (Ag) and 10,198 ounces gold (Au), the company said. Comprehensive financial and operational results are expected to be released on May 12.

For 2025 guidance, silver production at Juanicipio is forecast to range between 14.7 and 16.7 Moz, with payable silver production expected between 13.1 and 14.9 Moz, Fresnillo reported.

That’s based on a throughput rate of 4,000 tonnes per operating day at a silver head grade 1range of 380 g/t to 430 g/t, the company said. The gold (Au) head grade is expected to range between 1.2 g/t to 1.4 g/t.

Continuing optimization efforts and sustaining capital investments mean cost guidance is expected to range between negative US$1 to US$1 and US$6 to US$8 per silver ounce sold, respectively. Sustaining capital expenditures for 2025 are estimated between US$70 million and US$80 million, MAG said.

Some key investments include “expansion of the tailings dam to provide approximately six years of deposition capacity; (and) development of underground workshops, electrical and pumping infrastructure, and ventilation systems to support continued mine development and operations,” the company said in a release.

Expansionary capital expenditures for 2025 are estimated between US$22 million and US$28 million and are related to the installation of an underground conveyor system expected to be commissioned in late 2026 to support expanded mining rates and deliver enhanced efficiencies and mining cost reductions.

Expert: Market ‘Liked’ Dividend Announcement

In March, MAG announced a fixed dividend of US$0.02 per share and an additional cash flow-linked dividend of US$0.16 per share for a total dividend of US$0.18 per share.

“MAG shares were up 5.9% on the news, showing that the market liked it,” Peter Krauth wrote for The Gold Advisor on March 26. “The company has serious ongoing discovery potential at Juanicipio, Deer Trail, and Larder. Shares are up 24% just since the start of this year. Attractive to add on weakness.”

An April 23 Research Flash by National Bank of Canada’s Don DeMarco noted that Juanicipio is “starting to show consistent, elevated production reflective of a world-class mine.”

An April 23 Research Flash by National Bank of Canada’s Don DeMarco noted that Juanicipio is “starting to show consistent, elevated production reflective of a world-class mine.”

DeMarco maintained his Outperform rating and CA$32.75 per share price target for the stock.

“Our thesis considers production growth at Juanicipio (44%), diversified metal production, a re-rate to producer multiples, exploration upside and M&A appeal tempered by Juanicipio JV terms, which limit profit sharing to once per year,” the analyst wrote.

Roth Capital Partners LLC Analyst Joe Reagor said MAG’s inaugural dividend is a boost for shareholders.

“We believe this dividend policy could broaden MAG’s investor base and thus, we view it as a positive,” Reagor wrote.

“[The] inaugural dividend with cash flow-linked feature allows investors [to] get paid with a yield that’s among the top for silver names while maintaining upside to silver prices,” wrote DeMarco, who maintained an Outperform rating on the stock with a CA$30.50 per share target price.

The Catalyst: Silver Mirrors Strength of Safe-Haven Gold

According to a report Wednesday by FX Empire’s Arslan Ali, silver has recently mirrored the strength of safe-haven gold, hovering around US$32.70 and hitting an intraday high of US$32.86.

“A falling U.S. Dollar Index, now near a three-year low, has made dollar-denominated metals more appealing to global investors,” Ali said. “Despite a more positive global equity tone, silver continues to find support from both safe-haven flows and solid industrial demand.”

The material’s industrial utility that helps create a deficit for silver, which is the best conductor of electricity among the metals. [OWNERSHIP_CHART-536]

“Underpinning silver’s fundamentals is robust demand from industrial applications,” The Silver Institute said in its World Silver Survey 2024 report. “These continued to push higher last year, reaching a new all-time record, fueled by the remarkable rise in solar demand and in spite of stagnation in some other sectors. Sluggish silver supply, owing to the slight decline in global mine production, was another factor contributing to silver’s deficit conditions last year.”

Mordor Intelligence noted that silver is expected to register a compound annual growth rate (CAGR) of more than 5% between 2024 and 2029.

Ownership and Share Structure

Institutions own 70% of MAG, and 30% is retail, according to the company.

Top institutional shareholders include Juanicipio operator Fresnillo Plc. with 9%, BlackRock Investment Management (UK) Ltd. with 10.8%, Van Eck Associates Corp. with 9%, First Eagle Investment Management LLC with 6.2%, and Sprott Asset Management LP with 3%, the company said.

MAG Silver has a market cap of US$1.56 billion. It has 103.36 million shares outstanding, according to Reuters. It trades in a 52-week range of CA$11.29 and CA$18.27.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

MAG Silver Corp. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000.

Steve Sobek wrote this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

Paradigm Capital recently initiated coverage on Goldshore Resources Inc. (GSHR:TSX.V; GSHRF:OTCQB; 8X00:FWB) with a Buy rating. Read on to see what the analyst likes about this gold company.

On April 22, 2025, Paradigm Capital analyst Don MacLean initiated coverage of Goldshore Resources Inc. (GSHR:TSX.V; GSHRF:OTCQB; 8X00:FWB) with a Speculative Buy rating and a CA$1.20 price target, highlighting the company’s Moss gold project in Ontario as a top contender among the next generation of large Canadian gold mines amid a scarcity of quality, large deposits in safe jurisdictions.

