Modest price gains in gold, silver on corrective bounces – KITCO

Modest price gains in gold, silver on corrective bounces KITCO Powered by WPeMatico

Modest price gains in gold, silver on corrective bounces KITCO Powered by WPeMatico

Silver Price Analysis: Rebound capped below $70 with downside risks FXStreet Powered by WPeMatico

Gold is down around 20% from recent highs, even as oil prices surge. These two commodities usually rise in tandem, leading many investors to wonder […]

GR Silver Mining Mourns the Death of CEO Márcio Fonseca Mexico Business News Powered by WPeMatico

HL vs. PAAS: Which Silver Mining Stock has Greater Upside? Yahoo Finance Powered by WPeMatico

Silver Miners Are Up 124%, Platinum Up 89%: The 3 ETFs Giving Commodity Investors Access to Both 24/7 Wall St. Powered by WPeMatico

GR Silver Mining Announces Loss of President, CEO, and Founder, Márcio Fonseca Investing News Network Powered by WPeMatico

Gold, Silver Prices Are Getting Hit Today. One Big Thing Is Doing the Damage. Barron’s Gold and silver price higher amid inflation and interest rate hike […]

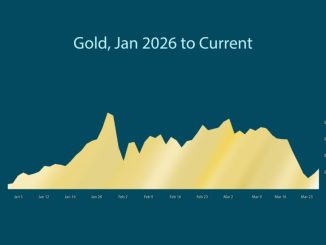

Current price of silver as of Thursday, March 26, 2026 Fortune Powered by WPeMatico

Silver Prices Have Plunged 20% in Just 1 Month. Should You Buy the Dip? Yahoo Finance Powered by WPeMatico

Copyright © 2026 | WordPress Theme by MH Themes