Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

A wild week for markets as the U.S. and Iran come to the brink of war before both sides apparently decided it would be wiser to pull back.

After Iranian missiles hit a U.S. military base Tuesday night, gold prices surged above $1,600 an ounce. As gold headed toward a 7-year high, even the mainstream media had to take note. Jim Cramer and his fellow stock market pumpers on CNBC took time to lament the fear-driven buying of gold.

Fear buying of gold and other safe havens ended up being short lived. After U.S. officials reported there had been no casualties and Iran stood down, fears of World War III suddenly turned into hopes for a quick end to hostilities. Wall Street celebrated as metals markets sharply reversed mid-week.

As of this Friday recording, gold is now relatively flat overall for the week to trade at $1,560 per ounce. The silver market shows a slight weekly gain of 0.2% to bring spot prices to $18.16 an ounce. Platinum is off 0.4% last Friday’s close to come in at $982.

And finally, palladium pushed through the $2,000 level for the first time ever. It currently trades at $2,129 on the heels of a 6.5% advance this week.

Well, while we can all take comfort in the tamping down of tensions between the U.S. and Iran, it would be naïve to believe that the threat of further conflict in the region is over.

It appears that Iran was in fact responsible for shooting down a Ukrainian passenger jet. If it instead had been an American Airlines jet loaded with U.S. citizens, we’d likely be seeing much more of a reaction from President Donald Trump and perhaps our military forces as well.

Iran or Iranian-backed terrorists could be planning other forms of retaliation as I speak. The assassination of Iran’s top general has stoked extreme new levels of anti-American resentment. It won’t abate anytime soon, especially as the Trump administration is vowing to impose tougher economic sanctions to punish Iran.

America is also struggling to keep Iraq from forging closer relations with Iran. Iraqis increasingly want U.S. forces out of their country.

Democracy in the Middle East never quite works out the way the foreign policy central planners in Washington envision. After so many years since 9/11, after so many trillions of dollars invested and ultimately wasted in Iraq and Afghanistan, President Trump at this point is looking for an honorable way to cut our losses.

But his neo-conservative advisors still cling to grand notions of re-making the region in our own image. And the pull of the Israeli lobby and military-industrial complex is perhaps the most powerful force in Washington. D.C. — as all Presidents come to learn.

Of course, precious metals markets will need more than occasional geopolitical flare ups to drive a long-term bull market advance. The fundamentals are turning in favor of higher gold and silver prices. From fiscally reckless trillion-dollar deficits in Washington, to a Federal Reserve obsessed with generating higher rates of inflation, to mining supplies of gold and silver looking tight, the ingredients for a big bull market are in place.

However, safe haven demand from investors has yet to pick up in a big way. We saw some of it this week, but it will likely be fleeting until the general public sees good reason to pull assets out of the stock market.

As stocks hit record highs last year, gold and silver coin sales at the U.S. Mint plunged to multi-decade lows.

The U.S. Mint sold just 152,000 ounces worth of gold American Eagles in 2019. That marks the lowest total on record going back to 1986. Meanwhile, sales of silver American Eagle coins came in at their lowest level since 2007. Now granted, a robust secondary market as a result of hordes of retail investor selling supplied the market with a cheaper alternative to the newly minted coins, and that explains part of those low numbers for 2019 U.S. minted product.

Australia’s Perth Mint, however, saw an increase in coin demand from its more internationally based buyers. Many sought physical bullion as a refuge from negative interest rates in their home countries.

As U.S. investors realize that they too face the prospect of negative real interest rates on savings and bubble valuations in equity markets, they too will increasingly find a compelling value proposition in gold and silver.

Well now, for some predictions on what 2020 will look like for the metals and the other markets, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome in Craig Hemke of the TF Metals Report. Craig is a well-known name in the metals industry and runs one of the most highly respected websites in our space and provides some of the best analysis you will find anywhere on banking schemes, global macroeconomics, and evidence of manipulation in the gold and silver markets.

Happy New Year to you, Craig. Thanks for coming on and welcome, how are you?

Craig Hemke: Mike, it’s always a pleasure. New Year’s started off with a bang, man. I hope it’s not indicative of how crazy this entire year is going to be. We’ll see.