Goldshore’s 100%-owned Moss project is located approximately 100 kilometers west of Thunder Bay, Ontario, with excellent infrastructure including proximity to the Trans-Canada Highway and access to low-cost power. The project hosts a significant resource of 6.7 million ounces of gold, with the pit-constrained portion containing 5.8 million ounces at 1.07 g/t (22% indicated, 78% inferred). The analyst’s interpretation suggests a mineable resource of 4.6 million ounces at 0.88 g/t.

MacLean envisions the Moss project as a large, long-life (15+ years) open-pit mine capable of producing 340,000 ounces of gold per year in the first five years and 279,000 ounces per year over the life of mine, with second-quartile all-in sustaining costs (AISC). At a gold price of US$3,000/oz, the project demonstrates an attractive 32% internal rate of return (IRR) and remains economically viable down to US$2,370/oz (above the analyst’s 20% IRR threshold).

From a valuation perspective, Goldshore is trading at just 0.05x the analyst’s net asset value (NAV) of CA$6.59 per share (at US$3,000/oz gold), which is half the developer peer group median of 0.10x. The NAV is sensitive to gold prices, increasing by CA$0.51 per share for every US$100/oz increase in gold price. At the share price of the time of the report of CA$0.345, Goldshore’s market capitalization is CA$122 million, representing just CA$21 per resource ounce compared to the peer group median of CA$40 per ounce.

The Moss project offers excellent exploration upside, with the current resource covering just 10% of the project’s 35 kilometers of shear structures. The analyst notes that large deposits like Moss often produce for much longer than initially estimated, adding to the project’s strategic appeal for potential acquirers and government stakeholders.

Key risks include uncertainty around the vertical continuity of the mineralized structures given the current 30-70 meter drill spacing for indicated resources and up to 100 meters for inferred resources. Additionally, the timing of major catalysts represents another risk, as the targeted H1 2025 preliminary economic assessment (PEA) may be deferred to Q3-Q4 to incorporate additional exploration results.

With the share price of CA$0.345, the CA$1.20 target price represents a potential return of 248%, making Goldshore an attractive opportunity for investors seeking quality exposure to gold price appreciation.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

Goldshore Resources Inc. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Goldshore Resources Inc.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Disclosure for Paradigm Capital, Goldshore Resources Inc., April 22, 2025

Goldshore Resources Inc. GSHR-CA 2,3 Note: Please refer to above table for applicable disclosure numbers. 1. The analyst has an ownership position in the subject company. 2. Paradigm Capital Inc. has assumed an underwriting liability for, and/or provided financial advice for consideration to the subject companies during the past 12 months. 3. Paradigm Capital Inc. expects to receive or intends to seek compensation for investment banking services from the subject companies in the next 3 months. 4. Paradigm Capital Inc. has greater than a 1% ownership position in the subject company. 5. The analyst has a family relationship with an Officer/Director of subject company. 6. A partner, director, officer, employee or agent of Paradigm Capital Inc. is an officer or director of the issuer. Paradigm’s disclosure policies and research distribution procedures can be found on our website at www.paradigmcap.com. Paradigm Capital Inc. research is available on Bloomberg, CapitalIQ, FactSet and LSEG or at www.paradigmcap.com. Issued by Paradigm Capital Inc. Research Rating System Paradigm Capital Inc. uses the following rating recommendation guidelines in its research:

About Paradigm Capital Inc. Paradigm Capital Inc. (PCI) is a research-driven, independent, institutional equity investment dealer focused on sectors and companies that have attractive longterm secular growth prospects. PCI’s research is available on our website at www.paradigmcap.com. Please speak to your Sales or Trading Representative if you require access to the website. The analyst (and associate) certify that the views expressed in this report accurately reflect their personal views about the subject securities or issuers. No part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendations expressed in this research report. Analysts are compensated through a combined base salary and bonus payout system. The bonus payout is determined by revenues generated directly or indirectly from various departments including Investment Banking, based on a system that includes the following criteria: reports generated, timeliness, performance of recommendations, knowledge of industry, quality of research and investment guidance and client feedback. Analysts are not directly compensated for specific Investment Banking transactions. The opinions, estimates and projections contained herein are those of PCI as of the date hereof and are subject to change without notice. PCI makes every effort to ensure that the contents herein have been compiled or derived from sources believed reliable and contain information and opinions, which are accurate and complete. However, PCI makes no representation or warranty, express or implied, in respect thereof, and takes no responsibility for any errors and omissions that may be contained herein and accepts no liability whatsoever for any loss arising from any use of or reliance on this research report or its contents. Information may be available to PCI, which is not reflected herein. This research report is not to be construed as an offer to sell or solicitation for or an offer to buy any securities. PCI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. PCI may act as financial advisor and/or underwriter for certain of the corporations mentioned herein and may receive remuneration for same. PCI is a member of The Toronto Stock Exchange, The TSX Venture Exchange and The Canadian Investment Regulatory Organization (CIRO). Any products or services mentioned on this website are made available only in accordance with local law (including applicable securities laws) and only where they may be lawfully offered for sale. PCI will not open accounts except in jurisdictions in which it is registered. To U.S. Residents: This report was prepared by PCI which is not subject to U.S. rules with regard to the preparation of research reports and the independence of analysts. PCI U.S. , affiliate of PCI, accepts responsibility for the contents herein, subject to the terms as set out above. Any U.S. person wishing to effect transactions in any security discussed herein should do so through PCI U.S.

Newsletter writer Stewart Thomson addresses the questions: Where does the gold price sale end, and what does the potential upside look like for investors?

The U.S. government is desperately trying to talk the outrageously overvalued stock market up again. The macabre hope of the government, sadly, appears to be to restore investor confidence in chasing the market into a state of even greater overvaluation than already exists now.

Here’s a look at the horrifying level of overvaluation, basis the CAPE/Shiller index (inflation-adjusted PE ratio):

From 1880 to 1980, the U.S. stock market was rarely overvalued, basis a CAPE ratio of 20 or more.

Now?

Now it’s almost always overvalued and rarely undervalued. The problem of course is . . . debt.

Gold has taken a hit this week, as the government tries to restart the “risk-on” theme.

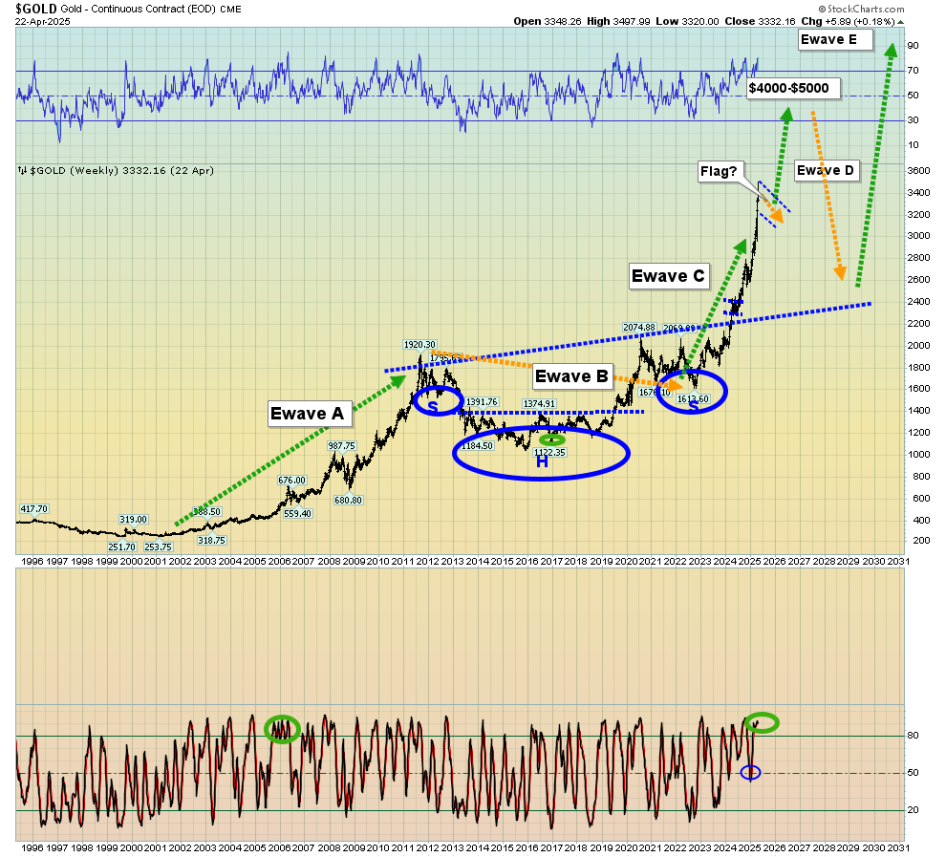

Here’s a look at gold on the weekly chart:

Note the Stochastics oscillator at the bottom of the chart. The pullback for gold was technically due and of course investors are eager to find out what might be next.

The key retracement zones are $3250 (a good buy zone for gold stock gamblers), $3150, and $2950. Those latter two zones are good zones for conservative investors to buy.

They are support and also loosely correlate to key Fibonacci retracement numbers . . . retracements of the entire rally that began with the year 2022 break out from the huge C&H pattern at about $2000.

Here’s a look at another weekly chart for gold, from an Elliott “Big Wave” perspective:

Wave C (3) is likely to end with a massive price surge out of a bull flag that appears to be forming now… and into the $4000-$5000 zone!

Interestingly, from an Elliott perspective, the correction for gold stocks may be over sooner, and no correction is forecast for silver!

Here’s a look at the daily silver chart of the SIVR ETF:

The gold/silver ratio touched round number 100, and silver is surging today . . . with gold down $100/oz!

Silver is a great way for the “little metals guy and gal” to play my 40year inflation cycle theme. I’ll talk more about that cycle in coming updates.

One gold stock that received massive junior mining stock analyst coverage in years gone by . . . and by me now . . . is Novo Resources.

Here’s a look at the daily chart:

I’ve been suggesting the stock can be accumulated in the sub 15 cent zone.

Novo was so widely followed in the past that even a small rally should generate enough momentum to push it to $1.00, even if all that the management hoped would happen . . . never does.

I’ll be covering more key junior miners in more frequent updates in the weeks ahead. The bottom line is that “good” (for the miners) stagflationary times are here, and even better ones are near!

Special Offer for Streetwise Readers: Please send me an Email to freereports@galacticupdates.com and I’ll send you my free “Silver Stocks: Set To Get Hot?” report. Silver stocks tend to rally dramatically in the final stage of a gold market surge. I highlight the SILJ junior silver stocks ETF, and key component stocks that appear set to surge!

I write my junior resource stocks newsletter about twice a week, and at just $199/12mths it’s an investor favourite. I’m doing a special pricing this week of $169 for 14mths. Click this link or send me an email if you want the offer and I’ll get you onboard. Thank-you.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

Stewart Thomson: I, or members of my immediate household or family, own securities of: GDX and SIVR-nyse (ETF). I determined which companies would be included in this article based on my research and understanding of the sector.