Mike Gleason: Yeah, certainly this week sparking action itself. Lots going on both geopolitically and in the markets, and we’ll get to a lot of that. Well, Craig, here we are entering another new year. The conflict with Iran and the potential for an escalation there spurred some safe haven buying in recent days, but the rally in metals started last month. I’d like to open by getting your thoughts on what you believe will be driving metals prices this year. Yes, we expect the forces of evil to continue doing their best to manage prices, and we’ll get to that topic of price manipulation in a moment, but talk about what you’re seeing in the metals here recently and discuss some of the themes you anticipate people will be talking about this year when it comes to the metals.

Craig Hemke: Well, I think it’s critical that people try to have a longer memory than 48 hours. As we record this today, I’m seeing all kinds of garbage. I saw garbage from some group that is always a perma-bear, always talking about how gold has topped out and going down, has a clear agenda, just like some of the short sellers that are always anonymously pound the mining stocks with fake research reports and stuff like that. And I’m seeing these things today about how, “Oh yeah, gold, look at that. Look how terrible that candle looks on the daily chart, and how come hold’s not going up when all this war stuff,” and it’s like, do you not understand? I mean, gold went up prior to the war starting. Beginning last Thursday, gold closed on the Comex, last Thursday, January the 1st at about $15.30. So, the whole move from $1,530 to $1,580 was war premium, if you will, really short-term war premium. Then the spike to $1,610 was when we seemed to be on the verge of what could even have been a nuclear war in the Middle East.

The fact that it’s pulled back to $1,550 shouldn’t surprise anybody. I mean, we hadn’t even worked out all the war premium yet. Despite what is some pretty cheery economic news this week, service sector PMIs, the ADP jobs report, that kind of thing, so jeez-Louise, I sure hope people keep their perspective. You are correct in pointing out, Mike, that the metals rallied strongly into the year and it had nothing to do with war. That wasn’t on anybody’s mind prior to about six o’clock in the evening on January the 2nd. Gold rallied 3% from December the 20th through that date. Silver rallied 8.5% from December 9th at $16.60 up to $18.40 on January the 2nd. The HUI, the gold bugs index … which everybody’s freaking out because the shares went down yesterday. The HUI is up 15% still since the middle of October. For a while it was up 20, and why is this happening? Because the Fed, whether they want to call it QE or not, began this direct monetization of the debt program in October.

Everything’s going up. Stock market, you name it, and that is going to continue this year. It’s only going to get worse. A lot of people missed last Friday, the 3rd, the minutes for the December Fed meeting were released. First of all, everybody was on vacation still on Friday, January the 3rd, and second of all, those are always released on a Wednesday, three weeks after the Fed meeting. So, no one’s looking for them on a Friday afternoon at two o’clock, but here they came. And buried within the minutes, anybody can pull these up, is admission that what’s very likely to happen in the months ahead is the Fed will start monetizing not just T-bills, but notes, longer term duration notes, two years, three years, five years, seven years, ten years. There’s no other option. They cannot afford the stock market to go down. They cannot afford the money supply to contract, and thus they will constantly be printing all through this year more and more dollars, and everything is going to go up for the reasons that were driving them last year. Please don’t get caught up in what happened and how the chart looks based on these extraordinarily rare events that we saw back on Tuesday.

Mike Gleason: There’s been a bit of a pattern in recent years where the metals start perking up in December and perform well in the first half of the year. Any thoughts about what’s behind that and are you looking for that pattern to repeat this year, Craig?

Craig Hemke: Yeah. We were talking about it on my site all the way through December. It was logical to expect, first in November, you expected the metals to trade lower because the December contract is always the most heavily traded all year long. And the December contracts, both gold and silver, had massive open interest and they were both going off the board at the end of November, which meant all the speculators that were long were going to have to sell, and if they don’t completely roll over their positions into February, then that effect is a selling pressure. The price went down.

I told people all through November, I thought, $1,440, that’d about do it. We’re already so extremely oversold. I couldn’t see a waterfall down. I think we saw $1,445. I thought we’d rally into the end of the year because as you said, Mike, that’s typically been the pattern, especially since the bear market lows were put in back in 2015. The shares performed well, especially in the back half of December, because they’re subject to so much tax loss selling, particularly in Canada, and that usually concludes around 18th, 20th. People want to get that done before they go on Christmas holiday. And so once again, we got that behind us and up with the metals. Let me just point this out to you, Mike, because this is a lot like last year. You remember last year, the stock market crashed. Remember that in December of 2018?

Mike Gleason: Sure. Worst December in decades.

Craig Hemke: Yeah, it was crashing, and basically the stock market was catching down to the contraction of the money supply that the Fed was doing by trying to “normalize”, whatever that means, their balance sheet, and the stock market finally caught on to that disappearance of liquidity. And so, what happened? On Christmas Eve, (Treasury Secretary Steven) Mnuchin… and anybody can look it up, I’m not making this stuff up… Mnuchin called a meeting of what’s called the Plunge Protection Team, the President’s Working Group on Financial Markets. They came up with a strategy to float it back higher. The day after Christmas, after the holiday, the Dow went up a thousand points and never looked back. Now, this was when gold first started to move higher, was in December last year, because interest rates had peaked in November, and this is what all caused me to issue a forecasting saying ’19 was going to be the best year for the metal since 2010. Well, why? Because the Fed was going to be reversing course and they were going to be printing cash because they don’t have any choice but to liquefy and continue to liquefy all these markets.

They can’t have deflation. They can’t have crashing stock markets. They can’t have higher interest rates, none of that stuff. So, in December of 2018, gold starts to rally, and everywhere everybody’s like, “Well, this is just a safe haven deal. Gold’s going to $1,100 in 2019,” and all this crap, Harry Dent stuff. Anyway, that’s not what happened. It wasn’t what was going to happen. It’s not what did happen, and so now here we are, gold rallying again, anticipating what’s going to be happening this year and it’s the same thing. “Well, the only reason gold went up is because of the safe haven stuff,” as if gold rallying in December and the shares railings since October had something to do with the idea that the U.S. was going to whack this Soleimani character on January the 2nd. It didn’t have anything you do with that. Gold is simply looking ahead, looking over the horizon as it always does, sees all this liquidity coming from the central banks around the world because it can’t afford to do anything else and it’s moving higher, and people need to understand that and they need to plan for that as they make their investment allocations for 2020.

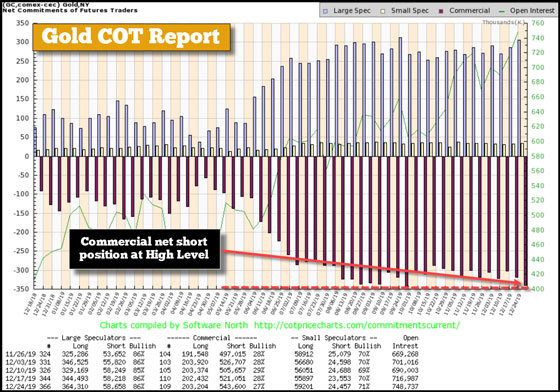

Mike Gleason: Now let’s talk about price manipulation. Nobody does a better job than you when it comes to covering what the crooked bankers are up to in the paper markets for gold and silver. They sold a boatload of futures contracts last year in both metals. You observed that open interest in gold was up a whopping 70%. Said another way, the supply of paper gold rose by 70%. Yet the amount of gold in the vaults backing that paper barely budged. It’s quite the racket. So, while gold itself is actually scarce and hard to produce, futures contracts are exactly the opposite. The supply is essentially unlimited. Last year, 33 million new ounces of paper gold were dumped into the market. Despite that, gold prices still managed to rise by 18% or so. So, what do you make of that?

Craig Hemke: Yeah, I mean, how the world, and I guess, I don’t know, too many people get their beaks dipped in this or just simply don’t care, but how the world allows, how the mining companies allow their product to be priced, not off of the exchange of the actual commodity, but off the exchange of these derivative contracts that have nothing to do with anything. It’s like I look at you and I say, “Mike, here. We’ll call this contract between you and I gold, and I promise at some point that I got the gold behind it and if you want it, I’ll deliver it to you,” and then you promise that you’re actually interested in it and you go borrow a bunch of money from your broker-dealer to buy it on margin, and then we just pretend that that contract is actually … there’s going to be some physical exchange between us at some point, but that never happens, and at the end of the day you just say, “Well, I liked my exposure,” and I sell my contract. You sell your contract and I, taking the other side of it, buy it back, and there was never any gold exchange at all. There was just some weird promise that there was a backing to it and it’s a trading of those things that is allowed to determine prices. It’s just ridiculous.