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Stewart Thomson Disclosures

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Rick Mills of Ahead of the Herd once again interviews Bob Moriarty of 321Gold to review how current events may impact the markets and discuss two companies.

Below is an interview by Rick Mills, the editor and publisher of Ahead of the Herd, with Bob Moriarty of 321Gold.

Rick Mills (RM): What are your sentiment-tracking measurements telling you currently?

Bob Moriarty (BM): Let me share something intriguing, you’ve known me for quite a while. I consider myself a contrarian and in my publications I explicitly claim that investment knowledge is secondary if you can accurately gauge market sentiment.

The current situation is noteworthy due to this week’s developments and I’ll provide a hint. Gold increased three consecutive days, $100/oz, how much impact do you imagine that had on the DSI [Daily Sentiment Indicator]?

RM: I suspect it’s quite significant.

BM: Surprisingly, it’s minimal overall. One week ago gold’s DSI registered 86 and following three days where gold jumped $100, it went 86, 79, 82, 87 which represents its peak, and with yesterday’s minor decline it’s fallen to 80. I can definitively state it hasn’t peaked at 87 — when it reaches 95 or 96 that will signal a substantial peak but we’re nowhere near that level.

There’s considerable mystery surrounding sentiment measurement, it’s not some random figure he generates, he’s performing mathematical computations on commodities but it’s remarkably precise and for the DSI to decline to 80 with gold at $3,300 that’s simply astounding to me.

RM: It appears counterintuitive, doesn’t it?

BM: Here’s the crucial point, it shouldn’t appear logical. It represents exactly what it is, simply a measurement of sentiment and nothing additional and all these industry personalities claim oh, when the Dow Jones rises gold prices fall, if gold prices increase the S&P decreases, and they’re attempting to link elements that aren’t necessarily always connected.

Sentiment remains sentiment. When we experience an all-time high it will be evident and I believe if you examine April 25th of 2011 I think silver sentiment exceeded its January 1980 levels.

RM: You’re essentially dealing with psychological factors — fear and greed, that’s what sentiment represents and if you can somehow quantify that accurately and express it numerically that’s Bernstein’s methodology.

BM: He’s discovered something valuable, I’ve recognized sentiment’s importance for decades, but finding the most reliable sentiment gauge was extremely challenging.

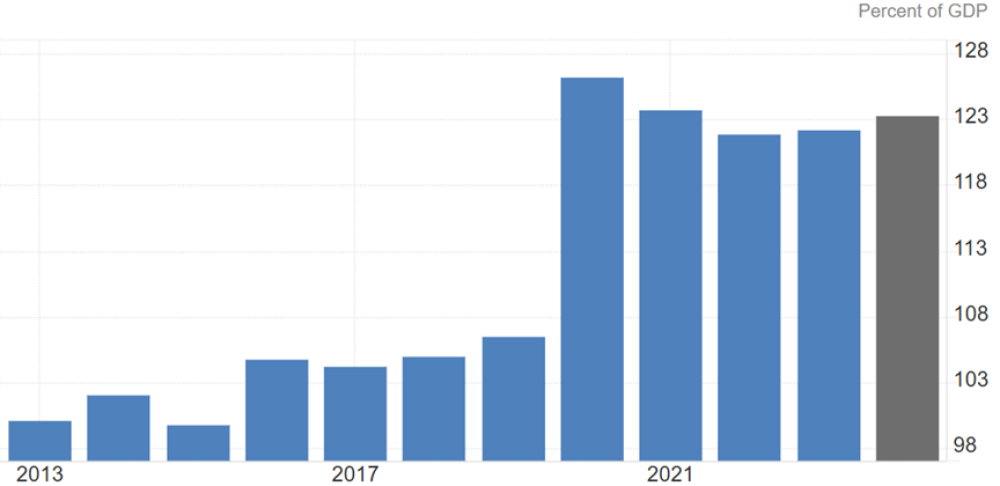

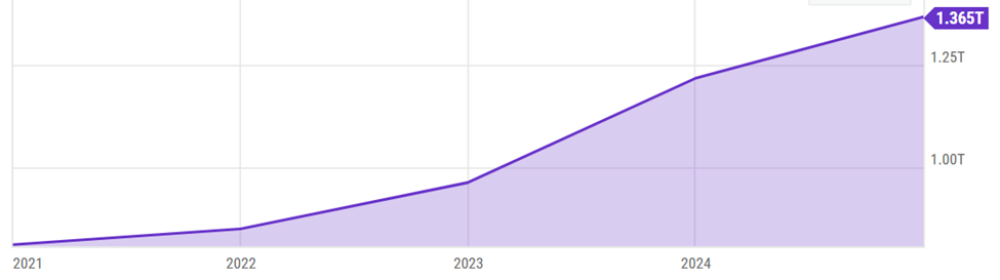

RM: America carries $9.2 trillion of obligations that must be either satisfied, refinanced or newly secured and a substantial portion includes $2 trillion deficit due this year. We’re aware Treasury auctions have proceeded successfully, so currently no discussion about debt monetization, actually there was an enormous Treasury auction in February and literally everyone participated, including the eurozone, Britain, Taiwan and even BRICS nations like China, India and Brazil.

United States — Federal Debt: Total Public DebtUnited States Gross Federal Debt to GDP

We witnessed the largest increase in foreign purchasing since ’21 and they predominantly acquired long-term securities, short-term instruments simply weren’t compelling, and they purchased long-term debt yielding approximately 4.28%.

We understand the Trump administration strongly desires lower interest rates because currently they’re attempting to solidify their agenda, working to maintain tax reductions and everything else, and I believe when people recognize one crucial fact, which will truly resonate with many individuals, is that American military expenditure reaches $1 trillion.

Actually it substantially exceeds that figure because nuclear weapons aren’t included, those fall under Energy, neither are Special Forces nor Veterans’ Administration — the VA, so your primary expense category on federal government financial statements currently is military spending.

That’s changed now, with this major refinancing and debt purchasing at such elevated yields, and the reason they’re acquiring long-term American debt — the 10, 20, 30-year instruments, is because only one alternative offers higher returns, specifically Britain. All other nations’ bonds yield approximately half, their 10-year securities around 1.6% perhaps 2.1%, they’re securing excellent returns on extended American debt, but consequently they’re pushing interest payment expenses beyond a trillion dollars.

U.S. Government Interest Payments

Now your predominant line item in annual government accounting will become interest payments on outstanding debt. That suggests to me something completely unmanageable, what’s your perspective?

BM: Curiously, you employed the most accurate description possible. When Elon Musk described Social Security as a Ponzi scheme he possessed sufficient wealth and prominence to state something universally acknowledged, correct? Social Security operates as a Ponzi scheme and we understand how Ponzi schemes conclude, and I’ve maintained for years, this represents a struggle between the BRICS resource-based system against the Western debt-based framework.

We’ve transformed from a manufacturing nation into a country where 32% of economic activity involves shuffling documents. It constitutes a crisis but one solvable only through collapse and complete restart. My concern is Donald Trump has entered a fragile environment swinging a baseball bat vigorously. He seeks to antagonize our largest trading partner, I simply cannot envision how that succeeds.

I believe it’s not exclusively Donald Trump and tariffs themselves, the collapsed basis trade carries far greater significance than tariffs, believe it or not. A crisis currently unfolds a liquidity emergency occurs behind the scenes within the global financial structure it’s about to explode dramatically, no resolution exists except default and it worries me because I observe Trump selecting the warfare path, thinking it provides escape from Depression I believe substantial probability exists we’ll initiate conflict very shortly.

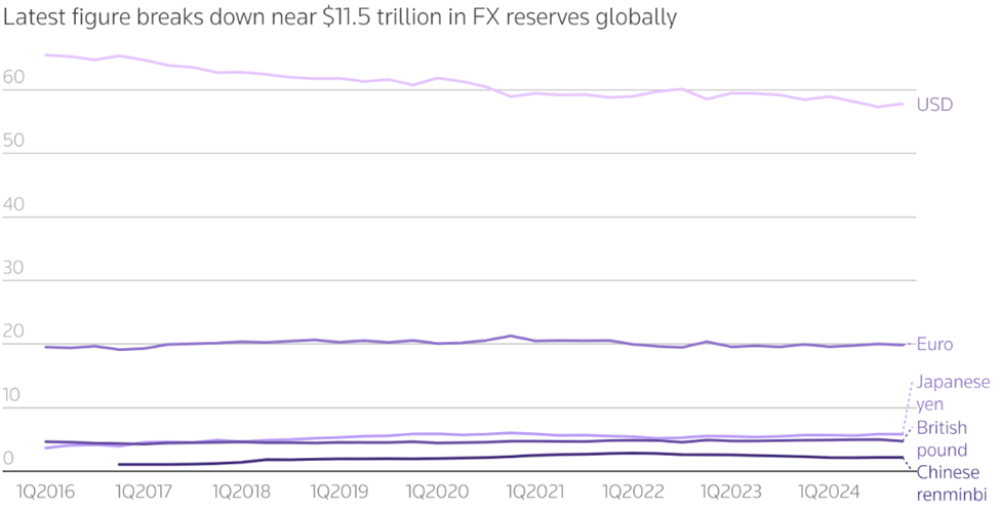

RM: Did you notice Citi [bank] has indicated the American stock market no longer warrants buying and they’ve downgraded U.S. equities to neutral from overweight? They also suggested investors should begin diversifying beyond America.

Deutsche Bank stated that markets are reevaluating the dollar’s fundamental underpinnings as global reserve currency, due to geopolitical and strategic shifts, de-dollarization and BRICS initiatives.

Reuters

New transaction systems avoiding American banks, and commodity exchanges increasingly denominated in non-dollar currencies.

Ultimately, bonds, dollars and stocks are simultaneously declining. Structural weaknesses exist in bond markets and people are reconsidering the dollar’s position.

BM: Well structural problems plague the entire global financial framework, not merely bond markets, it’s the complete system and Donald Trump just tossed an explosive into a packed venue. You cannot enter a motorcycle establishment and challenge the largest individual without expecting severe consequences and Trump’s inconsistent tariff approach lacks coherence and numerous supporters remain because some positions he advocates I consider brilliant.

We’re experiencing a fascinating historical turning point, it will prove interesting observing developments, I believe considerable likelihood exists we’ll engage in warfare.

RM: We discussed this during our previous conversation where we both concluded Middle Eastern conflict might trigger events.

Are you worried about America’s massive unfunded liabilities?