Yeah. Let’s backtrack to that open interest thing that you said, because here’s a great way to look at it. Everybody knows, or at least should know, that 2018 was the largest year of global central bank gold purchases since 1969, the year after the London Gold Pool, 651 metric tons. Projections are, run rates, I haven’t seen the actual final numbers yet, but the projections are the 2019 was even greater, probably about 670 metric tons. So, there is what, 25% of global mine output actually demanded, I guess, as far as we can tell, physically delivered to the central bank – 670 metric tons of physical demand, offset by, as you said, the creation of over 1,000 metric tons of digital pretend paper, gold contracts. It’s like a two headed monster. I mean you’ve got the actual physical product, which as you said, is scarce, being priced by the trading of derivatives, which can be created infinitely because no one ever calls any of these people to the carpet. So it’s ridiculous. It’s outlandish.

Yes, gold managed to rise 18% last year, even while the supply of derivative contracts increased by 73%. Imagine if there was some forced linkage between the ability to create contracts and the amount of actual gold on deposit in the vaults, and you couldn’t have increased it by 73%. What if the supply only increased by 10%? Well then all that money around the planet looking for gold exposure would have had to find it through acquisition of existing contracts. This is how the stock market that allegedly works, but that’s not how it works in the pricing of precious metals. The banks just create more contracts, taking the opposite side, taking the short side, and figuring they can out last the speculators, eventually maybe forced them out and cover their shorts. It’s disgusting, and again, at the end of the day, what’s really astonishing are these dopey rock breaking geologist CEOs of the mining companies that think it’s a valid pricing structure and they fall for it. That’s what’s really mind blowing.

Mike Gleason: I want to ask you about the possibility of whether or not the bullion banks will lose control of prices anytime soon. That 70% jump in open interest is extraordinary. The department of justice is prosecuting several people and they have secured some guilty pleas. It’s interesting that they are using RICO laws. Perhaps they actually see the bank activity for what it truly is, organized crime. Officials in London are asking some pointed questions about the fraudulent use of EFPs, exchange for physical. An optimist would say that some of these developments will lead to reforms, but I think we’ve all learned that you should never overestimate bureaucrats’ ability or willingness to do the right thing. We may have to wait for the market to solve the problem, which will happen right after confidence in the futures markets, the banks, and/or the dollar collapses. What are your thoughts about how much longer this crooked price discovery system will persist, Craig?

Craig Hemke: Well, Mike, you’ve said a mouthful there. Let me pick off a couple of things. You mentioned the regulatory agencies. You got the Rico investigations here in the U.S. It’s pervasive. The fraud is pervasive. The former head of JP Morgan’s precious metals desk, who is also on the board of the London bullion marketing association, the LBMA – why would he be on both? Why would he be a JPM trader and on the board at the LBMA? But anyway, he’s now been indicted. The RICO statutes allow you to not just go after the goon, but allow you to go after the Don. So, we’ll see how far it reaches, however, it does reach across the pond. My friend Andy McGuire has been telling me this now for over a year, that the FCA, which is the English/British equivalent of the SEC, I guess, or Department of Justice, whatever, has been looking into the risks that are being taken by the English banks, and what that might pose the system.

Andy has told me about a meeting he had with a couple of Members of Parliament, and this guy, Andrew Bailey, who at the time was the head of the FCA. This was back in maybe August, and this Bailey had no idea, because the LBMA’s so opaque. I mean, you don’t get these stats every day, all the unallocated gold and all this stuff, and the risk that the bullion banks are taking there. So Andy laid it out for him and he said, this guy’s jaw dropped, and he’s like, “Look, we can’t afford a second financial crisis off of this. I mean the people … we already shafted them once. They’ll never let us get away with it again. We have to put a stop to this somehow,” and Andy told him about the EFPs, and we’ll get to how that continues in a second.