BM: No, we discuss funded obligations as though they’re significant, they’re entirely inconsequential. There’s a principle few comprehend and practically nobody except myself fully recognizes. All debts get settled, either by borrowers or lenders. The issue isn’t America’s accumulating debt, but America’s spending because payment becomes inevitable, whether through taxation, inflation or default and I see no resolution to this debt crisis except catastrophic default.

RM: Well the federal government collects slightly above $5 trillion annually, current year expenditures exceed $7 trillion, creating $2 trillion deficit requiring financing. Interest payments on unfunded obligations already constitute the government’s largest expense. Such spending restricts many worthwhile policy initiatives.

Federal Reserve chairman Powell appeared on television saying something particularly striking and we haven’t reached stagflation yet but he expressed concern about rising inflation, increasing unemployment, and already slowing growth, that precisely defines stagflation. We haven’t arrived there yet, but I believe America heads toward severe stagflation — would you agree?

BM: I think conditions are worse. Substantially worse. I’ve forecasted for 15 years an impending massive financial crisis in America culminating in market collapse across all sectors exceeding 1929 severity. I believe it’s commenced, it’s begun though nobody recognizes it yet, Donald Trump’s tariff actions inevitably create enormous complications, he’s throwing wrenches into an already vulnerable system. Introducing mechanical obstructions into machinery doesn’t improve operations it worsens them.

RM: The stagflation scenario probably represents the optimistic projection for forthcoming events.

BM: I experienced stagflation during Nixon and Carter administrations and people could manage it, many lost employment and interest rates climbed and circumstances deteriorated but we survived.

RM: But precious metals surged, and mining investments performed excellently during the ’70’s, vastly outperforming bonds and traditional markets. That situation appears to be developing currently, stagflation or comprehensive collapse.

Bob you and I observe these developments together, I’ve got substantial free time too. I conduct extensive research and frequently browse online and simply shake my head watching events unfold, it’s somewhat pleasant avoiding daily routines. I’ve been retired 20 years and we retired my spouse early and together we manage our business, televisions remain active as we monitor global situations. Occasionally we simply must switch off the nonsense and disengage due to absolute foolishness pervading statements and actions. Nothing makes logical sense whatsoever.

BM: Let me illustrate. Being French naturally, Macron discusses deploying French troops to Ukraine. Starmer in Britain contemplates similar measures. The entire British Army could occupy Wembley Stadium leaving vacant seats. British forces total 75,000 personnel, requiring 72,000 for ceremonial functions, leaving potentially 3,000 individuals for Ukrainian deployment.

Ukraine represents history’s most senseless conflict. It began as civil unrest instigated by America and NATO targeting Russia, resulting in complete disastrous failure for NATO, Germany, European Union, United States and nobody possesses courage to acknowledge mistakes. Why not terminate operations correct? Worthwhile endeavors deserve proper execution while pointless activities warrant abandonment.

That constituted an incredibly stupid confrontation offering no victory path and Russia honestly isn’t Europe’s adversary, nor America’s enemy. All rhetoric regarding Russian European invasion intentions is fabricated nonsense. France faces no Russian threat, France confronts American hazards.

When America sabotaged Nordstream [pipeline] and as both intelligence operative and combat veteran I assert America destroyed Nordstream no alternative perpetrator exists, they effectively destroyed European economic foundations. So why does Macron fear Russia? Why does Starmer worry about Russia? They should concern themselves with America, America represents their adversary not Russia.

RM: America seems to behave extremely antagonistically toward numerous parties.

BM: Well we inhabit fascinating times making me grateful for advanced age. Speaking today on Good Friday, do you know my primary concern?

RM: Easter celebration costs?

BM: No. Our entire societal structure verges on catastrophic failure due to systemic complexity and now Trump’s administration introduces explosive devices into crowded environments.

RM: “The complexity of everything.” That’s quite astute Bob captures it perfectly.

Bob I forwarded information regarding Basel III. Fundamentally for us it might ultimately involve allocated versus unallocated gold and American responses, interestingly they announced reassessing certain asset valuations then DOGE requested Fort Knox gold audit.

What’s your perspective regarding Basel III and American Endgame? Do you anticipate increased retail interest in gold? Central banks actively purchase gold, suggesting possible connection with global currency system reset. What thoughts regarding Basel III?

BM: It represents ongoing developments with fascinating implications and essentially Basel III requirements mandate banks maintain stronger reserves including gold. I attempt addressing overlooked topics. I’ll pose questions for your best responses.

RM: Certainly.

BM: Avoid numerical answers, but comparatively how large is the silver marketplace?

RM: Minuscule.

BM: Extremely small. Negligible. And comparatively how extensive is the gold marketplace?

RM: Not substantially larger, perhaps slightly bigger but minimal, equally insignificant.

BM: Appreciated. Everyone unnecessarily complicates matters. During 2007 I wrote regarding GFC [Global Financial Crisis] stating everyone believes securing seating remains possible when music stops. But suppose seating scarcity exists?

Similarly applies to gold especially silver. When music ceases everyone will shock discovering seating absence, understood?

What happens when gold appreciates $500 daily becoming unobtainable? Imagine multiple buyers competing for each ounce? Resulting unprecedented chaos awaits. Generally I retain rather than sell precious metals, understood? Those represent my financial turmoil insurance.

Gold and silver mining stocks’ relative value compared against metal prices registers lowest levels in 45 years understood? Observing gold appreciating 3% single day represents significant movement. We experienced three instances last week.

I anticipate my gold investments appreciating 10 or 15% because they should command premium above gold price increases. People remain so skeptical regarding gold it’s guaranteed, understood, for profit generation.