So anyway, this guy Bailey, who according to Andy said we got to somehow put a stop to this, this guy Bailey was just nominated and confirmed to be the head of the bank of England by Boris Johnson. So what’s he going to do? Does the buck stop when he leaves there, leaves the FCA and now he’s got to be a servant to the bank of England and stop paying attention? Or maybe he’s going to call the banks on the carpet. I know what direction I think any cynical or non-cynical person would think that that’s going to go, but I digress. These EFPs that I’ve been writing about for a couple of years, this is an arcane process that’s a part of every futures market, but I just can’t even describe the degrees to which it is abused … I guess that’s the right word … within golden silver.

I’ve kept track of … I don’t even know what it is… over the last two years, something like 14,000 metric tons of gold contracts. Each Comex gold contract is a hundred ounces, allegedly, of gold. Well, enough contracts that are the equivalent of 14,000 metric tons had been moved off the Comex and exchanged for physical (EFP) through London. Andy says they have this process where they swing them into these 13 day little contracts that are off the books and just keep rolling them over and over and over trying to kind of hide it and pretend that it’s not there, but this process continues. Mike, let me lay this on you. It’s just that we’ve had, as we speak, five trading days in the year 2020. In those five trading days, there have already been 67,713 Comex contracts shifted off of the exchange and exchanged for physical, as they say again, in London. 67,000. Mike, again every contract is a hundred ounces. That’s 6.7 million ounces. That’s 210 metric tons of gold.

The whole Comex vaults only holds 8 million ounces and they shifted 210 metric tons, 6.7 billion ounces off exchange in just five days? This is the scam of the greatest order, and like I said, again, the amazing thing is that it still exists… that people in 2020, when the world is all interconnected and everybody knows everything and I can watch missiles take off in Iran five minutes after they’re shot just by following Twitter. It’s amazing that this continues. It’s just mind boggling that this is allowed to continue.

Mike Gleason: Yeah. Well put, you beat your head against the wall trying to figure out when it’s going to finally end and why there’s not more talk about it. Well, Craig, before we wrap up, I’d like to get any final thoughts. I know you’ve got a lot to say here early in the year. If you could give metals investors an idea of what it is that you’re going to be watching most closely, what they should be watching most closely over these first few months of the year, and then maybe a sign that perhaps the powers that be are losing control, or any other comments you want to make here as we wrap up?

Craig Hemke: Yeah, I don’t know, Mike. Since I’ve been doing this, and I have to admit kind of fallen forward a little bit and getting excited about it myself back in 2009 and ’10, that kind of thing. This hyperbole of, “The Comex is going to fail.” Come on. That’ll all happen in a blink of an eye someday or overnight, but to sit there and … these people that say it’s going to fail above $22 silver. I mean, come on. We’ll see. The banks are going to keep it going as long as they possibly can and I don’t think anybody can come up with a time table for it. The only thing it that will end is a run on the banks for physical metal, and this kind of thing gains momentum and it snowballs and finally that realization of what a scam at all is sinks in and people panic to get their hands on actual mental while they can. Again, I can’t stress this enough, ignore the perma-bears with an agenda.

They’re trying to talk down the market. They’re trying to talk down the shares, or trying to talk down the individual shares because they have some massive short position. The Fed is going to continue with the repo crisis. It’s not going away. The U.S. is going to have at least a $1.2 trillion deficit every year this decade. That’s what the Congressional Budget Office says. That money’s got to come from somewhere. The central banks cannot afford a deflationary collapse. They will be printing and printing and printing. Even absent that argument about what that does to the dollar and all this other stuff, that cash goes someplace, and it goes everywhere. Again, it’s not a mistake that the HUI… was up 20% since October 15th… is now up 15%. What happened on October 15th? That’s when this whole new not-QE debt monetization program kicked in.

Everything’s going up. Okay? So everything’s going to continue to go up. The banks are going to throw up roadblocks. We’ve already got 800,000 contracts of open interest Comex gold. So, I don’t know how far gold will go. $1,650? Maybe if it kind of gets rolling, it can go to $1,750 this year. That’d be a pretty good year from where we are. Where I think the real interest should be, for people that want to either have some fun, make some trading fiat currency that then they can buy more physical metal, that kind of thing … I mean start looking into whether or not you have exposure to the mining shares, not just the big companies, but the medium juniors and the explorers, that kind of stuff, because as global asset managers, who have all this cash, and they’re always looking for a place to go. Once the GDX, the DDXJ, the HUI begin to make new highs versus 2016, the floodgates are going to open and money’s going to come pouring into the sector and it all has to pass through a little tiny funnel because there’s only so many places it can go.