Gold ownership serves multiple purposes. Primary purpose involves financial chaos protection. Financial chaos manifests currently pleasingly since I maintain protection.

Investment aspect exists additionally and I constantly evaluate optimal current investment opportunities. Now I’ll state numerous gold and silver companies exist poised for 50 or 100-fold appreciation. People will express astonishment.

RM: Shouldn’t surprise anyone because between us, we recognize historically optimal leverage against rising precious metals prices involves owning quality junior exploration companies seeking and developing gold and silver deposits. That represents indisputable factual reality.

BM: No you’re mistaken, quality isn’t mandatory. I visited one Tanzanian company around 2007, 2008 where describing management as fraudulent dishonest incompetent would constitute compliment because actual situation exceeded those descriptions. They completely depleted finances completing financing at five cents, understood? Currently numerous 5-cent stocks exist but few existed then.

They secured financing at 5 cents, subsequently drilled previously held property yielding excellent results driving shares to 5 dollars. Having warned about management incompetence deception dishonesty cheating thievery what outcome befell that company?

BM: Thank you, so prepare for astonishment some companies led by corrupt incompetents will appreciate 100-fold having already occurred previously.

Curiously discussed in my financial publications, sentiment’s importance relates directly to history’s greatest human behavior analysis “Extraordinary Popular Delusions and the Madness of Crowds”. Reading that confirms human stupidity. Simply determine prevailing behavior then act contrarily understood?

You recall several months ago predicting stock market peak alongside cryptocurrency peak. Everyone dismissed me as blithering imbecile proven incorrect.

RM: You followed sentiment indicators?

BM: Obviously. That motivated writing those financial books initially. They represent straightforward publications anyone comprehends within hours and future generations will reference those books because I express numerous concepts with absolute clarity avoiding confusion,

When purchasing investments seeking profits sell upon achieving profits.

RM: Two observations regarding this discussion. Firstly, regarding your books, selling advice remains timeless. Sound guidance maintains relevance today tomorrow indefinitely.

Secondly, my selling decisions stem from discomfort continuing ownership, that motivates selling. Future projections past performance external recommendations holding selling, all prove irrelevant.

I sell experiencing discomfort continuing ownership, fearing profit loss. So selling occurs when discomfort arises regarding accumulated profits if comprehensible.

BM: Perfect comprehension indeed, referencing “Extraordinary Popular Delusions and the Madness of Crowds” sometimes people object to my characterizing humans as exceedingly unintelligent. Well justification exists within observable behavior patterns.

People exhibit maximum optimism at absolute peaks and maximum pessimism at absolute bottoms, numerous resource sector stocks several months ago couldn’t attract interest, understood? I recognize opportune acquisition moments.

I continue purchasing certain stocks at 2 or 3 cents because despite potential worthlessness, potential exists for 20 or 30 cent appreciation, we’re entering territory 99% of investors never experienced. Have you examined ancient cartography from 15th, 16th centuries? Depicting unknown territories?

RM: “Here be dragons.”

BM: Precisely describes current circumstances. “Here be dragons.” So purchase during inexpensive periods and sell during expensive periods.

RM: The gold-silver ratio during our initial conversation registered 102 and remains 102, gold’s $3,300 silver’s $32.50. Conducting casual research I utilized AI searching. I investigated average gold-silver ratio spanning 20 years, receiving 60 to 1 response, suggesting $55 silver today.

So, acknowledging gold’s attractiveness, silver offers superior opportunity in my opinion and our discussion covered numerous topics, gold silver justifications and my firm conviction that optimal leverage against rising precious metal prices involves quality junior exploration companies, but I perceive major discrepancy, specifically gold-silver ratio disconnect and I intend discussing one silver opportunity shortly. But would you elaborate regarding New Found Gold Corp. (NFG:TSX.V; NFGC:NYSE.American) Your thoughts?

BM: Ok, investors must understand personal responsibility for profits and losses, so rather than seeking gurus, comprehend why guru popularity exists? It seems counterintuitive yet simple why are gurus popular?

RM: I employ comprehensive analytical frameworks, macro-micro examination for everything proceeding accordingly. I disregard gurus, questioning why anyone heeds them.

BM: Well guru popularity exists, revisiting “Extraordinary Popular Delusions” human irrationality prevails, because someone receives blame following mistakes.

I possess extraordinary narratives spanning hours regarding promising stocks where isolated poor decisions caused implosion.

I possess reasonable judgment but people heed gurus avoiding personal responsibility, returning to New Found Gold.

You’ve examined assay results revealing hundreds of ultra-high grade gold intersections. The primary mistake those young executives controlling the company made involves resource estimation methodology, utilizing scattered sampling attempting evaluation across the entire project covering extensive area, producing extraordinary results, but attempting evaluation across dozens of kilometers strike length they erred with excessive drilling intervals.

They secured numerous positive gold intersections, when qualified professionals prepare 43-101 documents two considerations apply. They consider drilling spacing intervals and regardless of grades, larger drilling spacing reduces estimated gold content due to uncertainty within undrilled zones.

Another critical yet largely unknown factor involves capping ultra-high grades understood? With 75 gram intersection you’ve analyzed half the core. Will remaining half contain 75 grams? Answer: not necessarily, potentially containing 150 grams or merely 5g so with 7-meter 75g gold intersection you cap it. You estimate 10 grams rather than 75 grams throughout.