It’s just simple economics. You get twice the cash chasing the same handful of stocks, and they’re going to go up in price. So, I think it’s going to be a very good year again for the metal, just like last year was, and I was right when I predicted it last year. But I think the real outsize gains will probably be in the shares more than in the physical metal. I wrote that up. I kind of make an annual forecast every January. I posted it to my site. It’s a free link. Maybe I’ll send it to you, Mike. You can put it on this page. I always try to come up with a catchy name, so this year’s title is 2020 Foresight, instead of 2020 hindsight. Kind of clever, huh?

Anyway, 2020 Foresight is what it’s called. You can go to my site, or like I said, click the link, if you can put it on this page, and it will just explain to you the basis for why I think it’s going to be a good year. If you’ve got time, I think it’s worth a read.

Mike Gleason: Yeah, it would be time well spent for sure. I always say, we spend a lot of time looking at your site here in this office. It’s money well spent for anybody that wants to get on board there with TF Metals Report. And before we let you go here, Craig, tell people a little bit more about your site, how they can get signed up, and maybe some other tidbits they should know.

Craig Hemke: Well really the best thing about my site, I mean I do analysis every day and we try to keep people locked into the big picture, not the tick by tick stuff, but the site is… I mean the people that populate it are from all around the world, all different political views, but we realize we’re all in the same boat, and so instead of bickering at each other and name calling and all that kind of stuff, rule number seven in the community guidelines is treat others the way you want to be treated. Come on, your mother taught you that. Why do you think just because it’s an anonymous website, you can be rude and mean like Twitter, things like that. So anyway, the community itself is what’s worth it.

It’s only 12 bucks a month. So it’s not like I’m getting rich off of it. 40 cents a day to give you access, really keep you on top and grounded of where we’re headed. And again, I just can’t emphasize enough. I mean Mike, the old line is a rising tide lifts all boats, right? Think of the rising tide being all of the cash. It has to be created from nothing. You must understand, this is direct monetization of the debt by the Fed. Primary dealers, they get the Treasury bills, soon to be Treasury notes from the Treasury. The primary dealers are the ones responsible for making that market and getting them filled. They buy them themselves, and anybody can, ZeroHedge has been great about writing this. The Fed then buys these directly from the primary dealers about 72 hours later. Okay, so there’s an intermediary in between, but basically the Fed is buying the Treasury bills, soon to be notes, directly from the Treasury.

How that isn’t direct monetization of that? I don’t know. Just because there’s a step in between? So, this is happening, Modern Monetary Theory, all that stuff that the politicians daydream about, that’s coming, and whether you are going to want to talk about gold standard and system reset and all that kind of stuff, whatever. Yeah, sure. But all of that cash is going to be sloshing around. Stock market’s going to go up, everything. So, gold and silver are going to go up and the shares are going to be particularly advantageous to own in the next few months. And so, again, I just want to keep everybody grounded and not be thinking about the events of Tuesday, and I mean that was a real, you want to talk about one off, that was a one off. That was hopefully something that you’ll never see again in your lifetime. This on the brink of maybe nuclear war in the Middle East. Ignore the reaction to it, the run up to it and look at the bigger picture and I think you’ll see that physical gold and silver and maybe some mining shares must be a part of a portfolio in 2020 going forward.

Mike Gleason: Yeah, well put. It’s going to be a great time to kind of focus more in on this if you’re not already doing that, and it’s going to be an interesting maybe, tumultuous year. Ignore the blips or don’t pay as much attention to them. We do have a trend in place here and Craig and TF Metals Report is a great way to follow that, hopefully right here on this podcast as well.

Well, very good. Thanks again Craig. Have a great weekend. I wish you a happy and prosperous New year and we look forward to catching up with you again soon. Keep up the good work, my friend.

Craig Hemke: All the best, Mike. Go Chiefs!

Mike Gleason: Yeah, good luck to your Chiefs this weekend. Well, that will do it for this week, thanks again to Craig Hemke. The site is TFMetalsReport.com, definitely a fantastic source for all things precious metals and a whole lot more. We urge everyone to check that out if you haven’t already done so for some of the very best commentary and analysis on the metals markets that you will find anywhere.