RM: Myself and many others question whether NFG contains more than 2 million ounces?

BM: While avoiding guarantee terminology however I’ll definitively state 2,000,000 ounces reflecting 43-101 measurement, accuracy probability equals zero.

It’s absurdly conservative ensuring subsequent 43-101 will contain substantially greater gold, representing Fosterville-type deposit understood? Fosterville transformed Kirkland Lake from $3 billion company into $18 billion company.

Recent New Found Gold purchasers will profit tremendously, it’s extraordinary project, lacking fundamental flaws.

Some decisions retrospectively appear misguided but given robust market conditions which we lacked, perhaps they weren’t actually wrong merely temporarily inappropriate but anticipate substantially exceeding 2 million ounces.

Two respected geologists, two individuals I know discussing New Found Gold’s 43-101 both employed identical terminology, specifically the 43-101 is nonsensical.

RM: I experienced profound shock witnessing such modest resource estimation.

BM: The gold exists, Fosterville featured depth, New Found Gold lacks depth maintaining shallow mineralization indicating additional gold. Meaning subsequent 43-101 promises intrigue.

Naturally management will appear heroic but share prices declined through Labrador Gold share disposals alongside exceptionally conservative 43-101.

RM: Two discussion aspects. Initially, regarding your publications, selling guidance remains perpetually relevant. Worthwhile advice retains relevance indefinitely.

Secondly, my selling decisions originate from ownership discomfort, that triggers selling. Future projections past performance external recommendations holding selling prove irrelevant.

I sell experiencing discomfort continuing ownership, fearing profit loss. So selling occurs when discomfort arises regarding accumulated profits if comprehensible.

I’ll discuss an attractive silver opportunity from my advertiser portfolio. I appreciate CEO Jason Weber demonstrating intelligence, I admire his Silver North Resources Ltd. (SNAG:TSX.V; TARSF: OTCQB) development. Trading symbol SNAG, they control property optioned to Coeur [Mining] while Coeur operates CRD along Yukon border.

Silver North’s Tim property remains under Coeur option. Coeur continues property exploration. Confidence levels remain extraordinarily high regarding carbonate replacement system presence resembling Coeur’s neighboring project. That project presents interest though optioned allowing Coeur continuing earn-in.

The property receiving today’s focus involves Silver North’s Haldane property situated within Yukon’s Keno Silver District, representing globally premier high-grade silver region. The district produced 200 million silver ounces historically with mines classified primary silver operations generating zinc lead byproducts.

SNAG’s Haldane project neighbors Hecla [Mining], who commenced mining during 2023 possessing proven probable reserves approaching 50 million ounces @ 700 grams per tonne. Their project mineralization, currently under production, resembles Haldane project characteristics.

Average Keno district silver operation contains 30 million ounces understood, with historical production grades approximating 1,100 grams per tonne silver, classified primary silver operations rather than silver-equivalent operations.

Silver North maintains clear plans, focused direction and implementation. They recently secured $1.35 million representing hard money preceding upcoming charity financing potentially reaching $4 million and charity financings typically require comfortable hard money reserves initially.

Observers recognize this pattern and they completed charity financing last year suggesting anticipated success raising potentially $4 million focusing on drilling 2,000 to 5,000 meters, depending upon financing outcome, targeting their recent Main Fault discovery.

They’ve completed three modest drilling campaigns each yielding discoveries, however Main Fault stands exceptional, representing substantial mineralization exhibiting three distinct layers. They believe current year drilling will minimally establish clear visibility towards, if not outright achieving, standard 30-million-oz Keno deposit.

Given current share pricing they could complete 17.5-cent financing calculated fully including warrants yielding 138 million shares outstanding fully diluted. Additionally $1.5 million in warrants at 15 [cents] potentially exercisable.

Conducting valuation analysis, the property contains 12 kilometers vein potential; additional discoveries exist including high-grade West Fault. Considering current market capitalization reasonable expectations include multiple returns following successful drilling campaign.

I favor this project for standalone potential, alternatively providing integration opportunity with Hecla’s existing operation. Consider, they possess 49.7 million ounces proven probable mining reserves, you’re adjacent, merely 2 kilometers from Hecla’s processing facility. Demonstrating 30, 40, 50 million silver ounces likely attracts serious consideration from Hecla.

BM: I’ve not monitored this however during your presentation I conducted research and another project priced so affordably that believing in silver justifies investment. Substantial historical silver production occurred there, predicting Yukon popularity this year.

RM: I favor their prospects building primary Keno silver deposit.

BM: Indeed, acknowledging silver appreciation requires recognizing leverage available through quality pure silver investments. Hecla proximity represents substantial advantage.

RM: Absolutely crucial, Hecla maintains junior-friendly corporate culture, they maintain cooperative relationships with juniors, they’re approachable business partners.

BM: Timing appears nearly perfect and I commend them securing adequate funding for meaningful drilling program.

RM: Were additional topics warranting discussion today Bob?

BM: Future discussions await certain topics.

RM: I appreciate your time commitment with us.

You can view more from Rick and Bob at Ahead of the Herd and 321Gold.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Important Disclosures:

Silver North Resources Ltd. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000.

As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Silver North Resources Ltd.

Rick Mills: My company has a financial relationship with Silver North Resources Ltd. I determined which companies would be included in this article based on my research and understanding of the sector.

Bob Moriarty: I determined which companies would be included in this article based on my research and understanding of the sector.

Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Ahead of the Herd Disclosures

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH. Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.